As we talked about last March, initial capital expenditure (capex) budgets announced by public E&Ps for the upcoming year can provide a good benchmark for how they are currently thinking about their assets. When compiled together, the budgets offer insight into the trajectory of a region’s production. However, those budgets can change. In our most recent Upstream Outlook, we analyzed how the capital budgets of some of the largest public independents changed for 2019 and the impact on our production outlook. Today’s Energy Market Commentary will provide an overview of currently planned capital spending in 2019.

On average, E&Ps in our sample increased their drilling and completion (D&C) budgets by 10% compared to initial plans throughout 2018. Higher commodity prices drove management teams to accelerate capital spending. That exuberance didn’t last. Following a $30 price correction to finish 2018, E&Ps highlighted capital discipline and a decline in capex for 2019. Now that we’ve taken a closer look at these capex plans for 2019, what trends do we notice?

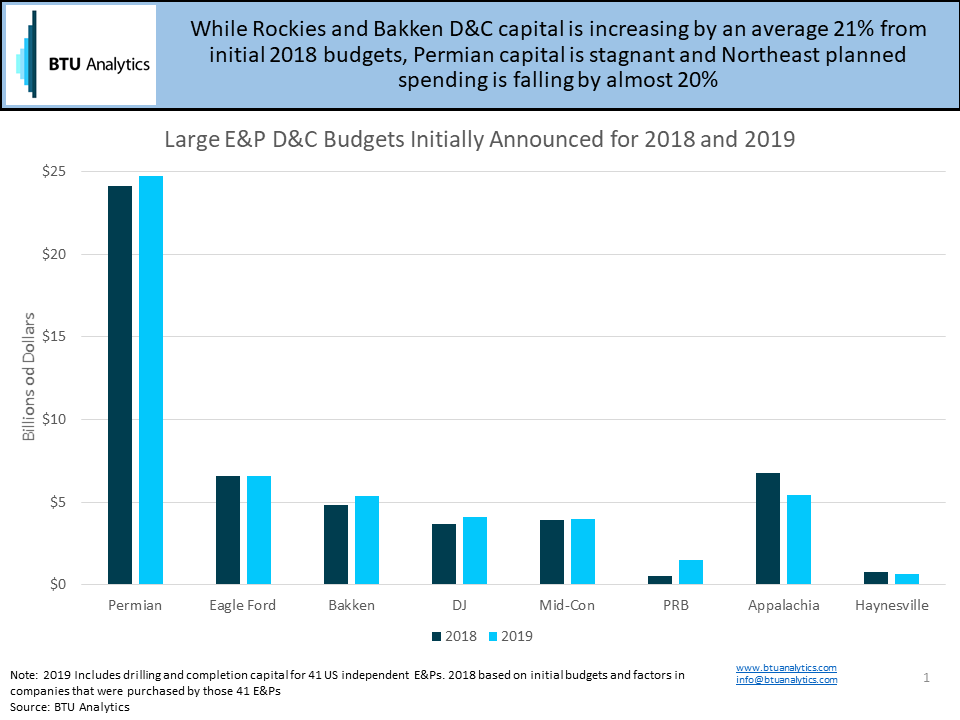

In short, planned 2019 US onshore D&C spending for 41 E&Ps looks about the same as it did when 2018 budgets were announced a year ago. Those 41 E&Ps represent about 44% of current horizontal rig activity. However, compared to actual capital spending for 2018 this subset of independents is planning to put less capital in the ground in 2019.

How this capital is distributed between major basins varies considerably. The chart below shows the cumulative drilling and completion budgets for 41 E&Ps (and the companies they have since acquired) initially announced for both 2018 and 2019. Planned capital spending in 2019 increased by an average 6% for liquids plays compared to initial 2018 capital plans. However, planned spending in the natural gas regions of Appalachia and the Haynesville is almost 20% lower.

Permian D&C Spending Flat in 2019

While initial D&C plans in the Rockies and Bakken saw sizable increases between 2018 and 2019, Permian spending is relatively consistent. This is far from a signal of slowing Permian momentum.

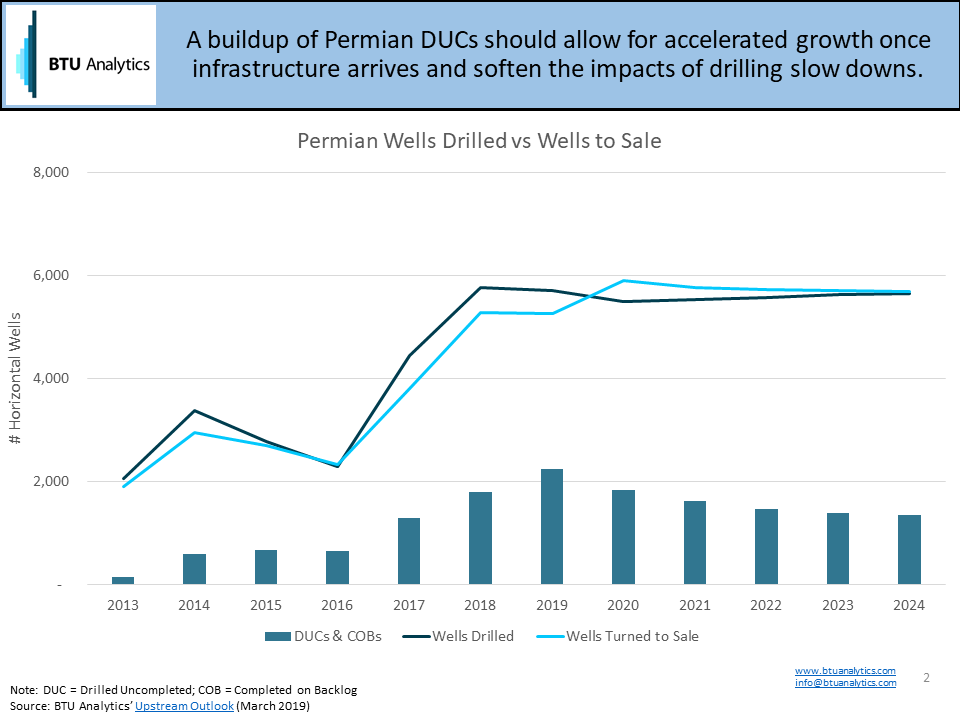

As a result of Permian infrastructure bottlenecks, the Permian has compiled a large backlog of drilled but uncompleted wells (DUCs) over the past few years, as shown by the chart below. Producer capital spending is falling from its peak but also where the dollars are being spent is changing. In order to conserve capital, operators will cut drilling in 1H2019 and then increase completion activity in 2H2019. The slowing in drilling and subsequent uptick in completions will result in eventual decline in the number of DUCs in the Permian. Many of these DUCs were drilled in 2018 or before, offering producers a way to reduce spending, but still fuel growth in 2019 and 2020.

Northeast Capex Decline

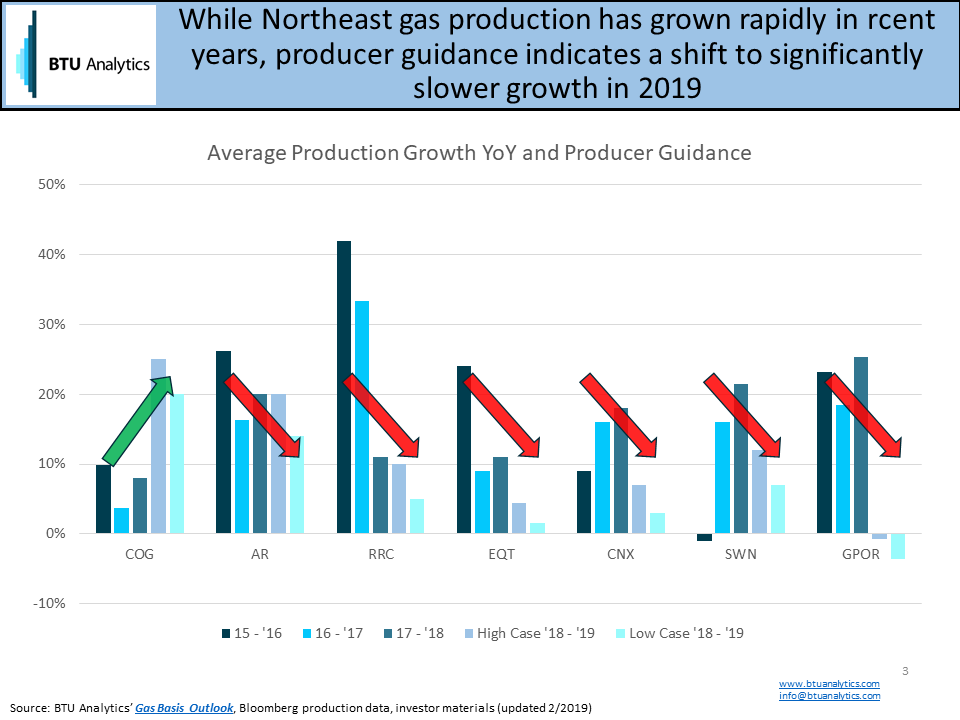

In the Northeast, production growth is likely to be more impacted by the substantial decline in planned E&P capex spending. BTU has consistently called for a slowdown in Northeast production growth in our forecasts, as we highlight in our new Gas Basis Outlook. 2019 producer announcements for capex and production growth appear to support that call.

The chart below highlights the 2019 production growth targets for some of the larger public Northeast E&Ps compared to their historical production growth. All of the producers shown below are planning for slowing or even declining production, with the exception of Cabot. Cabot operates in Northeast Pennsylvania and has subscribed pipeline capacity that it is planning to grow into.

While the changes to D&C spending for major E&Ps could translate to shifts in production dynamics across the US, it’s important to note that this is only part of the story. Majors continue to grow their foothold in the unconventional space, especially in the Permian. Additionally, many plays like the Haynesville have a large presence of private operators that do not disclose capital budgets. Capex budgets can also change rapidly, as we saw during 2Q earnings reports last year. With crude prices rising once again, 2019 could prove to be another test for operators to show how disciplined they truly are with their capital.

Keep up to date on BTU Analytics’ views on US natural gas, oil and NGL production by requesting a copy of our Upstream Outlook report.