In Fall 2014, in an elevator in downtown Denver, I overheard two energy professionals lamenting at the time what they thought were weak oil, gas, and NGL prices. One commented to the other, ‘keep calm and frac on’ as I thought to myself ‘this will not end well’. Here we are over a year later and as this week has demonstrated, with every energy equity and commodity screen bleeding red, the correction is not over and too much ‘frac’ing on’ has only contributed to the over-supplied situation.

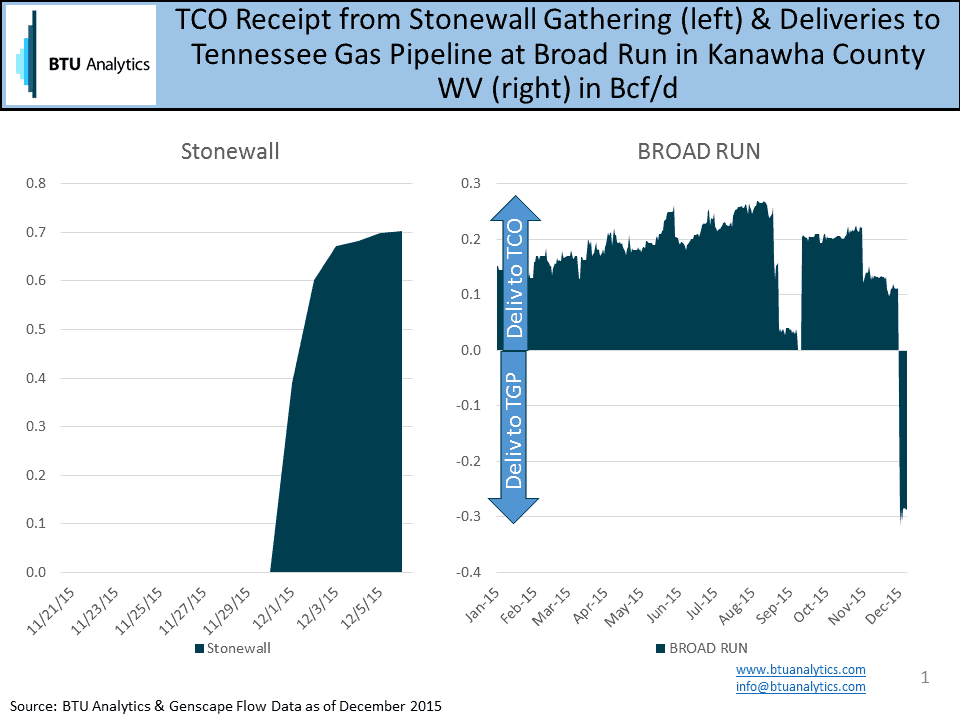

Last Thursday, December 3, 2015 total Marcellus and Utica production hit a new all-time high at 18.7 Bcf/d using a Genscape interstate pipeline flow sample for PA, WV, and OH. As has been the case in 2015, Northeast production has mostly moved sideways as the market has been waiting for new pipeline capacity. New capacity is what ushered in this new record as the Momentum Midstream Stonewall gathering system went into service on December 1 and is now delivering about 700 MMcf/d into Columbia Gas (TCO) in Braxton County, WV. At the same time, the TCO Broad Run meter flipped from receiving 100 MMcf/d from Tennessee Gas Pipeline (TGP) to TCO and is now delivering about 300 MMcf/d to TGP as shown below.

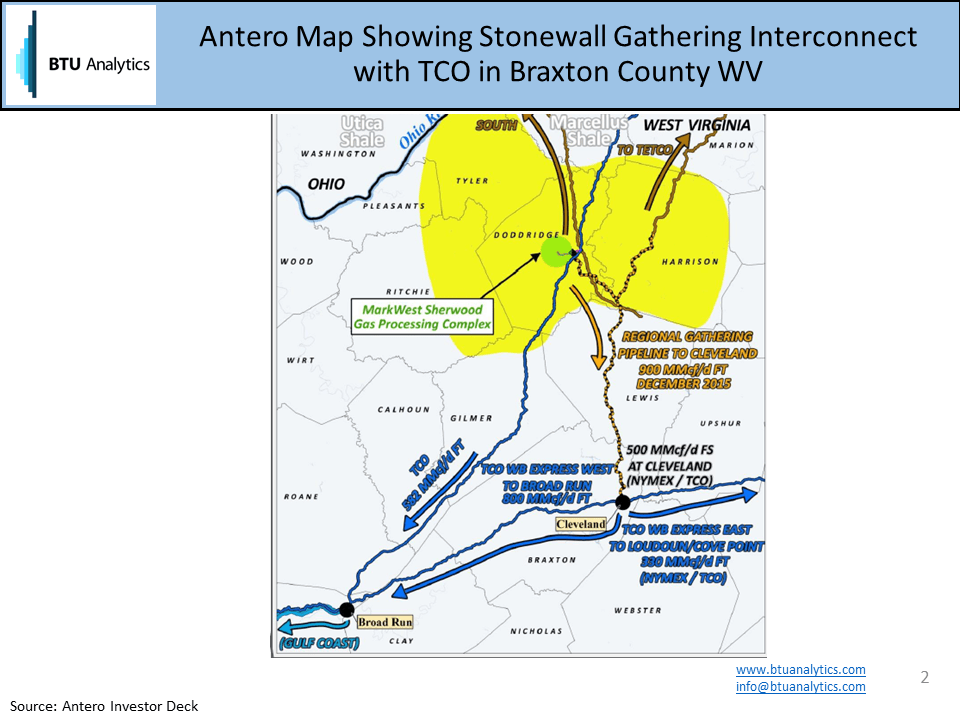

Below is a map from an Antero Resources (NYSE: AR) 2015 investor deck showing the route of the gathering system, the location of Broad Run, and where Antero expected the new volumes to flow.

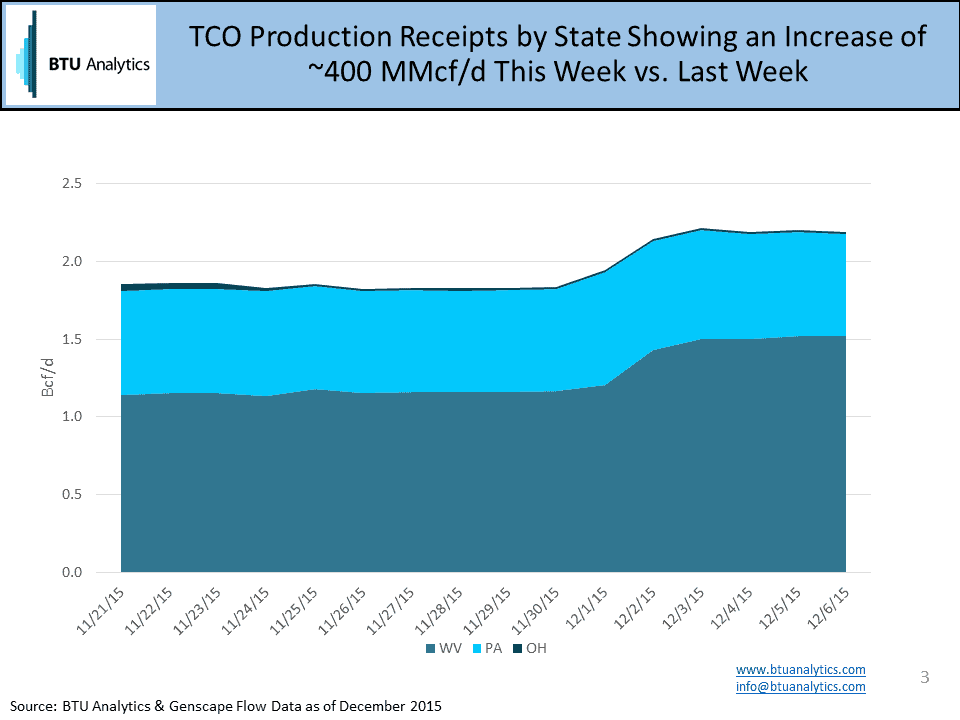

As the Broad Run meter shows, there has been a swing of about 400 MMcf/d in flows at that meter. While the Stonewall meter shows 700 MMcf/d delivered to TCO, several other production meters on TCO dropped when Stonewall started service. In addition, the ETC Northeast gathering system started service the same day as Stonewall and is moving incremental volume to TCO and Dominion in WV. If we look at TCO production receipts we see about a 400 MMcf/d increase week-over-week as a result of Stonewall and Broad Run coming into service – see below.

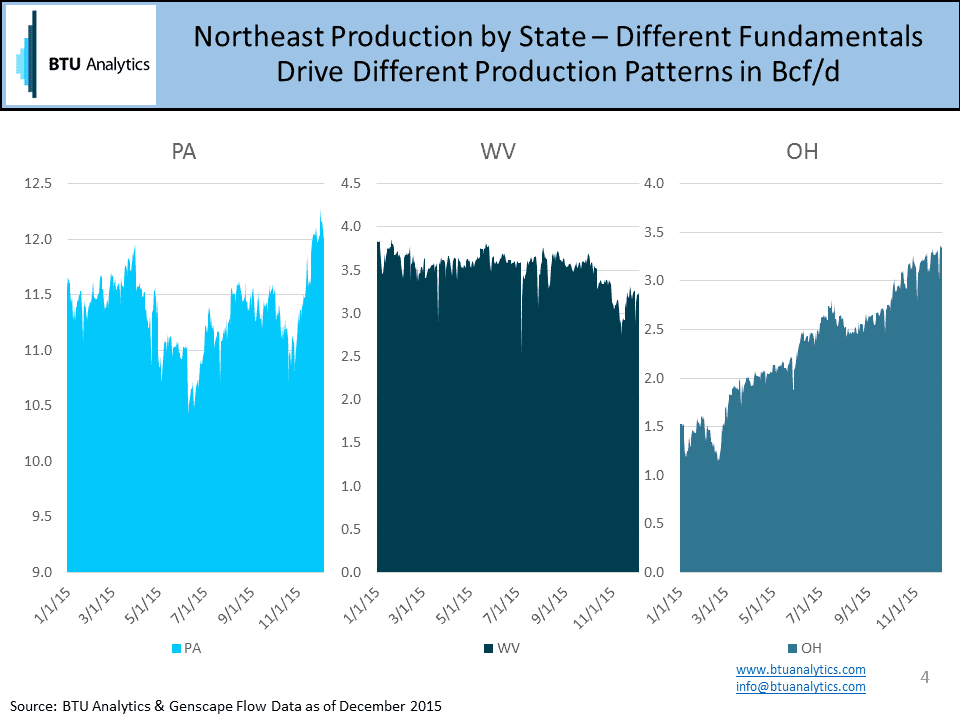

Back to my ‘keep calm and frac on’ friends. The North American oil and natural gas markets are still struggling to rebalance despite a prolonged period of weak prices in 2015. Prices may need to go lower and stay there for longer to get the necessary response. However, some parts of the market are starting to show signs of responding. BTU Analytics has cut Bcf upon Bcf of associated gas production out our forecast outside the Northeast and we still see Northeast supply meeting large chunks of incremental demand in the US through 2020. Below is Northeast production by state which can be characterized (moving from left to right) by Pennsylvania – moving sideways waiting for new capacity, West Virginia responding to weak wet gas economics, and Ohio with the REX reversal growing like there is no commodity correction going on at all. For more information on how BTU Analytics tracks changes in the Northeast Gas Market, request a sample of BTU Analytics Northeast Gas Quarterly and be sure to attend our upcoming conference, What Lies Ahead, taking place February 4th in Houston, TX.