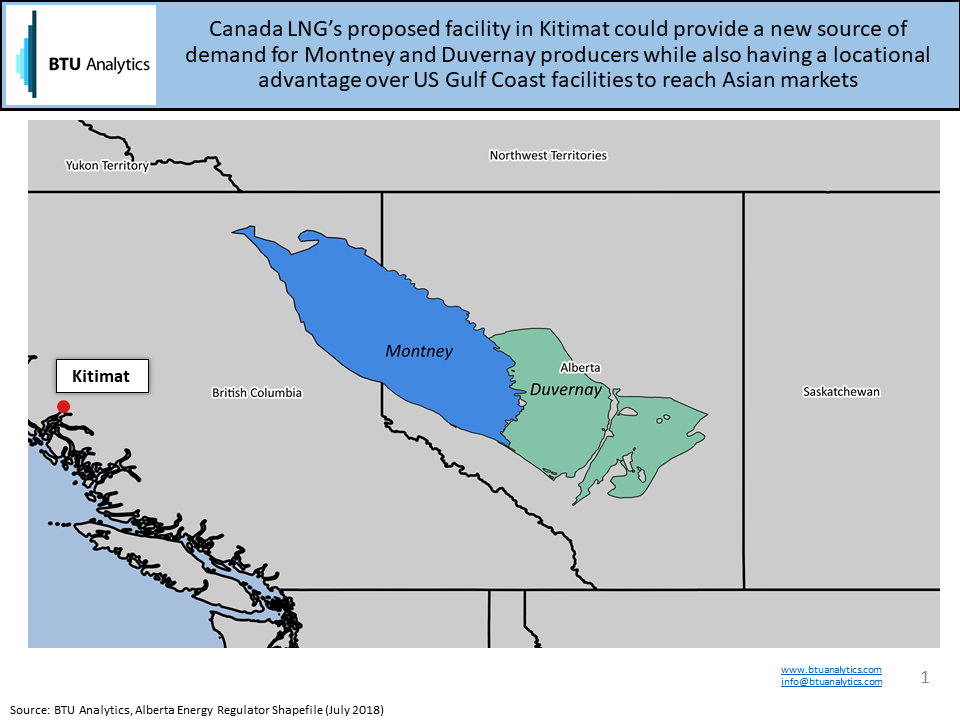

To date, North American LNG export projects have mainly been a US-focused story with Sabine Pass and Cove Point loading cargoes and four other projects set to come at least partially online by 2020. However, Canadian LNG export projects are gaining traction as LNG market pricing improves while Western Canadian gas markets continue facing depressed pricing. Over the last couple of months, the chances of a 2018 FID for the Canada LNG Kitimat project appear to be improving. The 1.75 – 3.50 Bcf/d project rivals Sabine Pass’s capacity and would be located relatively close to the prolific Montney and Duvernay fields in Western Canada.

Canada LNG is hardly the only proposed project looking to export cargoes out of Western Canada. The Canadian government currently lists 20 proposed projects with 34 Bcf/d of cumulative capacity. 14 of the 20 projects (81% of capacity, 27.5 Bcf/d) are located on British Columbia’s West Coast. These projects would have locational advantages (direct route to Asia versus US Gulf Coast exports that must travel through the Panama Canal) to reach premium and growing Asian markets. According to the May 2018, FERC Landed Prices report, Korea and China had the two highest landed prices in the world, and both KOGAS and PetroChina are part of the Canada LNG joint venture.

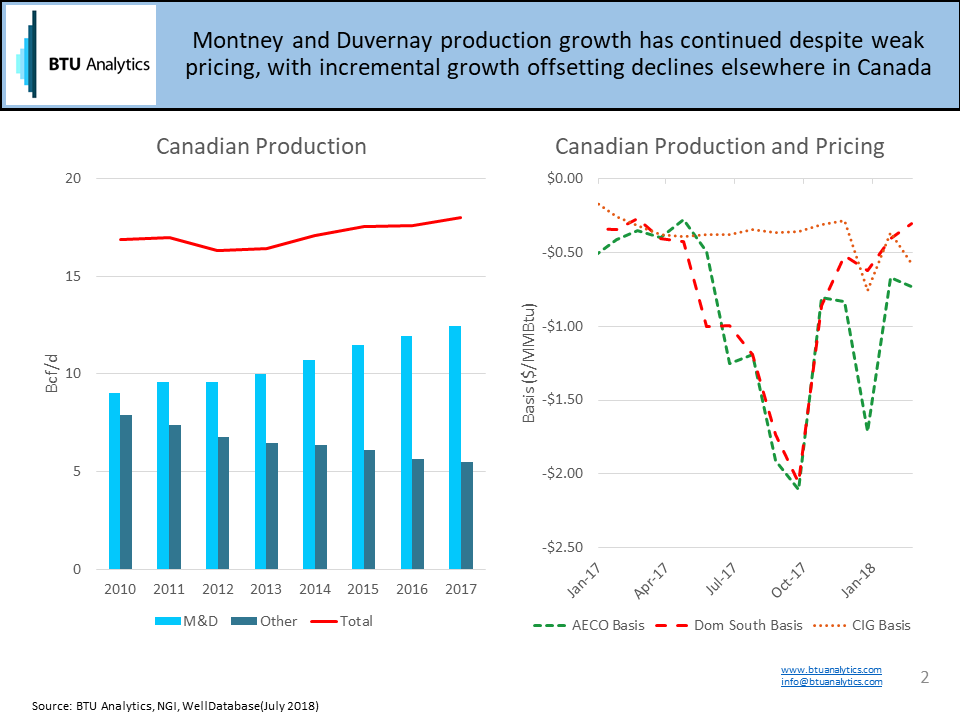

Besides shorter shipping routes, Western Canadian facilities would also be located adjacent to the plentiful gas resources in the Montney and Duvernay. Recent production growth in Canada has come out a relatively small geographic footprint in the Montney and Duvernay while other plays have been flat or declining (chart on left below). Currently, gas produced there must be transported long distances to serve West Coast, Midwest, or East Coast US demand, often forcing AECO to sell into US markets at depressed prices (chart on right below). The lack of proximity to demand alongside congestion in the NGTL system has put pressure on Montney and Duvernay producers, but production growth has continued nonetheless.

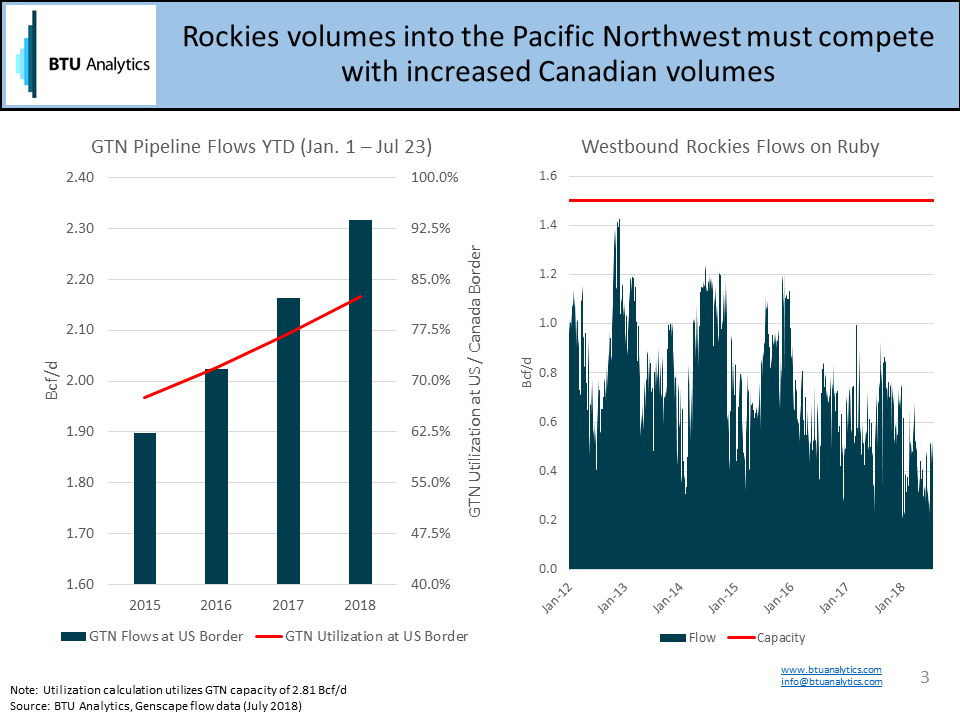

For US operators, Canadian production and pricing are important factors to monitor because Montney and Duverney dynamics have downstream impacts on US producers. For example, growing Western Canadian volume has resulted in more gas moving along GTN towards Northern California (chart on left below), with Rockies gas being displaced along Ruby (chart on right below), helping place incremental pressure on Rockies prices (chart on right above). While these flow dynamics are likely to change as US pipeline infrastructure comes to fruition, the key takeaway is that AECO volumes currently have no other option besides selling into US markets at depressed prices, but LNG export facilities along Canada’s West Coast could change that relationship.

Kitimat is likely still 5+ years away from commercial service, but it could signal the beginning of a new wave of LNG projects that could shift the North American supply and demand landscape. Rockies producers, for example, could benefit long-term from increased West Coast LNG projects. Check out our latest insights into how the second wave of LNG will impact the mid-2020s and beyond with the Long Term Gas Outlook or subscribe to the Henry Hub Outlook to keep up to date on how the first wave of LNG projects will impact the market over the next several years.