Recent cold-temperature spikes across the U.S. have lifted near-term pricing after an extremely weak December. Last week, winter storms Gerri and Heather sent Henry Hub surging above $13/MMBtu, the highest daily average price for the U.S. natural gas benchmark since Winter Storm Uri in 2021. However, the impact of mild weather in December and the swing to colder temperatures in January hasn’t been limited to Henry Hub. Adding to our recent Energy Market Insight that looked at the effects recent weather had on near-term pricing for both Henry Hub and TTF in Europe, this Energy Market Insight delves into the pricing effects in two winter premium basis markets on either side of the U.S., New England and Southern California.

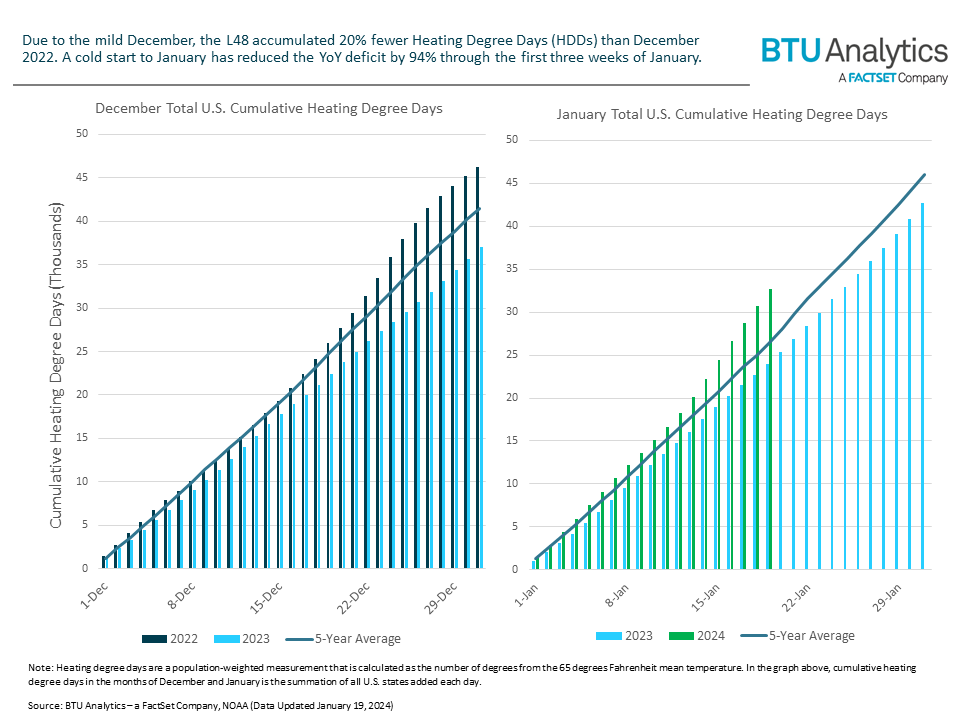

In December 2023, the U.S. accumulated 20% fewer heating degree days (HDDs) than in December of 2022 and 11% fewer than the five-year average. Weaker-than-normal December demand was realized in the national storage withdrawal with a mere 14 Bcf/d of natural gas pulled from storage and the EIA reporting storage at 3.48 Tcf, a five-year-high for the week ending December 29th. Conversely, January month-to-date has produced 23% more cumulative heating degree days than the five-year average, making up for 96% of the December deficit. National storage volumes reflect this change with storage for the week ending January 12th at 3.18 Tcf, representing a 300-Bcf withdrawal over the past two weeks.

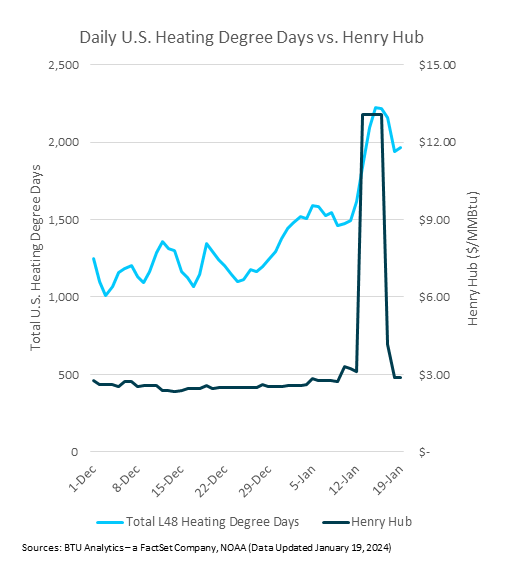

U.S. gas prices have largely reflected the two temperature extremes. Henry Hub remained holistically involatile in December 2023 with an average price of $2.52/MMBtu and a respective maximum and minimum of $2.77/MMBtu and $2.33/MMBtu. Three weeks into January 2024, pricing has been much more volatile with Henry Hub averaging $5.05/MMBtu largely driven by a blowout to $13.08/MMBtu on January 13th due to the polar vortex.

Boston Market

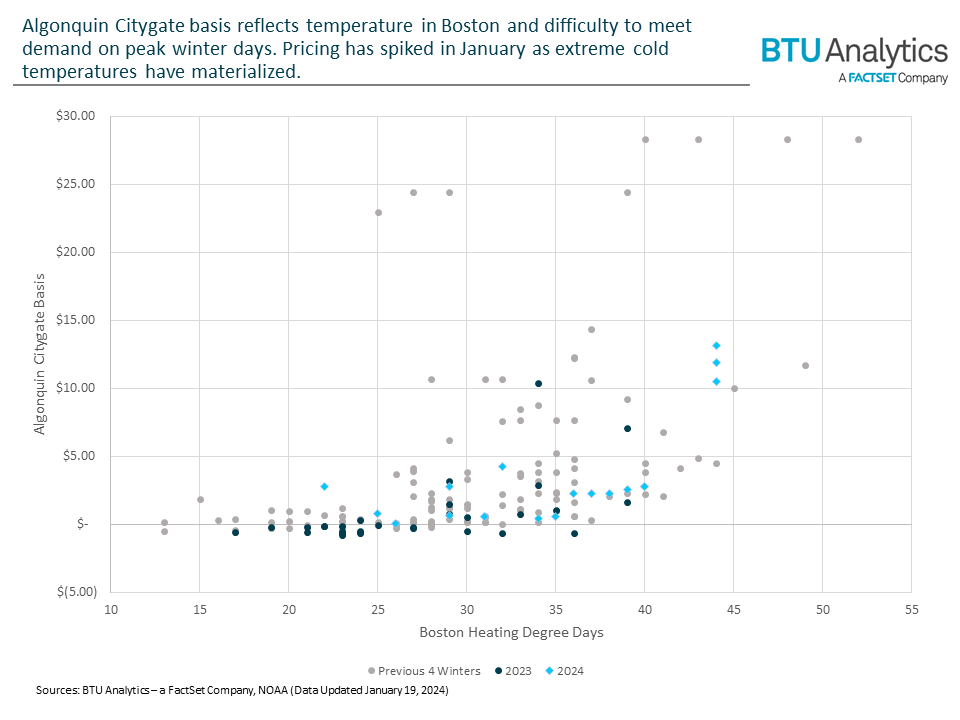

Winter premium basis markets tend to show a strong correlation between temperature and basis. Algonquin Citygate is no exception, as basis consistently reflects cold weather in Boston and the difficulty in meeting demand on peak winter days. Supply is limited by pipeline capacity out of the Northeast, which tends to become constrained during peak winter events. In December, temperatures were simply not cold enough to put pressure on infrastructure constraints and subsequently provided stability for Algonquin pricing with basis averaging a $0.70/MMBtu premium to Henry Hub. However, through the first three weeks of January, Algonquin Citygate basis has strengthened to an average of $3.36/MMBtu.

The chart above illustrates the strong relationship between Algonquin Citygate basis and Boston HDDs. In December 2022, basis blowouts primarily occurred once temperatures exceeded 36 HDDs. Yet, in December 2023, those temperatures broadly failed to materialize with just three distinct days with 36 HDDs or more. However, extreme cold in January has pushed basis back to a significant premium, as the Boston area has already recorded nine days with at least 36 HDDs. Basis has responded accordingly. Algonquin Citygate basis reached as high as $13.12/MMBtu on January 19th and maintained a premium above $10.00/MMBtu for six days over the past two weeks.

Southern California Market

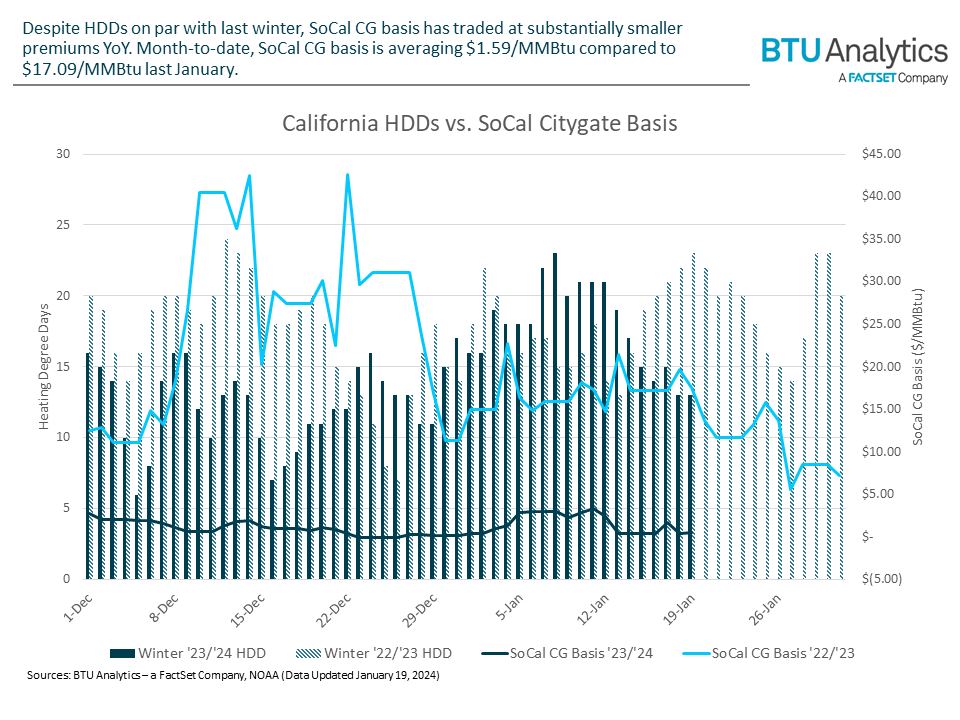

Like New England, Southern California has experienced mild weather through December and into January. However, unlike markets in the North, such as Algonquin Citygate, Southern California’s SoCal Citygate does not follow the traditional temperature-and-price correlation trend, evidenced by the fact that even on days when temperatures were as cold as they were this time last winter, Winter ‘23/’24 basis was significantly weaker.

This is due to infrastructure constraints into the California market that provide limited access from nearby supply hubs. El Paso and Transwestern pipelines are both full out of the Permian, and supply from the Pacific Northwest is constrained at PG&E’s Redwood Path. That leaves Kern River, out of the Rockies, as the marginal supplier of gas into the SoCal market. With cold weather driving an uptick in pricing at Opal (averaging $3.43/MMBtu in January 2024 compared to $0.62/MMBtu in December 2023), SoCal Citygate basis has seen a corresponding increase. Basis is trading at an average of $1.59/MMBtu since the beginning of January compared to averaging $1.03/MMBtu last month.

In short, pricing in the U.S., both at Henry Hub and winter basis markets, was muted by a mild December. However, cold temperatures in the first half of January resulted in stronger basis in premium markets, like Algonquin Citygate. Even markets with mild local weather, like SoCal Citygate, have been affected by increased demand in supply regions, albeit to a lesser degree than northern markets. To the extent that cold weather continues to materialize through the remainder of winter, premium winter markets should continue to realize winter premiums despite an inauspicious start to the season.