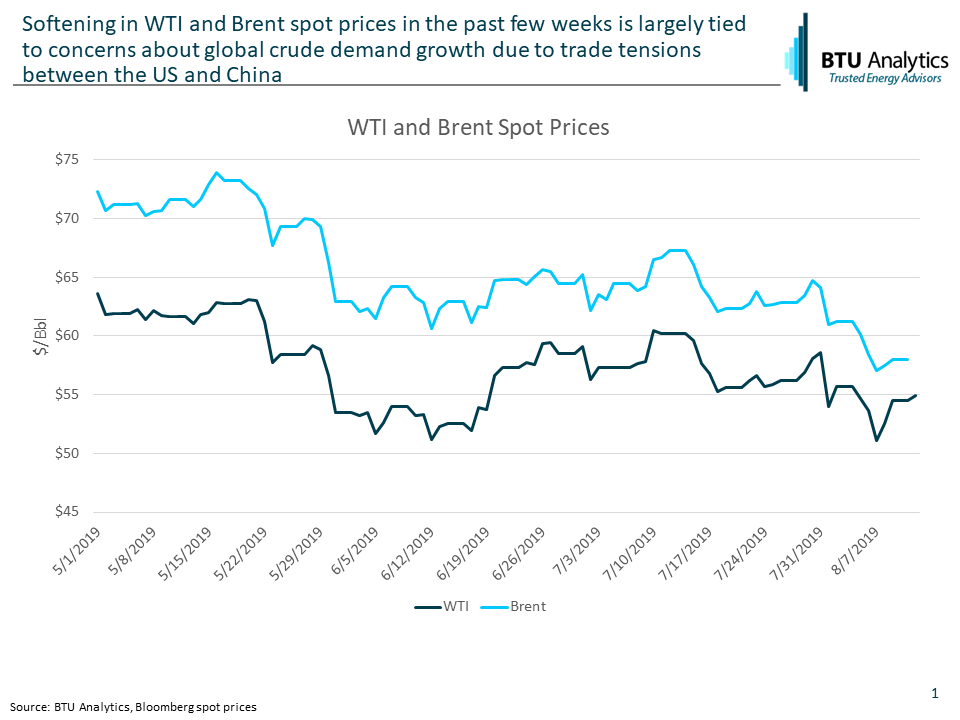

Both US and international crude oil prices have been on a downward slide in the past few months amid trade tensions between the United States and China. Both WTI and Brent spot prices have swung following updates to trade talks between the two nations. However, the general outcome of every bounce has been another leg down in spot pricing with Brent now below $60/bbl and WTI near $55/bbl. Underlying the concern on the outcome of the trade war between the US and China is the impact to crude oil demand growth globally and the ramifications to balancing the global crude market. In today’s Energy Market Commentary, we’ll explore the cascading impacts to slower demand on the outlook for global crude balances.

As US crude supply and exports rise, the pace of global oil demand growth becomes an increased focus of the market. Going into 2019, global demand was expected to grow by 1.4 MMb/d and recent downward revisions to growth expectations are contributing to the slide in crude oil prices domestically and internationally. While growth expectations have declined, demand for crude is still expected to grow in 2019 and 2020. However, global economic growth slowing as a result of heightened trade tensions could force oil demand growth lower than forecasted, which could materially impact the global crude balance.

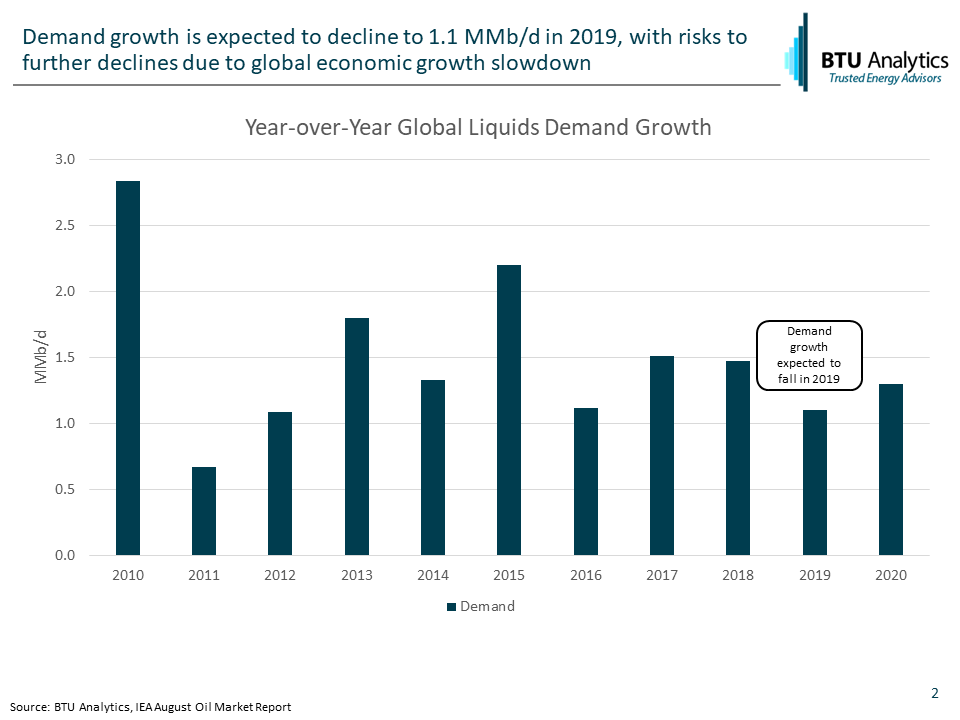

According to the International Energy Agency, China was the only major source of demand growth in the first half of 2019 at 0.5 MMb/d in incremental demand out of global incremental demand of 0.6 MMb/d. Further disruption to the US/China trade relationship could pose downside risk to global crude demand growth. Due to market uncertainty, the IEA recently revised down their forecast for global demand growth in 2019 and 2020 by 0.1 MMb/d (growth is now forecasted at 1.1 MMb/d and 1.3 MMb/d, respectively) but expects risks to be skewed to the downside for global demand.

The chart below shows year-over-year historical changes in demand growth. Historically, in years when demand growth has risen year-over-year, demand growth has increased by an average of 0.5 MMb/d. With this average in mind, a 0.1 – 0.2 MMb/d decrease in growth may not seem like a large change, but demand growth is already expected to be 0.3 MMb/d lower in 2019 than in 2018. Even small changes in global demand growth can have far reaching impacts on the global crude balance. What might happen if global demand growth falls further as a result of risks to economic growth in the coming years?

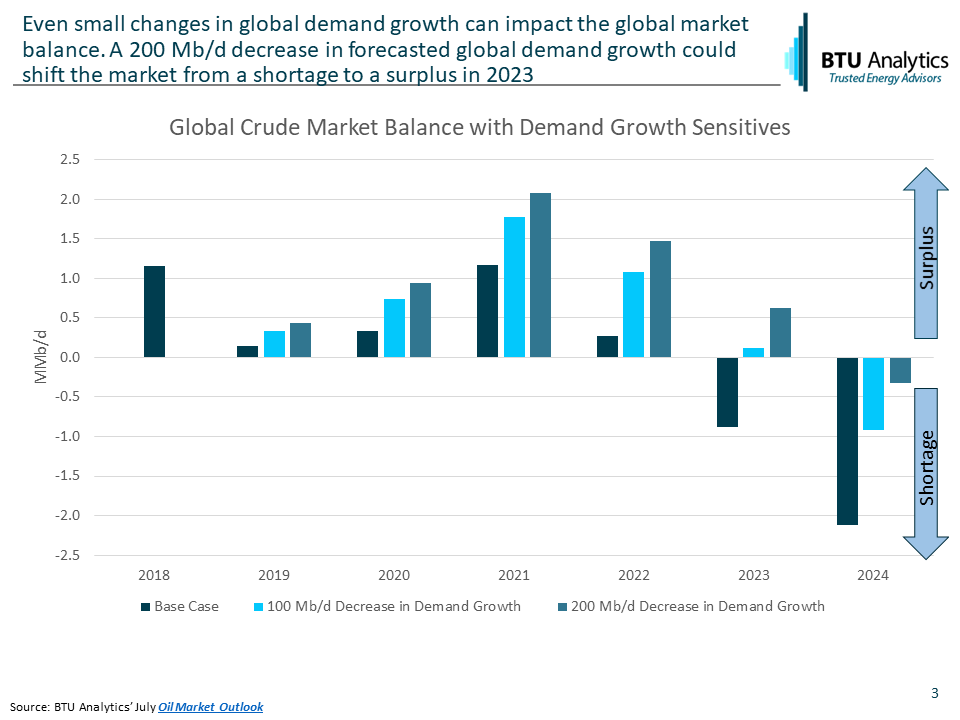

As of our July Oil Market Outlook, BTU Analytics modeled global demand to grow by about 1.2 MMb/d from 2019 to 2020, in line with IEA expectation in July, creating a 140 Mb/d surplus in 2019, assuming OPEC cuts are extended through 2019. The global balances then become extremely long supply in 2021 if OPEC cuts unwind. Assuming demand continues to grow at 1.2 MMb/d, the market would turn balanced in 2022 and net short in 2023 (base case below). However, slower growth has a cascading effect on the timeline to balance markets (assuming no change in production outlook from base case). The chart below highlights the impacts of even the relatively small revision of 0.1 MMb/d and the impact if expectations are lowered even further to 0.2 MMb/d decrease in global demand growth. As a result of slower demand growth, the crude market balance would reverse from a shortage to a surplus in 2023.

The equilibrium of the global crude market is sensitive to even small changes in demand growth, and the delicate balance of international trade could swing the global market in the coming months. In the US market, three crude pipelines are expected to come into at least partial service through the end of 2019, debottlenecking the engine of US supply growth, the Permian. While export capacity may be limited in the short term, (see Crude Oil Export Capacity – A Limit to Crude Production Growth?) the long term constraint on US supply growth will be the global oil markets’ ability to absorb the new supply. To follow BTU’s views on both international and domestic crude market dynamics, request a sample of our Oil Market Outlook.