On February 5th, the European Union (EU) imposed additional sanctions that target Russian refined product imports. Since the policy banned Russian product imports into the EU, the region will now have to find other sources of refined product supplies. The product ban will likely reconfigure trade routes, as seen with the EU ban on Russian crude imports, with Russian refined products heading toward Asia and South America and the EU sourcing more from the U.S. and Middle East. However, currently low storage of refined products in the U.S. could pose problems for this global rebalancing.

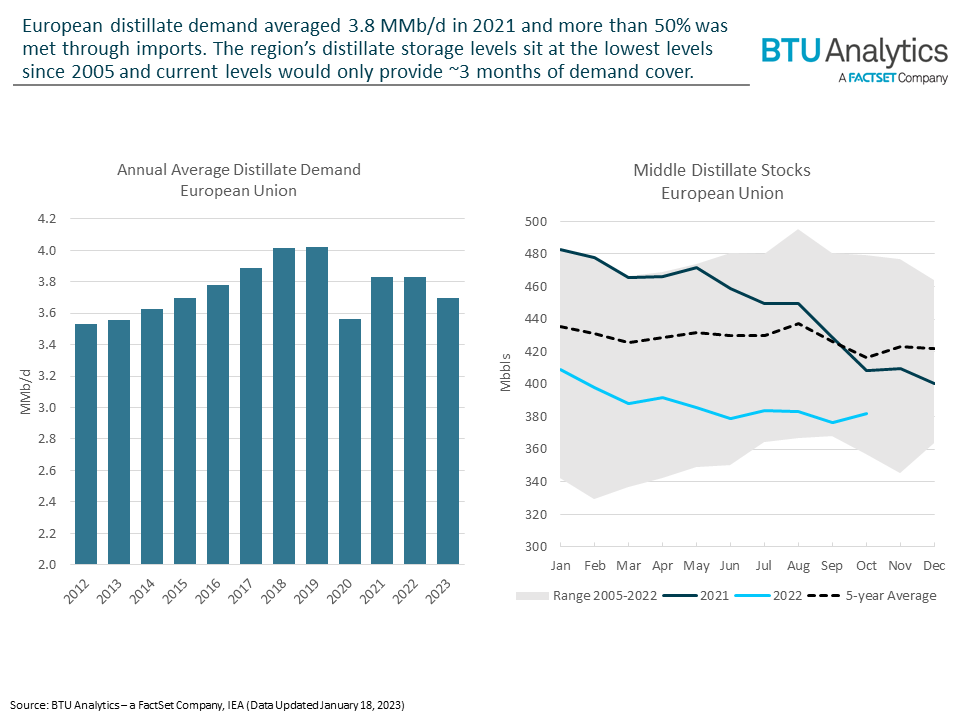

EU distillate demand peaked at 4.0 MMb/d in 2019 and fell to 3.8 MMb/d in 2022. The IEA expects demand to continue declining in 2023, reaching 3.7 MMb/d in 2023. Additionally, IEA data estimates the region imported ~2.0 MMb/d of distillates in 2021, suggesting the EU must import more than 50% of its distillate consumption. While a significant portion of EU demand is met through imports, summer consumer demand is supplemented by storage since daily demand typically outpaces imports and refinery output. Looking at EU distillate storage from 2005 to 2022, 2022 storage levels mark near the low end of the timeframe’s seasonal range, with October 2022 levels being 18.4 MMbbls below the five-year average. Based on October 2022 levels, the most recent data available, EU storage would only cover ~3 months of demand.

In 2022, U.S. distillate exports averaged 1.2 MMb/d, but exports to EU countries represented only 4% of that total. Historically, U.S. distillate exports to the EU represented as much as 28% of annual exports, but exports have shifted away from the EU toward South and Central America over the last decade. With the realignment of trade routes, it is possible Russia takes South American market share from the U.S., leaving the U.S. to send more distillate to the EU. If this doesn’t occur, the U.S. could export an additional 135 Mb/d above the 2022 average before reaching the export maximum observed in 2017.

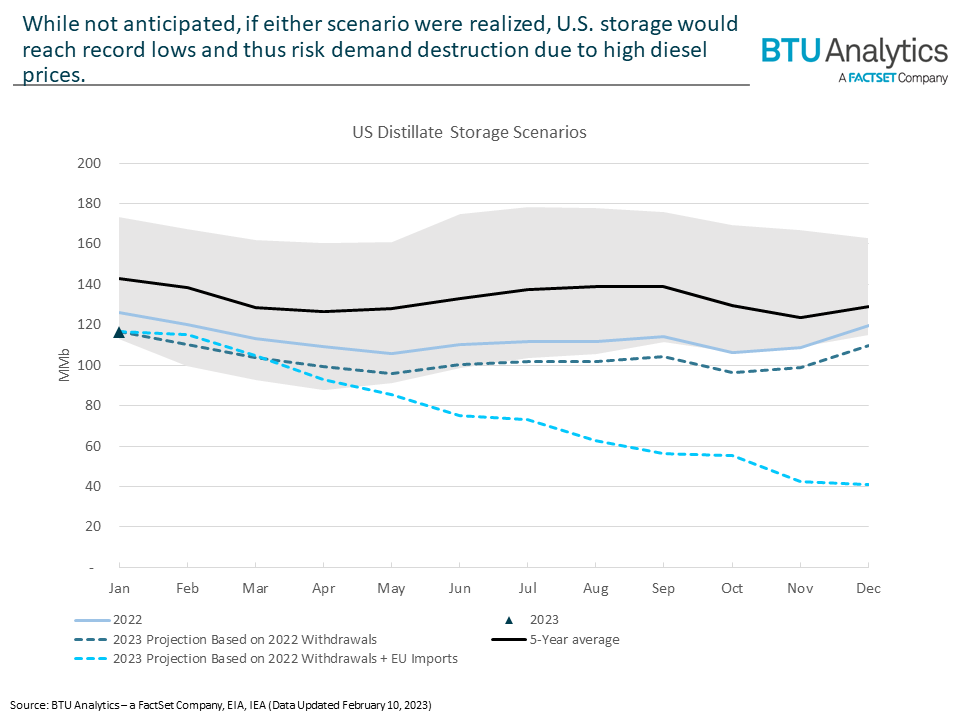

Similar to the EU, U.S. daily distillate demand in the summer is supplemented by distillate storage since daily demand outpaces refinery output. However, U.S. distillate storage levels are currently near record lows, and the January 2023 average distillate storage level of 116 MMbbls would only be able to cover ~2 months of distillate demand. With the shift in EU policy, BTU Analytics considers two possible scenarios:

- U.S. distillate withdrawals follow the same pace as 2022: If trade routes realign, U.S. exports stay flat, and 2023 U.S. distillate withdrawals follow the same path as 2022, storage levels would average 110 MMbbls in December 2023 and mark the lowest monthly level since 1989.

- U.S. increases distillate exports to meet EU demand: If the U.S. were to cover its own demand while also increasing exports to the 2017 maximum to meet EU demand, December 2023 diesel storage world reach ~41 MMbbls, thus reducing demand cover to less than a month.

While these scenarios represent a bookend for how low storage could be at year-end, BTU Analytics expects a low probability of either occurring since government or industry intervention would likely occur before storage reached such low levels.

With U.S. distillate storage already at record lows, any incremental distillate exports to support EU demand would quickly bring U.S. distillate storage to uncomfortable levels. Low levels of distillate, or even a shortage in the extreme case, would put upward pressure on diesel prices and increase fuel costs across economies, potentially hindering demand growth. BTU Analytics expects robust demand growth in 2023, putting upward pressure on benchmark prices, but any demand destruction from high diesel prices would limit demand growth and risk prices to the downside. To see what other risks BTU Analytics sees for WTI prices in 2023, see the latest Oil Market Outlook.