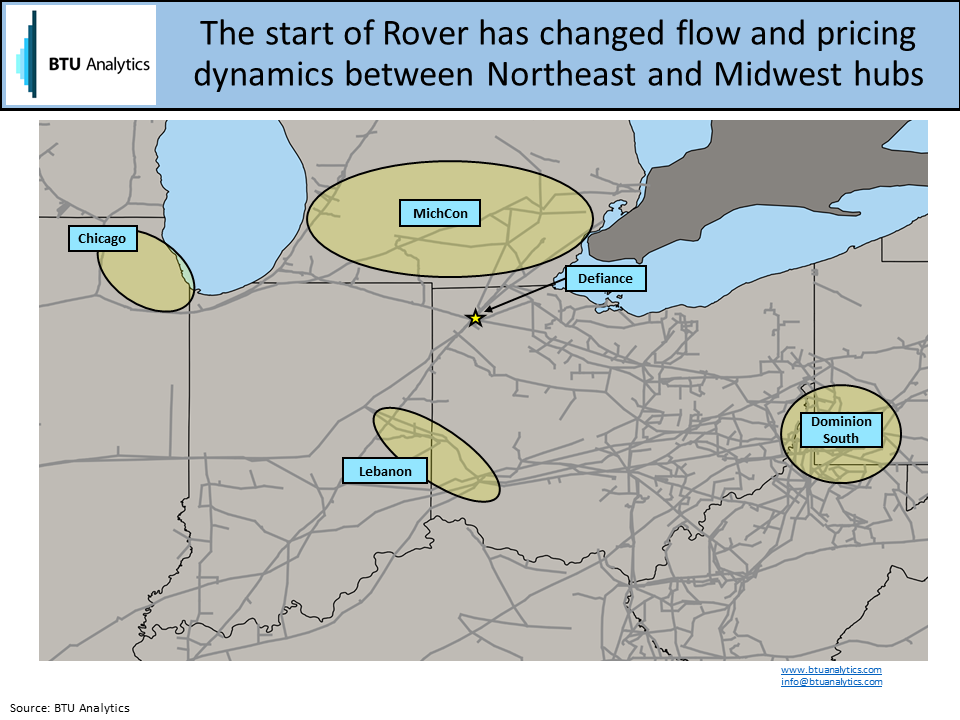

Rover recently received FERC approvals to start their Majorsville and Burgettstown laterals, which will bring the project up to its full effective mainline capacity of 3.25 Bcf/d. With so much Appalachian capacity targeting a limited market in the Upper Midwest, it was only a matter of time until we saw flow and pricing dynamics shift. Bearing the brunt of those shifts has been the Lebanon and Defiance hubs in southwest and northwest Ohio, respectively. However, impacts have propagated back to Dominion South, where prices are about $1.20/MMBtu stronger than this time last year. So how has Rover contributed to stronger Dominion South and, more importantly, how long will it last?

The map below shows the hubs in focus today. Rover began partial service back in September of 2017 delivering volumes to Defiance, Ohio. However, it was not until earlier this year when we started to see strong flows into the Midwest, reaching about 1.5 Bcf/d in February of this year.

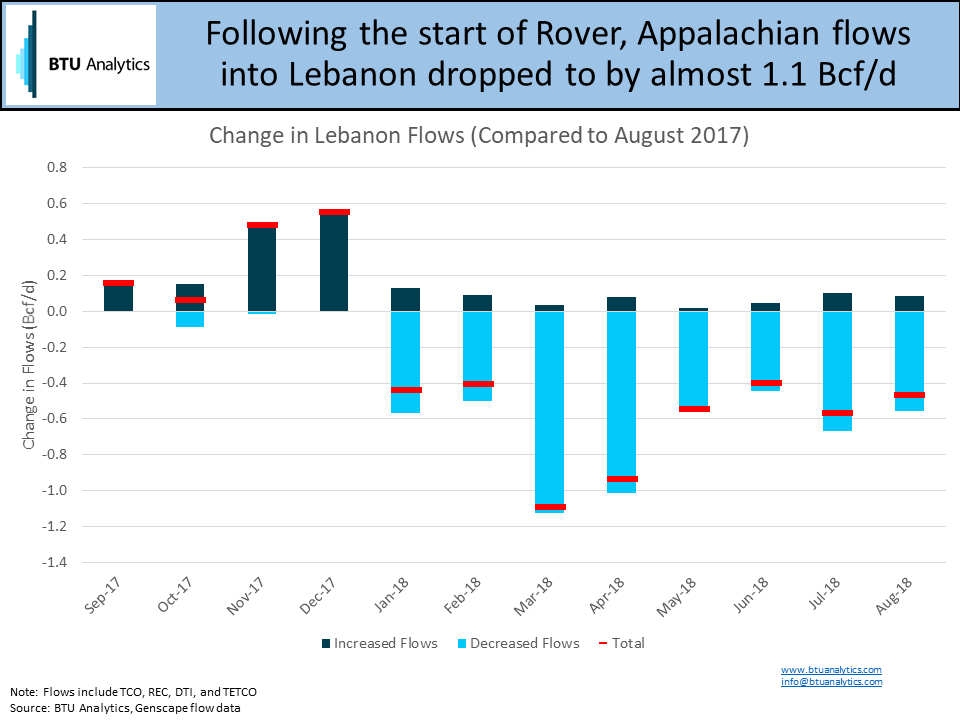

Before Rover, the main thoroughfare into the Midwest from Appalachia was via Lebanon on Texas Eastern (TETCO), Columbia (TCO), Dominion (DTI), and Rockies Express (REX). When Marcellus and Utica production grew in 2012/2013, utilizations to Lebanon were put under pressure as Appalachian volumes looked for any route towards stronger markets. With higher utilizations came wider spreads between Dominion South and Lebanon, reaching spreads as high as $2.00/MMBtu. However, with the start of Rover, volumes have been redirected off of this historically preferred route, as shown in the graphic below.

Just as higher utilizations along this route led to widening spreads earlier, lower utilizations have led to tightening spreads. This summer spreads between Dominion South and Lebanon averaged about $0.31/MMBtu, compared to the same time last year of $1.09/MMBtu.

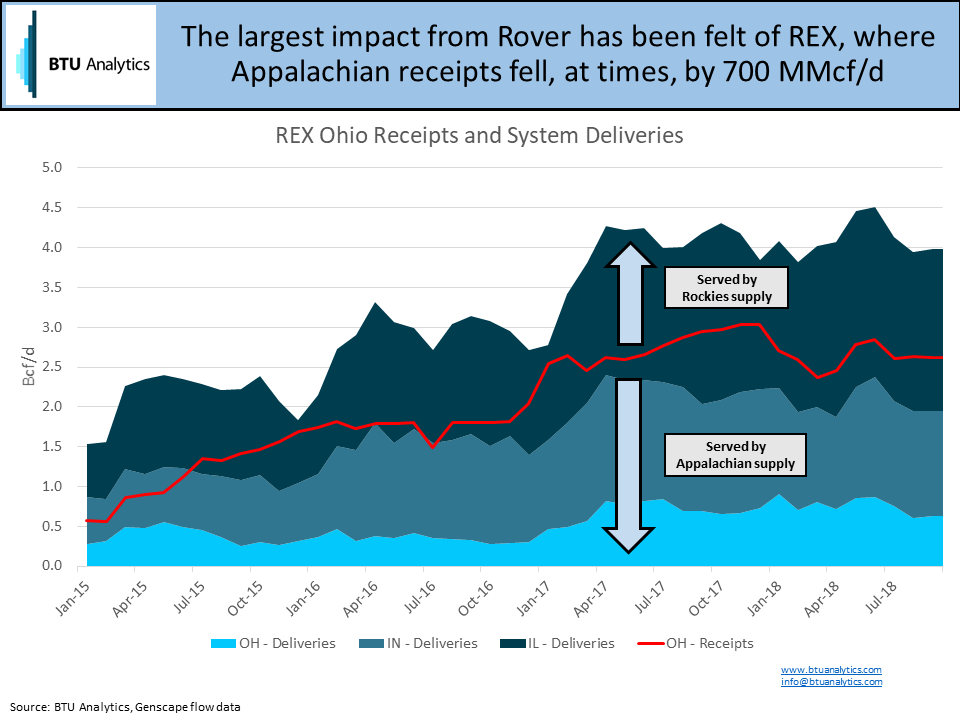

Bearing the brunt of this decline has been REX, which saw Appalachian receipts drop by as much as 700 MMcf/d following the start of Rover. Prior to Rover, REX had been making steady progress pushing Appalachian molecules farther and farther west, reaching NGPL’s Moultrie interconnect in Illinois just prior to the start of Rover last year. Surging Rockies outbound flows due to pressure from Permian associated gas and Appalachian volumes redirected to Rover have stalled this trend, however, as shown in the graphic below.

With under-utilized capacity between Dominion South and Lebanon on REX and others, spreads have tightened, and Dominion South has gained steam, but how long will it last? Lebanon has its own set of pricing mechanisms that we discussed in detail in our most recent Northeast Gas Outlook. If Lebanon prices continue to weaken as we have seen over the past two years, that weakness could drive down prices at Dominion South. In addition, surging production could drive spreads between Dominion South and Lebanon wider once again, putting us right back where we were a year ago.

Check out our most recent edition of our Northeast Gas Outlook where we devoted 10+ pages to discussing the emerging Lebanon pricing dynamics and the surge in production coming from Antero and EQT in the second half of the year.