On Tuesday, the Trans Mountain pipeline expansion, a pipeline project that would carry an additional 590 Mb/d of crude oil from Edmonton, Alberta to Burnaby, British Columbia, outside of Vancouver, was approved by the Canadian federal government. Once completed, this project will provide much needed relief to the congested crude oil pipeline system out of Canada. Pipelines are so full that Western Canadian Select (WCS) prices fell to a low of $13.46/bbl last November, prompting the Alberta government to introduce a production curtailment program at the start of 2019. While this project will help provide relief to oil takeaway constraints in western Canada, it is not expected to come online until at least mid-2022. Two other major pipeline projects that could provide relief to the Canadian constraint, Enbridge’s (NYSE: ENB) Line 3 Replacement and TC Energy’s (NYSE: TRP) Keystone XL, are facing delays in the United States. In the meantime, crude by rail will play a significant role in transporting Canadian oil production. Today’s Energy Market Commentary will take a look at how crude by rail transportation has been affected by the curtailment program in Alberta and what role crude by rail might play until additional pipeline capacity is available to carry Canadian crude.

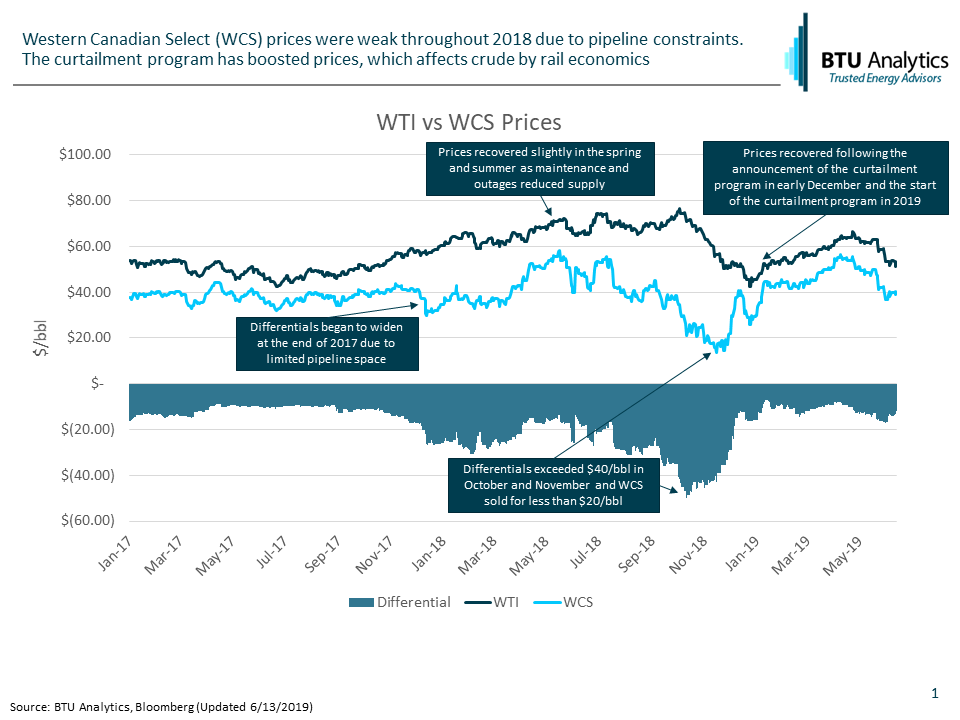

Canada’s benchmark crude oil price, Western Canadian Select (WCS), typically trades at a discount to WTI. The chart below shows the relationship between the two prices over time. In 2018, the differential between the two began to widen, driven by apportionment of pipeline capacity on the Enbridge Mainline. Throughout the year, oil production increased but pipelines remained full, resulting in storage inventories of 35 MMbbls, more than twice normal levels. The differential between WTI and WCS widened, even more, reaching over $40/bbl in November with outright WCS prices below $20/bbl. At the beginning of December, the Alberta government announced a mandatory production curtailment program to reduce the storage glut that had developed and improve prices. Following the announcement, WCS prices improved significantly and differentials have started to fall back in line with where they were before 2018.

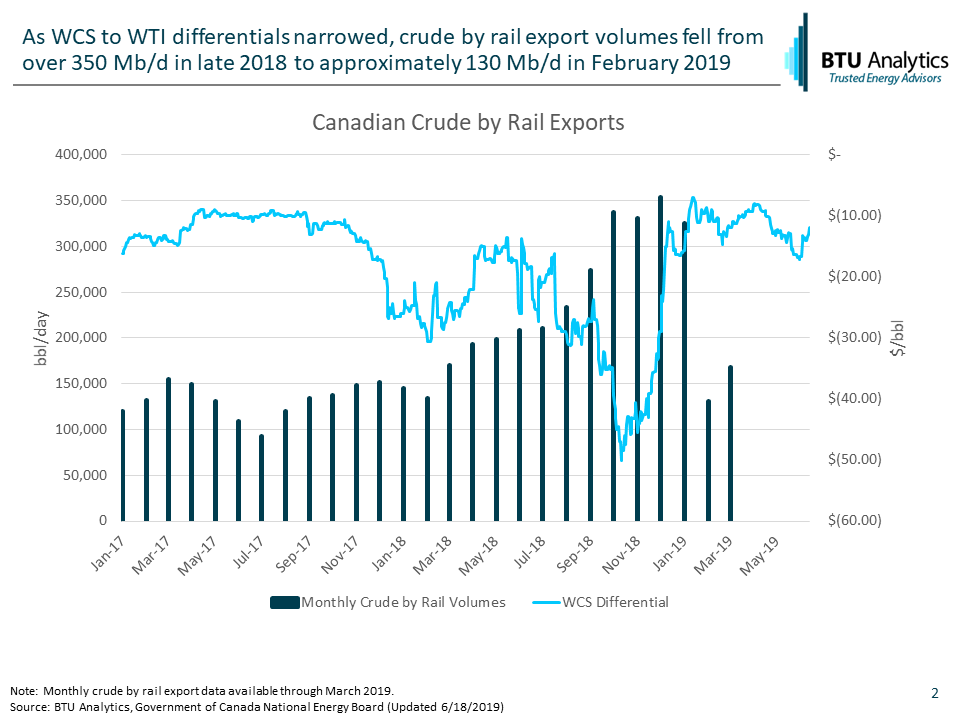

Differentials play an important role in crude by rail economics. Moving crude by rail costs more than transporting it via pipeline, and Canadian crude, in particular, requires heated rail cars, of which there are fewer than traditional rail cars. The chart below shows crude by rail volumes and the differential between WCS and WTI. Throughout 2018, crude by rail volumes more than doubled. Full pipelines and wide differentials made transporting crude by rail a good option for getting oil to market. By the end of 2018, crude by rail volumes exceeded 350 Mb/d. However, with the announcement and start of the curtailment program and the narrowing of differentials to below $10/bbl, moving crude by rail became uneconomic and volumes quickly dropped off. Differentials have started to widen back to pre-2018 levels, and crude by rail volumes for March, the most recent available data, suggest that exports by rail have stopped falling.

The previous Alberta government signed rail contracts to increase crude by rail capacity by 120,000 b/d by mid-2020. The new government, elected in April, is in talks to have producers take over those contracts. Regardless of who holds the contracts, the government, or producers, additional crude by rail capacity is coming. Given recent delays for Enbridge’s Line 3 replacement, the new government has mentioned possibly extending the curtailment program past 2019, with a goal of keeping the differential wide enough to incentivize crude by rail shipments but small enough that there is still value for the Alberta government. Until new pipeline capacity is available, WCS-WTI differentials and crude by rail will play an important role in transporting Canadian crude production. To stay up to date on BTU Analytics’ views on WTI and WCS pricing, request a copy of our Oil Market Outlook, which includes forecasts for those price points as well as other price points across the US.