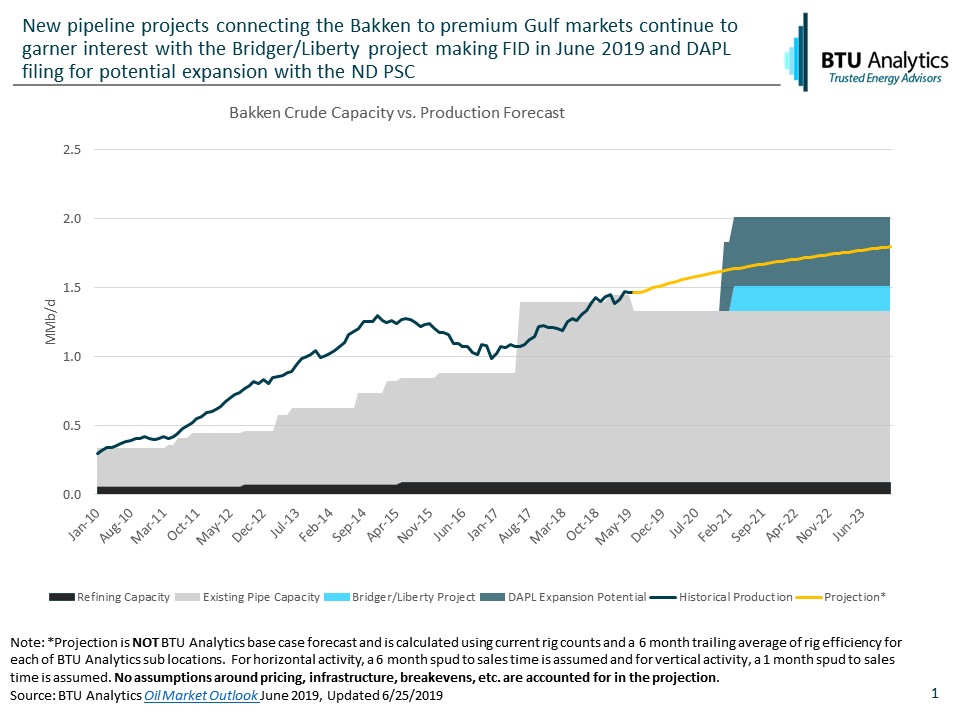

Bakken oil pipeline capacity has become incredibly dynamic as companies attempt to capitalize on production momentum. On June 10, Liberty Pipeline, a JV project between TrueCo’s Bridger pipeline and Phillips 66, announced completion of a successful open season to move forward with the project. The project will have 0.35 MMb/d of capacity with up to 0.175 MMb/d earmarked to serve the Bakken. Then, Energy Transfer filed for a potential expansion of Dakota Access Pipeline (DAPL) from its current 0.6 MMb/d of capacity to up to 1.1 MMb/d. An open season has yet to be announced and ultimate capacity of DAPL is still yet to be determined, but these two project announcements beg the question, “Is more Bakken oil pipeline capacity necessary?”.

Currently, Bakken oil production stands at 1.4 MMb/d. In June, 55 horizontal rigs were actively drilling wells, down from a 2019 peak in April of 59 rigs. Assuming the current rig count remains flat in perpetuity, Bakken oil production could reach as high as 1.8 MMb/d by the end of 2023. The projection shown below also assumes operators are able to maintain current well productivity over that same time frame. Currently, existing Bakken oil pipeline capacity and local refining are just over 1.3 MMb/d. Thus if supply follows the projection, there would be approximately 0.5 MMb/d of potential volumes in 2023 to move on a rail or new pipeline capacity out of the region.

Under this unconstrained scenario, the completion of 0.175 MMb/d of Bakken capacity on Liberty Pipeline and a full 0.5 MMb/d expansion of DAPL, sets the Bakken up to have excess pipeline capacity from the region. However, DAPL could phase in expansions limiting the risk of excess capacity. So, what do you have to believe to achieve a higher production outlook, and what is the risk that activity in the Bakken falls from current levels and grows less?

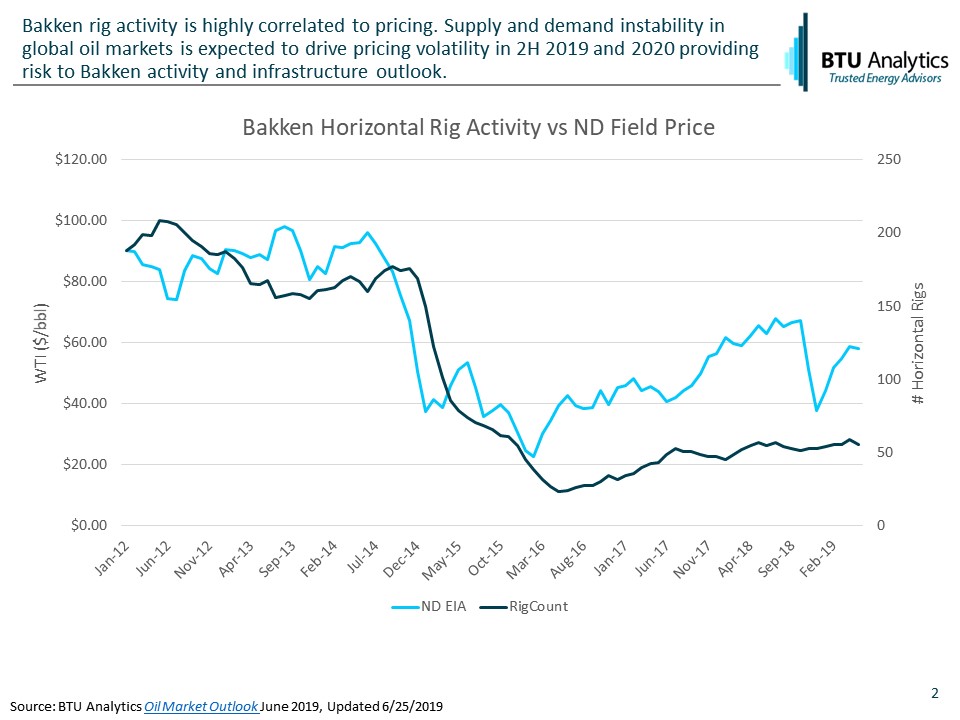

As part of our production forecasting process, BTU Analytics considers infrastructure, supply/demand balances, prices, breakevens, remaining drilling locations, and several other factors. In depth analysis of these variables impacts how production evolves in a given region, and in the Bakken, several of these align to create headwinds to significant long-term production growth. In addition to concerns around infrastructure shortages and low-cost inventory runway, of significant concern, especially in the next 12 months, is oil prices.

The Bakken is an area that remains responsive and sensitive to price fluctuations, especially below $60/bbl wellhead. With 80% of drilling activity conducted by public E&Ps, producers need to be responsive to oil prices to appease public investors that have become highly critical of capital outspend. Overall, the global oil market is poised to be extremely long if OPEC+ does not continue to extend its production cuts through 2020. This, paired with concerns around global oil demand growth due to increasing trade tensions and economic slowdown, has continued to pressure oil prices and could have long term effects on Bakken production growth.

For example, a ~10% drop in rig activity from 55 rigs to 50, results in Bakken reaching 1.65 MMb/d in 2023, a drop of 130 Mb/d compared to the projection of current activity. A second scenario where rigs decline by 10 to levels seen in 2017 when in-basin pricing averaged $51/bbl, would result in a significant difference of production remaining relatively flat to current production levels of just over 1.4 MMb/d. Both scenarios likely leave the Bakken with pipeline winners and losers. For in-depth production and pipeline analysis that accounts for not only oil prices but also other variables driving the evolution of Bakken production and the impacts of Liberty and DAPL, request a sample of our Upstream Outlook and Oil Market Outlook reports.