Entering 2020, with details of a rumored phase 1 trade deal with China swirling, one question became alarmingly clear here at BTU Analytics: how was China actually going to execute on the promised energy product purchase agreements, specifically for oil? Now, just one month later, that question is much more in focus thanks to the havoc that the novel coronavirus has wreaked on Chinese oil demand. Estimates on the impact the outbreak has on Chinese oil demand in 2020 range from as little as 0.2 MMb/d up to more than 1 MMb/d. Today’s Energy Market Commentary will focus on how this new dynamic impacts the likelihood that China lives up to its crude oil purchase agreements.

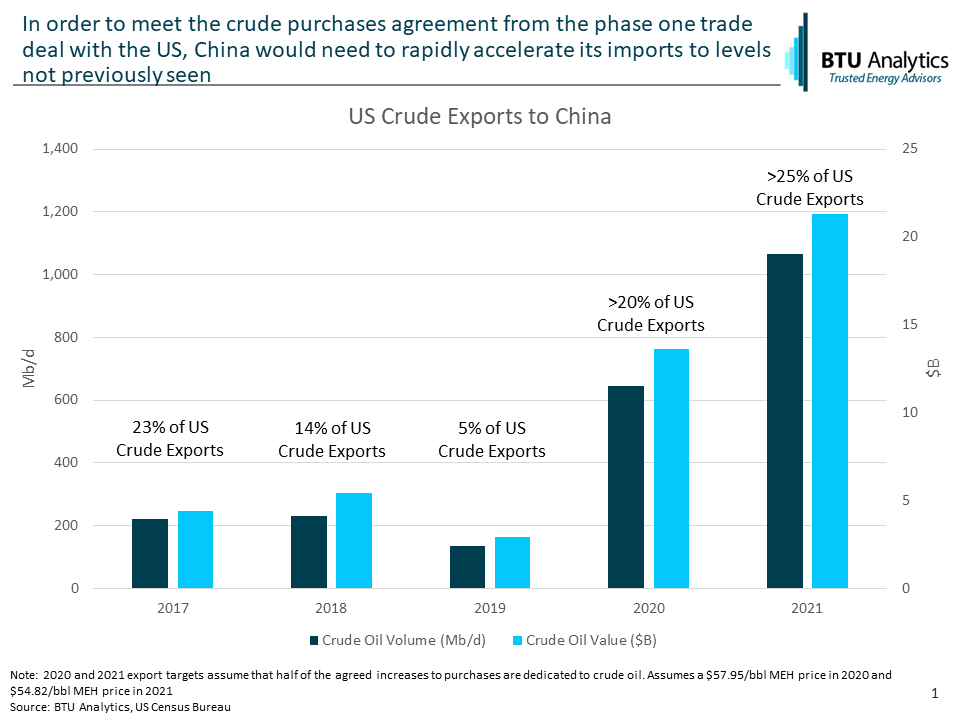

First, let’s estimate the amount of crude that China would need to import to fulfill its 2020 import agreement. In the phase one deal, China and the US agreed that China would increase 2020 purchases of US energy products (crude oil, LNG, refined products, and coal) by $18.5 billion above a 2017 baseline of approximately $8.5 billion, as well as increase 2021 purchases by $33.9 billion above the 2017 baseline. For simplicity’s sake in this analysis, we assume that at least half of these increases will need to be served by crude oil, as illustrated by the chart below. In 2017, China imported an average 222 Mb/d from the US for a total value of $4.38 billion, implying an average price of $54/bbl. Considering that Magellan East Houston pricing averaged $53.50 over this time period and the majority of crude exports from the US will leave from either Port Arthur/Beaumont, Houston, or Corpus Christi, we will use BTU Analytics’ Houston pricing forecast for our proxy for the value of crude exported, which is featured in the monthly Oil Market Outlook. With an average MEH price of just under $58/bbl in 2020, the US would need to export nearly 644 Mb/d to China in 2020, nearly triple the 2017 level. This figure then increases to 1,066 Mb/d to meet the 2021 agreements.

The most oil that the US has ever sent to China on a monthly basis was 475 Mb/d in October 2017, or roughly 30% of all US crude exports that month. For the 2020 target to be met, Chinese exports would represent more than 20% of what BTU Analytics estimates will be exported in total for the year.

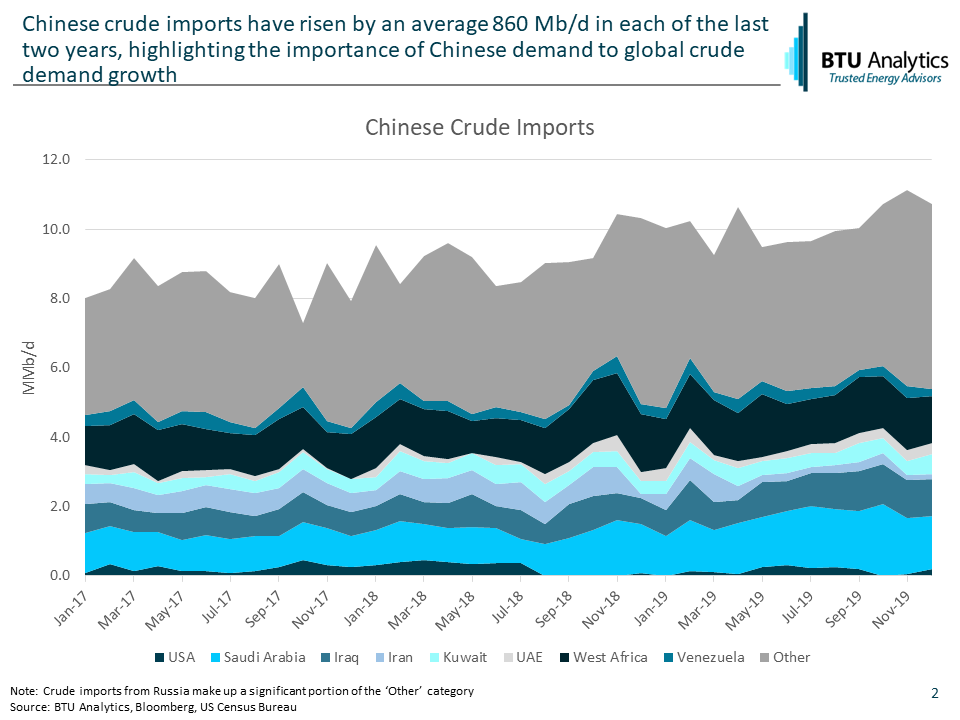

However, whether the US ends up sending all this crude to China isn’t really the point considering recent events. Could China even take all this crude without rapidly filling storage tanks? To answer this question, we will need to consider how much crude oil China currently imports, how those imports may be affected by the coronavirus outbreak, where China currently sources its crude from, and which of those sources are displaceable by US crude. As shown in the chart below, China imported roughly 10 MMb/d of crude oil in 2019. Considering that China’s oil production has held flat in recent years, any increase in imports likely corresponds to an increase in demand.

China has increased oil demand by an average 860 Mb/d each of the last two years. With China’s economy already slowing, let’s assume that Chinese oil demand would have increased by 500 Mb/d in 2020 without the impact of the coronavirus outbreak. Now factoring a moderate potential impact of the coronavirus, a 500 Mb/d deduction to Chinese oil demand, 2020 demand would remain flat to 2019 levels. This would mean that average 2020 crude imports in China would need to fall by nearly 600 Mb/d from December levels of 10.6 MMb/d. This is all while imports from the US are growing by 500 Mb/d, meaning that non-US countries would need to decrease exports to China by a combined 1.1 MMb/d, and therefore give up market share in the most important crude market in the world.

Who might give up this market share? First, it’s important to note that Saudi Arabia is currently discussing deepening production cuts by an additional 600 Mb/d. While Saudi Arabia typically sends its heavier crudes to China (as opposed to the US’s light, sweet crude), the cuts would help balance the overall picture. However, these additional cuts are likely to only be a short-term impact while global pricing markets remain heavily focused on Chinese oil demand. Apart from Saudi production cuts, the most logical displaceable crude grades are those out of West Africa, which exported an average of 1.5 MMb/d to China in 2019.

Whether or not this displacement actually occurs is yet to be seen, but significant oil market disruptions are necessary for phase one US-China trade deal to ring true. Not to mention the tariffs that still weigh on US crude headed to China, which was reduced this morning from 5% to 2.5%. What is equally as important is how the US chooses to respond if China falls short of its energy product purchase agreements. How do the potential impacts of the coronavirus fit into the broader crude market, and how might global supply disruptions help buoy markets? The answers to these questions and more can be found in BTU Analytics’ monthly publication of the Oil Market Outlook. Also, the February edition of the Upstream Outlook will contain a deeper dive into global liquids markets and how China fits into that picture. Click the above links above to receive more information on these reports.