On December 23, Enterprise Products Partners (NYSE: EPD) announced that the first cargo of US domestic light sweet was contracted to be loaded in January by Vitol taking 600,000 barrels of crude oil from the US to destinations yet unknown but rumored to be Europe. Within days of the end of the crude export ban, producers found a new market and now the Brent to WTI spread has shifted with WTI a premium to Brent for the 4th time this year (January, June, and November, and December). In each of the previous flips in the spread, WTI premiums remained unsustainable as US production remained strong and US producers were required to price themselves into the stack of the US refining slate. Now with production off its peak levels, new condensate splitters starting up in Corpus and Houston and a global glut of light sweet crude, do crude exports provide any boon to US producers and could it lead to a bust of US refiners?

With WTI now a premium to European markets, as well as the US dollar’s continuing strength, why would global refiners choose to purchase US barrels? And if they do, where are they most likely to purchase them from? To answer those questions, we must understand what drives a refinery’s purchasing decisions because not all crude oil is created equal. Factors influencing refineries purchasing decisions include, but are not limited to:

- Supply stability

- Product consistency (gravity, metals, sulfur content, etc…)

- Distillation yield and resulting crack spread

- Logistics

The US and Canadian markets offer functioning legal systems, highly efficient infrastructure, and liquid futures markets and hundreds of potential counter-parties, something crude sourced from countries like Venezuela or Nigeria can’t match.

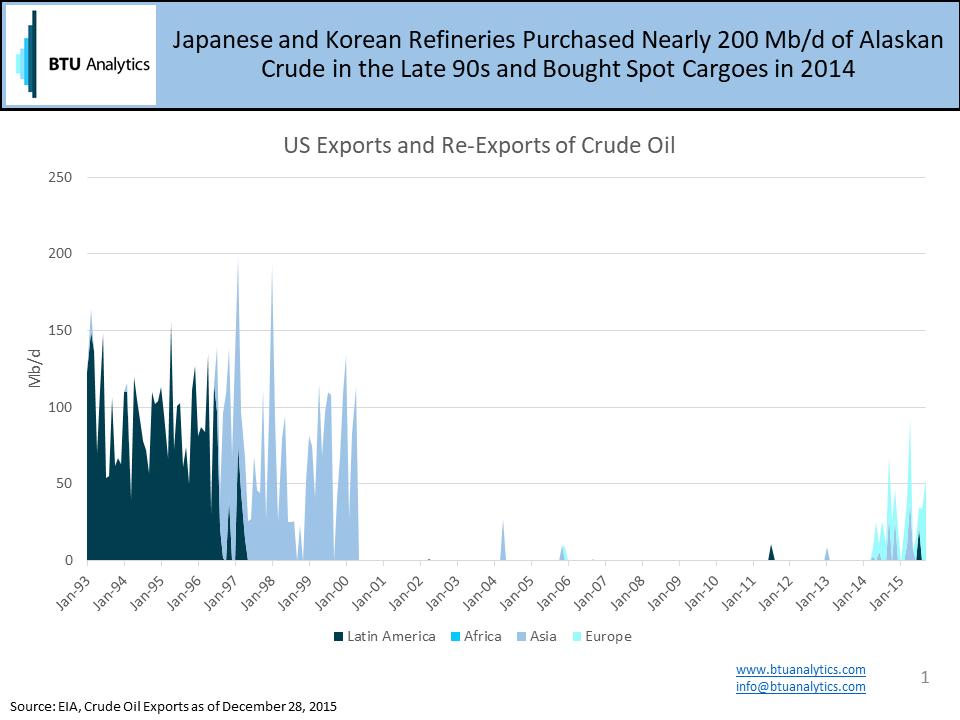

As markets watch for additional Gulf Coast crude exports, we wondered what other opportunities for reliable crude exports from the US might exist and the potential implications to producers, midstream providers, and refiners. Going back in history, Alaska exported ~70 Mb/d of crude oil from 1996-2000 peaking at 193 Mb/d in January 1998.

Exports to Japanese and Korean refiners dried up for 14 years, but in September 2014 ConocoPhillips exported an 800,000 barrel cargo of Alaskan crude to South Korea and an additional cargo was exported in April of 2015. These crude exports were done utilizing higher cost Jones Act vessels that had to utilize inefficient routes to reach the Korean market due to the exemption limitations in the crude oil export ban. If spreads were wide enough in 2014 to justify exports, are spreads still wide enough with the repeal of the ban to incentivize Alaskan barrels to flow to Asia instead of the US West Coast?

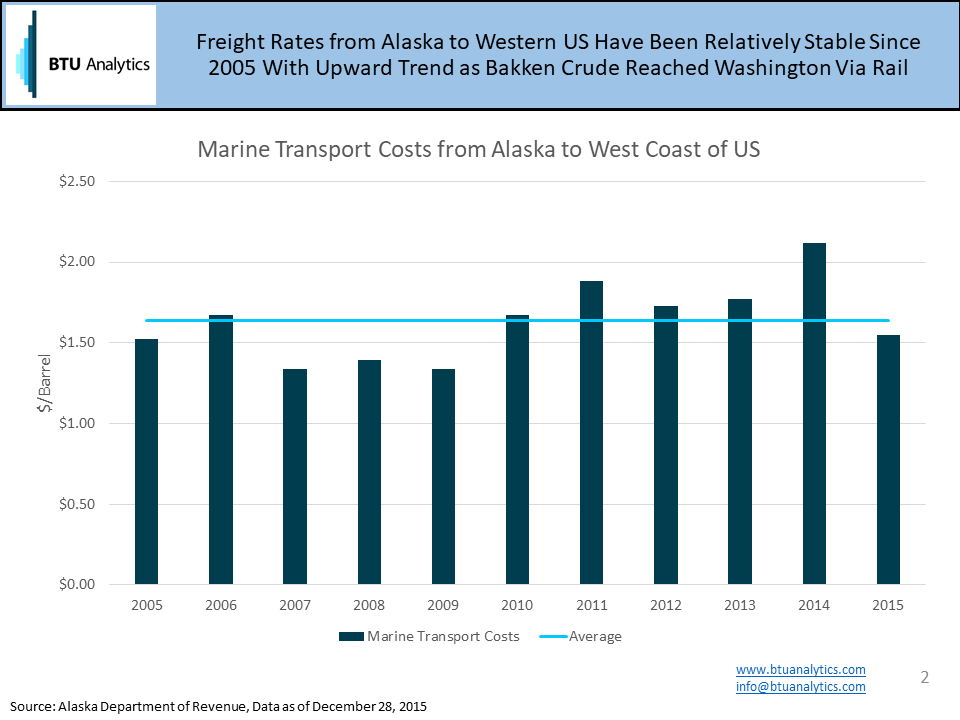

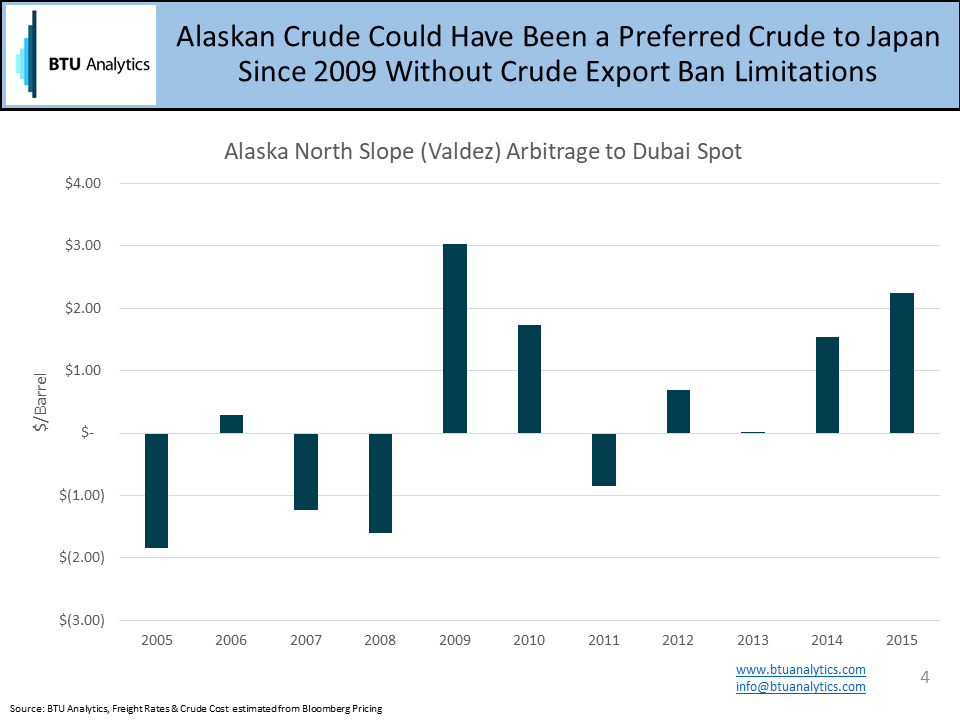

In order to answer that question, we first need to look at the cost of procuring Alaska North Slope Crude (ANS) versus competing grades of similar quality. For this analysis, we selected Arabian Gulf Dubai Fateh spot prices. Both crude oils are an intermediate grade (~31 API) with sulfur contents of ~0.7% and 2% respectively making the pricing between the two crudes fairly comparable not accounting for distillation differences. Since ANS spot cargoes are primarily delivered to refineries located in Washington and California, benchmark pricing for ANS is assessed there. In 2015, ANS on the West Coast averaged $51.74/bbl compared to Dubai crude that averaged $51.44. However, suppliers looking to buy Alaskan crude for export would much rather buy the barrel at Valdez, Alaska rather than from the West Coast, so we need to back out the shipping costs incurred between Valdez and the West Coast utilizing Jones act vessels. The Alaska Department of Revenue provides average costs for shipping to California and Washington refiners.

In 2015, that cost has averaged $1.55 per barrel reducing the acquisition cost of ANS crude to $50.19 giving refiners in Asia a $1.25/barrel advantage in barrels purchased for loading at Valdez over Dubai.

The next step is to factor in the cost of shipping the crude oil to ports in Asia. For our analysis, we picked a single import point, the port of Chiba in Japan, to compare estimated shipping costs. Freight rates, sourced via Bloomberg, for a VLCC in 2015 from the Arab Gulf to Japan averaged $2.19/barrel. While a dirty tanker rate from Valdez to Japan couldn’t be found, one could estimate the cost based on comparative shipping distances. If the ship originated in Dubai and traveled to Chiba, it was would need to travel 6,337 nautical miles compared to a tanker originating in Valdez, which would only travel 3,419 nautical miles, a route that is 46% shorter than originating in Dubai. Assuming the tanker rates are perfectly scale-able to distance, the freight rate from Valdez, Alaska to Chiba, Japan would have only been $1.18/bbl in 2015. Advantaged feed stock costs of $1.25/barrel combined with advantaged logistics costs of $1.01 would boost refinery margins in Chiba, Japan by approximately $2.25/barrel based on 2015 average prices.

The margins to support Alaskan crude export economics appear to be there, and could materially impact volumes previously destined for the US West Coast. For more data and analysis on the ramifications of crude exports and expected impacts to midstream logistics in North America, attend BTU Analytics’ Conference: What Lies Ahead, on February 4, 2016 in Houston.