Earnings season is here, and with it comes company specific insights as well as occasional perspective on the macro environment. Halliburton (NYSE: HAL) and Schlumberger (NYSE: SLB) commentary is often a bellwether of industry activity, so today BTU Analytics dives in to see what signals two of the largest oil service companies are sending to the market.

While overall the rebound in the North American market has benefited service companies over the last two years, there is significant concern around both the short-term and long-term viability of the prominent US plays in the most recent earning announcements.

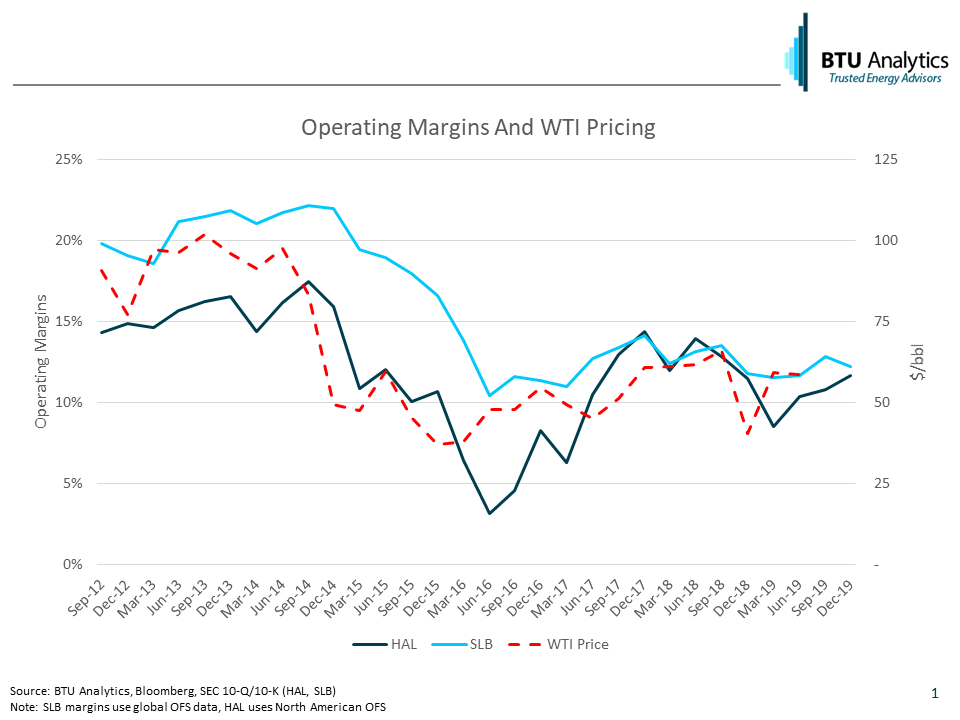

Additionally, the strong run of improving operating margins over the last couple of years has begun to slow. The chart below shows operating margins for HAL and SLB through 3Q 2018. Operating margins have been trending mostly flat since 4Q 2017. Slowing North American activity during the third quarter caused some service pricing weakness for HAL and SLB, and some of the challenges being faced over the next 12 months could mean that operating margins may not see improvement back to the 16% – 22% range seen in 2014.

In the short term, both companies are feeling the effects of infrastructure impacting their clients. SLB stated that the takeaway constraints out of the Permian Basin have led to lower activity in their hydraulic fracturing business which placed pressure on their 3Q performance. Halliburton also saw some customers defer completions due to takeaway issues, however, companies with firm capacity have continued to complete wells and maintain activity in the Permian.

Slower activity is expected to persist through 4Q, with operators pulling back through the end of the year due to both takeaway issues and budget exhaustion. Both companies see the current slowdown to be temporary and predict that WTI prices remaining in the $70/Bbl range will allow for larger budgets and encourage strong operator activity in 2019.

The pullback in activity across the US is consistent with BTU’s current well forecast, shown below. Increases in total US Wells to Sale activity have begun to slow, with BTU calling for 3Q 2018 to be the peak of completion activity until later in 2019 when many of the pipeline takeaway issues are resolved. Drilling activity is forecasted to remain higher than completions throughout this time frame, and for basins such as the Permian, it could result in a significant build-up of DUCs (drilled uncompleted wells) over the next few months. While service companies are hoping that activity will pick up in early 2019, BTU sees challenges which could push higher completions out until later in the year.

What are those challenges and what risks does BTU Analytics see to future activity levels? For more insight into BTU’s views, request a sample of the US Upstream Outlook report.