It wasn’t that long ago that US midstream companies were vying to attract customer commitments to new US Gulf Coast crude oil export terminals. For much of 2018 and the 1H2019, Brent to WTI spreads averaged between $7 to $10/bbl primarily because of US export capacity, located mainly in Houston and Port Arthur, reaching capacity. With spreads wide and an outlook for robust US oil production growth, over 18 MMb/d of new crude oil export project proposals flooded the market. However, the upheaval caused by COVID has whittled down this list to just 7 MMb/d of deep-water projects with pending applications with the US Maritime Administration (MARAD). Now, the outlook for US production growth is much more muted compared to outlooks in 2019. BTU Analytics expects only 2.1 MMb/d of incremental US production by 2026 compared to average 2019 levels. Today’s energy market insight will explore the competitive positioning for both new and existing export terminals and the potential for winners and losers in the race to develop new export capacity.

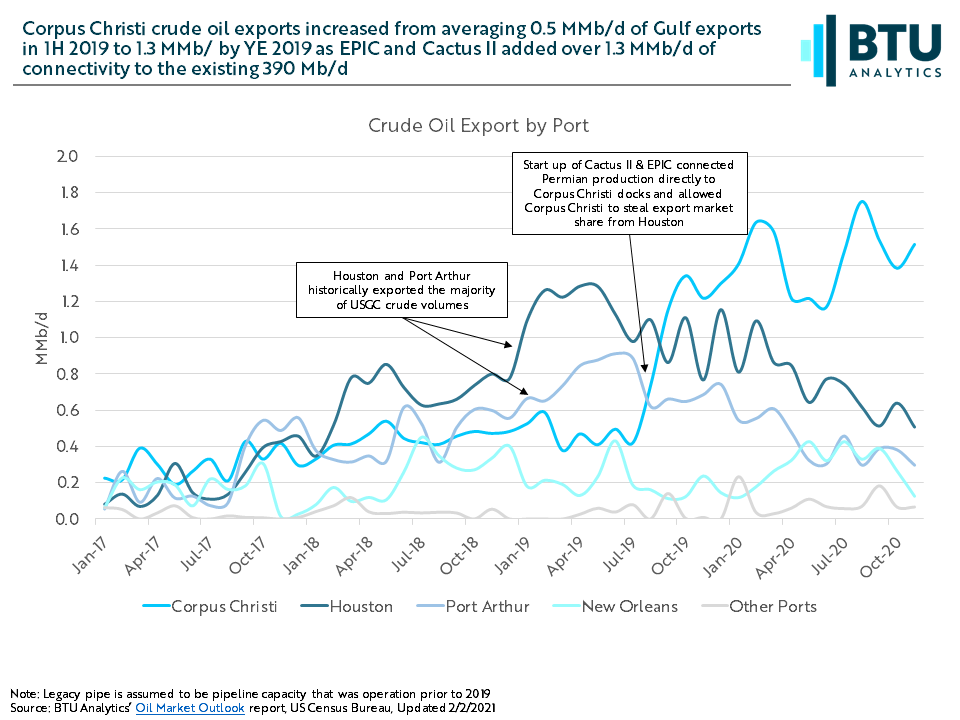

Prior to 2H 2019, Houston and Port Arthur were the primary points of crude oil export from the US. Both ports benefited from access to existing pipeline and dock infrastructure due to historically importing large amounts of crude to support the Houston and Midcontinent refining markets prior to the US shale boom. Together, these ports accounted for almost 2 MMb/d or 73% of Gulf Coast oil exports in 1H 2019. However, the completion of EPIC and Cactus II changed Gulf Coast crude export dynamics. The two new pipelines connected the Permian Basin to Corpus Christi and new export terminals. As a result, Houston and Port Arthur lost both volumes and market share. Exports from Houston and Port Arthur averaged 1.8 MMb/d or 60% of USGC exports in 2H 2019. Conversely, Corpus Christi doubled its share of the USGC export market from 17% to 34% between 1H 2019 and 2H 2019. Furthermore, by November 2020, Corpus Christi exported 1.5 MMb/d of crude oil compared to 800 Mb/d out of Houston and Port Arthur. The chart below highlights US Crude oil exports by Port.

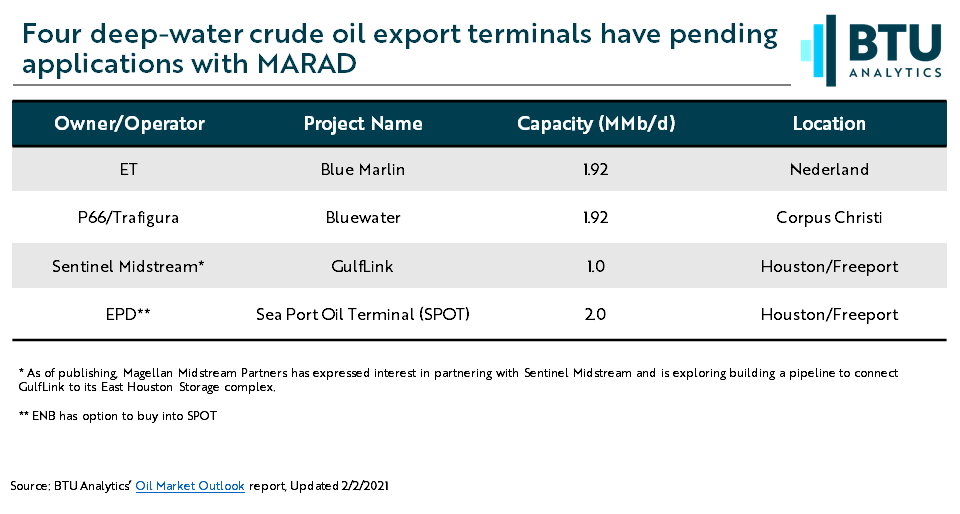

Except for LOOP in LA, there are currently no other deep-water ports in the Gulf Coast. Due to their ability to load larger volumes quickly to VLCCs, deep-water ports can potentially offer lower costs for crude going to export. In a bid to regain market share, three out of four proposed deep-water projects with pending applications with MARAD are proposed for the Houston and Port Arthur markets near existing pipeline and storage assets for several of the companies. The fourth is proposed for additional capacity at Corpus Christi and would also be supported by existing pipeline assets.

While Corpus Christi exports took market share from Houston in 2H 2019, owners and interested joint parties in the export projects for Houston are taking steps to increase project competitiveness via more than just pipeline and storage interconnects. For example, Magellan and Enterprise recently announced that they plan to create a single futures contract for physical delivery in the Houston area after two years of maintaining separate contracts. Enterprise is an owner of the proposed SPOT terminal. Meanwhile, Magellan has expressed interest in partnering with Sentinel to provide a direct connection to the GulfLink export terminal.

Increased trading liquidity alone is not likely to reverse trends in market share. Production volumes first need to rebound. In the interim, terminal operators may have to develop lower cost deep-water connections to reverse trends in market share. For more on BTU Analytics’ outlook on crude oil exports, oil pipeline flows, and price forecasts for key US Benchmarks and Brent request a sample of our Oil Market Outlook Report.