Across the industry, anxious callers are reaching out to E&P companies looking for reassurance that their investments remain economic even as oil prices continue to fall. We’re taking those calls as well, inquiring where and when we expect to see significant declines in activity.

The answer isn’t quick and concise. Every play has its core area and its fringes. Crude at $100/bbl provided a big tent where everyone was invited to the party to grow production, producers in the core areas and fringe areas alike. The pullback in domestic oil prices has forced producers to talk about re-evaluating development decisions. But will that talk translate into measurable changes in well counts and production any time soon?

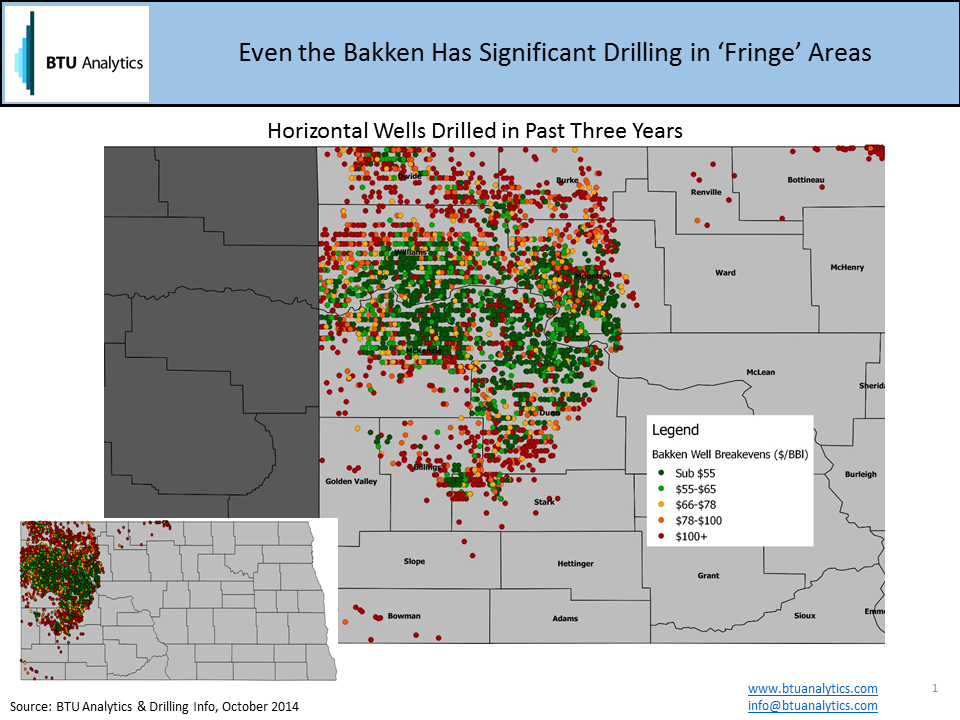

An easy way to visualize the core areas versus the fringe areas is to map estimated breakeven prices, a practice we regularly undertake as part of our consulting work and to inform the production forecasts found in our Upstream Outlook report. The map below shows a simple version of this analysis focusing on the Williston Basin in North Dakota.

In this analysis, we discovered what oil prices gave us a 10% internal rate of return given a natural gas price of $4/MMBtu, and an $8.8MM per well average drilling and completion cost across the basin. In a more complex analysis, we would have adjusted well cost by area, given that well costs vary with formation depth and completion technique both of which meaningfully impact drilling & completion costs.

What stands out? While we often mention Mountrail, McKenzie, Williams and Dunn Counties as the core Bakken, there is a significant variance in well performance across those counties. These oil price breakevens are based on the oil price received at the wellhead. If we assume that transportation out of the basin is another $5 to $10 per barrel, $80 WTI translates to something closer to $72/bbl netbacks to producers.

There is still a significant inventory of wells left to be drilled in the core area of the Bakken to support production growth out of the basin. But producers with fringe acreage could find their cash flows no longer support the growth they expected.

For more detailed information on well economics, drilling inventory and production forecasts, request a sample of BTU Analytics’ Upstream Outlook report.