For the last decade, global oil demand growth has been driven by China, but outlooks differ on whether this dynamic will be maintained going forward. Chinese demand growth forecasts have a 0.5-MMb/d spread between the most bullish and bearish views, with the IEA and OPEC expecting strong growth to continue, while China’s largest national oil company, China National Petroleum Corporation (CNPC), is much more bearish. The IEA and OPEC forecasts may be overly optimistic, as uncertain economic growth, population decline, and lower demand globally for Chinese-made goods may limit the increase in Chinese consumption. If IEA and OPEC forecasts for Chinese demand growth in 2024 do not materialize, their global demand growth scenarios of 1.3 MMb/d and 2.2 MMb/d, respectively, would lead to oversupply on the market.

Economic Risks

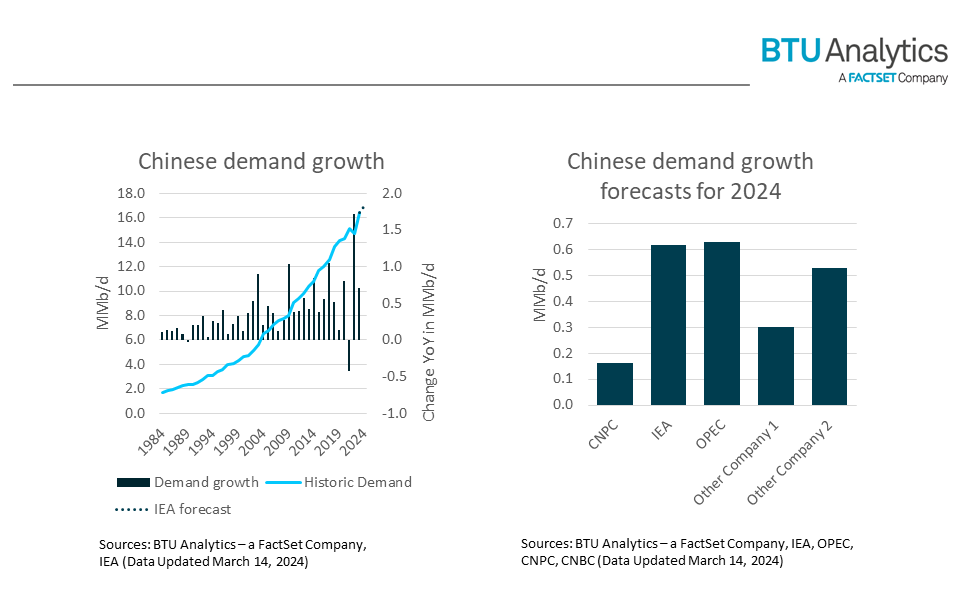

The IEA revised its forecast for 2024 Chinese demand growth down to 618 Mb/d in its latest Oil Market Report, while OPEC is forecasting 2024 growth at 630 Mb/d. In contrast, CNPC recently published a report forecasting demand growth at 161 Mb/d, citing slower growth in refined oil consumption and oil processing in 2024 along with further adoption of EVs. Between 2010 and 2019, Chinese demand growth accounted for about 45% of global demand growth per year on average. In 2024, OPEC and the IEA estimate it at 28% and 46%, respectively.

Historical relationships between GDP growth and demand growth suggest Chinese demand growth would hold flat at around 4% GDP growth. Prior to 2019, to achieve demand growth above 400 Mb/d, Chinese GDP growth needed to be north of 7%. The estimates for Chinese GDP growth in 2024 are narrow, at 4.5–5% among the IMF, World Bank, FactSet Consensus, OPEC and the Chinese government, which has the most bullish forecast.

While China’s economic outlook is uncertain, a struggling property development sector and declining Chinese exports highlight some of the country’s economic risks and calls into question significant GDP growth in 2024. Also, according to the National Bureau of Statistics, China’s population decreased for a second consecutive year in 2023 and the country’s birth rate is at a new low. The IMF is forecasting another small decline for population growth in 2024, which may also put downward pressure on demand growth.

Oil Demand Risks

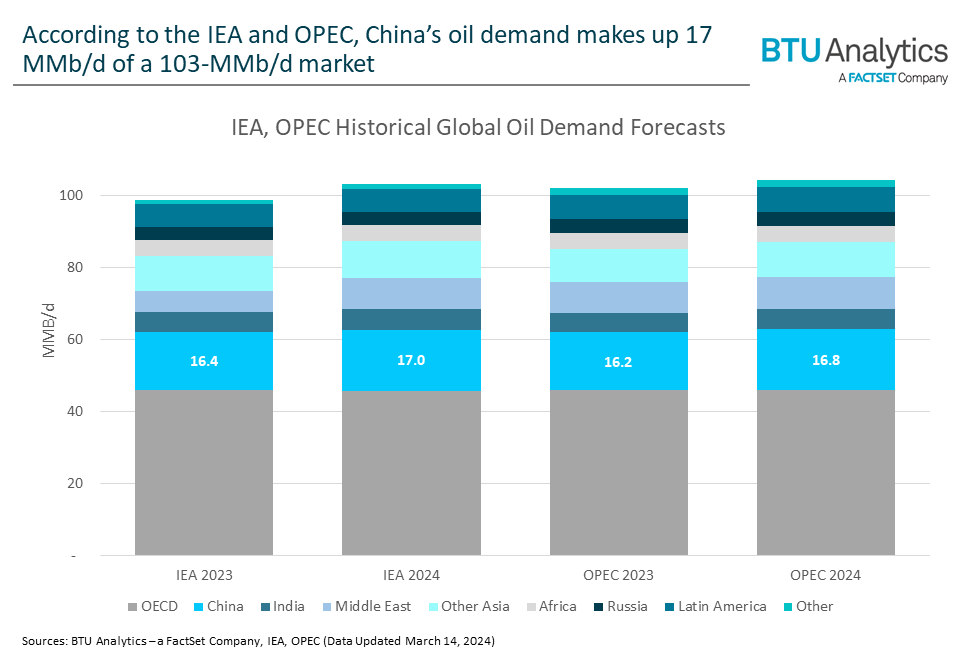

The IEA and OPEC use China as the major source of global demand growth for 2024, contributing to their expectations for a historically normal pace of demand growth for the year. But if Chinese demand growth were to come in closer to CNPC’s forecast, the IEA would overestimate global demand growth by as much as 460 Mb/d and bring 2024 growth to below 1 MMb/d.

Lower-than-forecast global demand growth and production increases in the U.S., Brazil, and Guyana in 2024 skew global market imbalance risks toward an oversupplied market. The IEA recently changed its 2024 forecast from a deficit to a surplus, hinged on OPEC+ keeping its cuts in place and having high compliance through 2024. The uncertainty of Chinese demand growth, a market trending toward oversupply, and concerns over OPEC+ maintaining cohesion through a sticky price environment point toward the risk range for benchmark crude prices being skewed to the downside through the remainder of the year. For more details on BTU Analytics’ global oil forecasts, be sure to check out our Oil Market Outlook.