Independent E&Ps are being increasingly pressured by investors to live within their means and generate positive free cash flow. However, given the low commodity pricing environment, some operators may not yet be in a position to do so. With capital markets increasingly difficult to tap into, some E&Ps have turned to shedding assets to inject additional cash flow into the company, either to fund operations, pay down debt, or return cash to investors. In past, private equity has been a willing buyer of E&P assets. That capital has been drying up throughout 2019, though, which is evident in recent acreage deals as well as equities markets. Today’s Energy Market Commentary will dig into the implied acreage values of recent deals as well as the implications for potential acquisitions of small and medium sized E&Ps based on the value of their equity today.

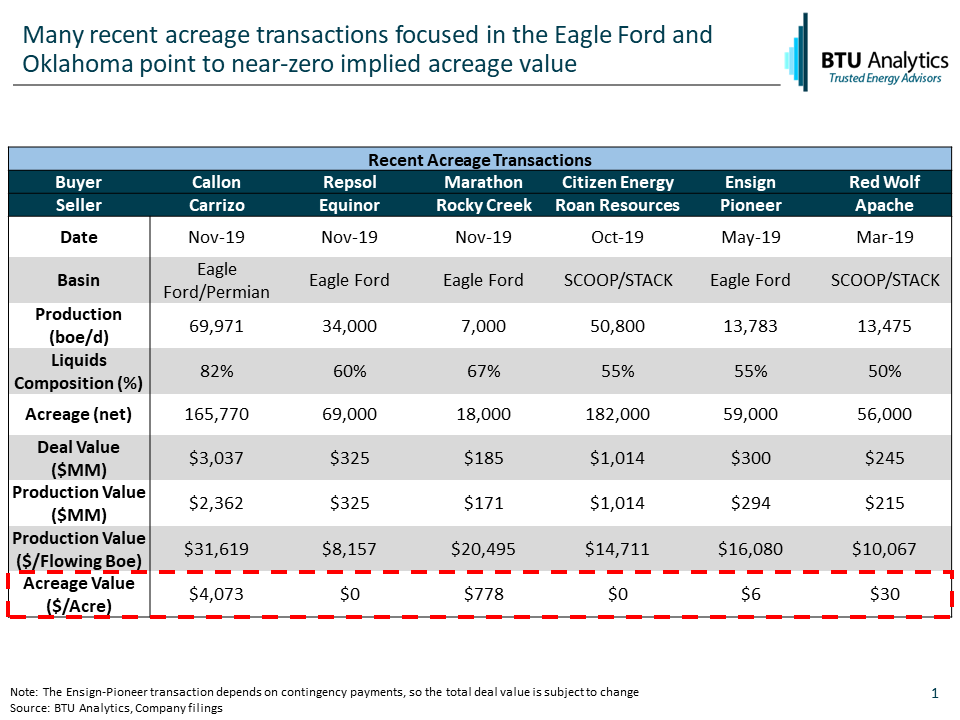

As capital available to E&Ps has dried up throughout 2019, recent acreage transactions have considerably bucked the trend of exorbitant payouts for undrilled acreage. In fact, as highlighted by the table below, numerous transactions have offered little too no value for the acquired acreage, instead relying on the existing production to drive the value of the transaction.

To arrive at these acreage values, BTU Analytics assumed a value for the existing production of oil, natural gas, and NGLs. For most of the transactions, BTU Analytics assumed $45,000 per flowing barrel of oil, $13,500 per flowing barrel of NGLs, and $2,000 per flowing Mcf of natural gas. These multiples drive the value of the existing production, and any value left from the total deal value can then be applied as the net acreage value at the bottom of the table.

These existing production multiples are already depressed from recent years, driven by the decline in commodity prices. However, for the Repsol-Equinor deal, those multiples had to be drastically handicapped in order for the value of the production to at least equal the total deal value. Equinor was likely willing to accept such a low price for this JV acreage given that the acreage had been marketed for some time as well as the company’s size. Smaller E&Ps may not be able to accept such a low price, as the transaction may be needed to fund operations.

For the majority of transactions highlighted above, the resulting acreage value implied in each is far lower than the headline deals of years past. Even after the deal was recently revised lower, Callon Petroleum’s acquisition of Carrizo fetched the largest implied acreage value of deals listed above, which has assets in both the Eagle Ford and Delaware Basin. The value applied to the acreage may be driven by the fact that Permian acreage with significant undrilled locations may still carry significant value. However, given the deteriorating commodity environment highlighted above as well as the large Eagle Ford acreage that Carrizo owns, the acreage value is still far less than recent Permian acquisitions. For comparison to other Delaware Basin deals, Concho’s acquisition of RSP Permian in March 2018 implied more than $75,000/net acre after accounting for existing production.

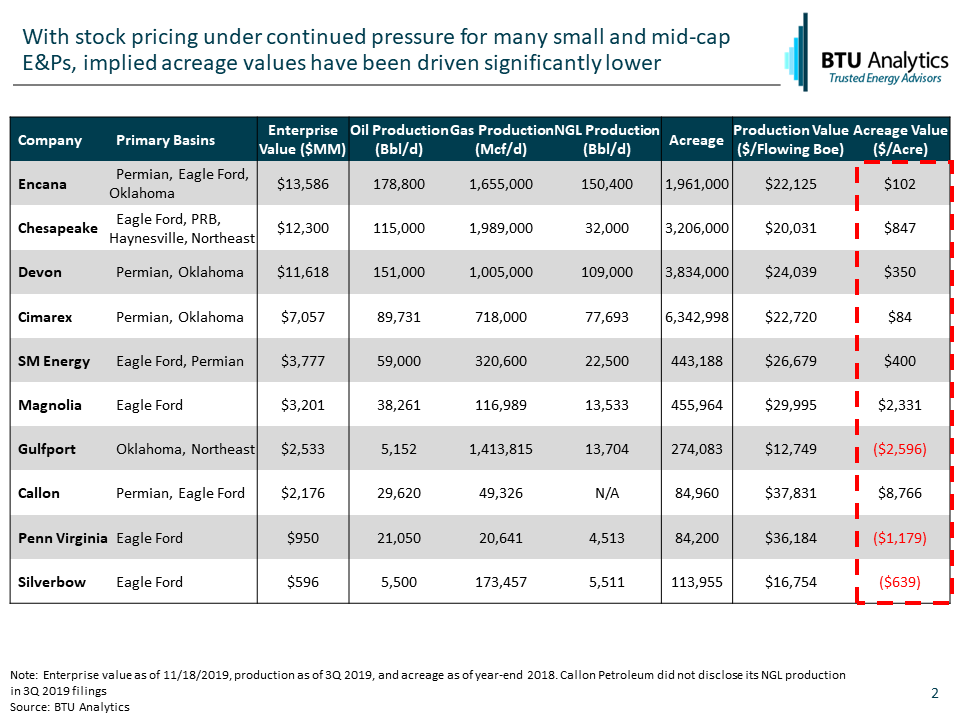

Considering the decline in recent acreage transaction metrics, especially those in the Eagle Ford and Oklahoma highlighted above, the pressure on public E&P stock prices over the last several years has had similar implications on the value of an operators’ undeveloped acreage in the event of an acquisition.

Using the assumptions discussed above concerning the value existing production, the table below breaks down the value of each public E&P by existing production and implied acreage value. The list of companies was chosen because each has significant operations in either the Eagle Ford or Oklahoma, but excludes large companies like Marathon, ExxonMobil, EOG, and Continental. The value for current production and undeveloped acreage is based on the current enterprise value of the E&P, which is comprised of debt plus the current market value of the equity, less cash on hand.

Assuming no premium to each company’s stock price, the resulting acreage values look similar to that seen in the recent acreage deals highlighted above. Three companies (Gulfport, Penn Virginia, and Silverbow) are trading below the value of their existing production based on the multiples discussed above. This could be occurring for multiple reasons, including that the existing production of these companies could decline rapidly or that there are other concerns with the company in public markets that could cause it to trade at a discount.

Driven by the pressure that has mounted on independent E&P stock prices over the past several years, the current value of acreage that E&Ps once paid staggering amounts for has now been called into question. Recent transactions have pointed to low implied undeveloped acreage values, implying that the undrilled inventory on each asset may not be profitable in today’s commodity environment. Have questions on the runway for a particular region? BTU Analytics analyzes undrilled inventory by breakeven for each major shale basin in the E&P Positioning Report. Request a sample today.