Second quarter earnings season is drifting into the rearview mirror, and we have been busy sifting through earnings calls, presentations, and press releases looking for critical tidbits of information (every quarter, we compile a cliff-notes style earnings summary for about 30 US E&Ps and publish that as part of our US Upstream Outlook). An interesting takeaway from those notes were the planned ramp in wells-to-sales in Q3 for EQT and Antero, with Antero explicitly stating that they plan to turn 65-75 wells online in the third quarter alone. By comparison, Antero turned 51 wells-to-sale in the first two quarters combined. Will an aggressive third quarter Appalachia production surge overwhelm Southwest Appalachia infrastructure?

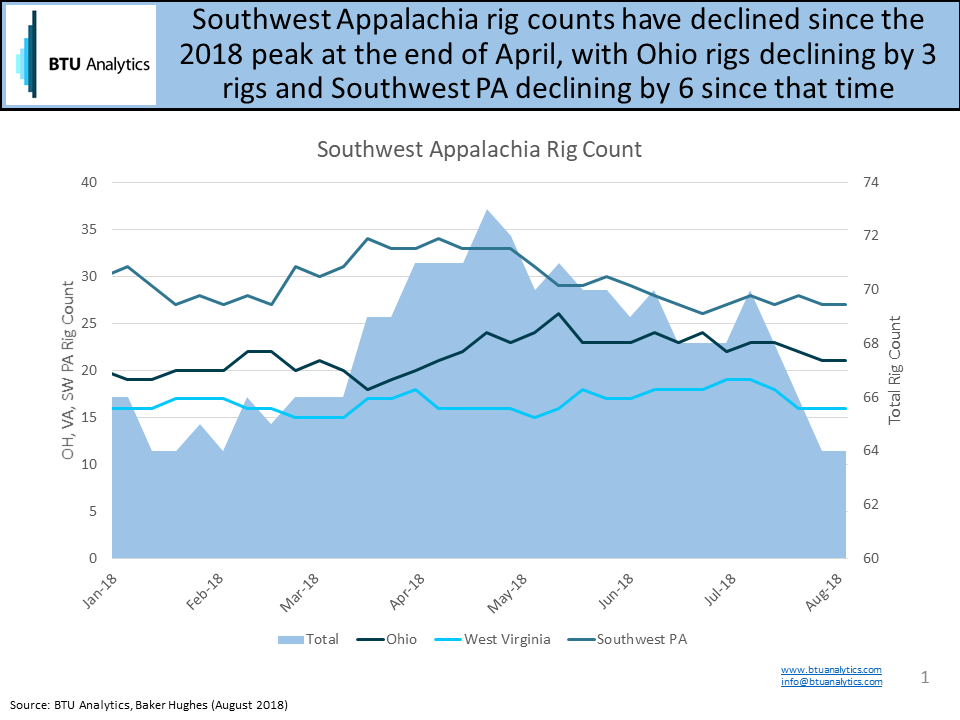

Rig counts in Southwest Appalachia have slumped over the last several months from the peak in April, declining from 65 to 57. As seen in the chart below, Ohio rig counts have remained relatively flat while West Virginia and Southwest PA rig counts have declined from the peak reached in April.

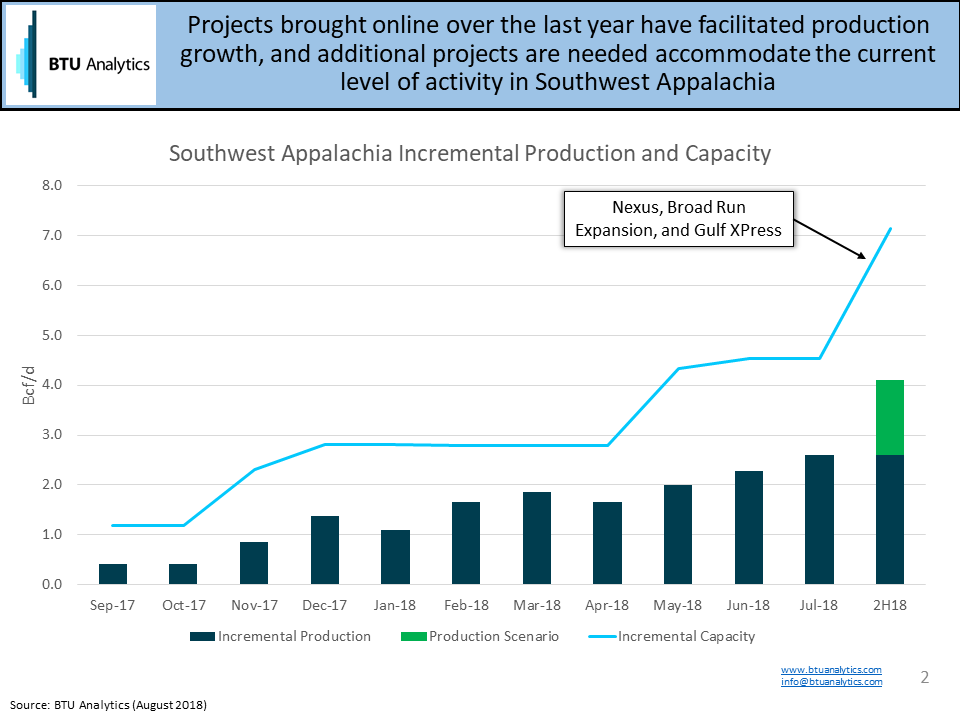

BTU Analytics’ forecast takes into account many real-world factors including infrastructure constraints and hedging, but we also run production scenarios where these constraints are absent. This can be helpful to understand whether activity can be expected to accelerate or decelerate when real-world factors are brought back into the conversation. In a production scenario where today’s current rig count is carried forward along with an increase in wells-to-sales more in line with EQT’s and Antero’s outlooks, production growth could be 1.5 Bcf/d throughout the remainder of 2018.

In June, we published an analysis looking at how Southwest Appalachia production has grown into new capacity and the corresponding impact on prices. The chart below is an update from that publication with the addition of future capacity from Nexus (1.5 Bcf/d), TGP’s Broad Run Expansion (0.2 Bcf/d), and Gulf XPress (0.9 Bcf/d, paired Mountaineer XPress), which are all expected to come online in 2018.

While the chart above seems to confirm that takeaway won’t be a challenge as the gap between incremental production and incremental capacity is nearly 3 Bcf/d for 2H18, those pesky real-world factors can change how reality plays out. As we discussed in the analysis published last week, Antero’s wells have been materially more productive than the average producer in West Virginia, so actual production growth could have additional upside. On the infrastructure side, the possibility of unexpected delays is always present, most recently seen with complete halts to both Atlantic Coast Pipeline (ACP) and Mountain Valley Pipeline (MVP). Rover also continues to face regulatory setbacks – Rover submitted requests in February and May to bring the remaining two laterals online, which would unleash the remaining 0.85 Bcf/d of effective mainline takeaway, but approval has not been granted. Beyond production and infrastructure, demand, pricing, and other factors can lead to different conclusions.

For the latest integrated view on how Southwest Appalachia production and pricing will play out, request more information on BTU’s Northeast Outlook. This month’s publication coming out on August 31 will dive into the implications of ACP and MVP halts, Atlantic Sunrise’s startup, production growth, corridor flows, and more.