As the WTI strip hovers around the $50/Bbl it is natural to start to wonder which areas and which producers will be able to start layering on hedges to better fund drilling programs. Due to wide transportation differentials and stagnating average well results, the Bakken is one of the areas that has been hit hardest by weak pricing and has seen some the largest reductions in drilling activity. However, one reason that we do economic analysis at BTU Analytics on well by well basis is because it is easy to fall into the trap of looking at basin averages rather than a distribution of results. While basin averages are easier to quickly assess and analyze, they miss the fact that there may be a number of great wells in a basin that significantly outperforms the average well. To truly understand and characterize how different basins and producers will respond it is important to know who holds top tier acreage and who doesn’t.

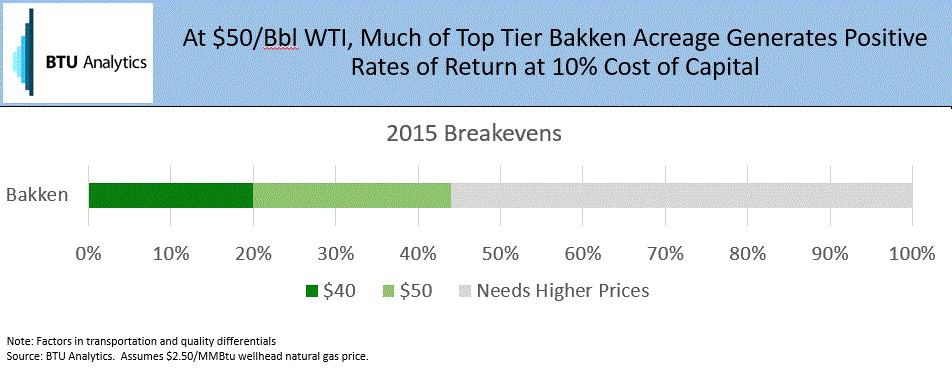

For example, while there are areas in the Bakken that work with today’s prices, an increase in WTI from $40/Bbl to $50/Bbl (factoring in a $10 discount for differentials) increases the number of Bakken wells completed in 2015 that generate a positive rate of return at a 10% cost of capital from 20% to 45%.

In order to understand the characteristics of these wells that are currently economic, let’s start by looking at the top 45% of wells drilled in 2015 (as measured by highest 30-day average oil IP rate) and compare them to the basin average. The average 2015 IP rates for Dunn and McKenzie counties were 539 B/d and 474 B/d, respectively. Looking at just the top performers, the average is almost 800 B/d and 720 B/d, which is between 50% and 70% higher than the average producers in the county.

Comparing a few select top performers to the basin average shows wide variability in type curves, but consistently strong IP rates and 12-month EURs. The names on the list come as no surprise, and recently, Whiting (NYSE: WLL) announced that they secured an outside investment in a wellbore only participation agreement, where their partner pays 65% of well cost for a 50% working interest (1Q 2016 Earnings Call).

Access to outside capital and well-level breakeven analysis has been a key theme that BTU Analytics has spent time researching and discussing to better understand which producers are best positioned to respond to pricing. Without looking at the distribution of wells, as the strip has moved to $50/Bbl WTI, it would be easy to miss the fact that top tier Bakken wells are able to generate positive rates of return, opening up a window for outside investment. Higher prices combined with access to outside capital could help producers maintain activity and potentially even begin to add some rigs back into the play.

{kind=link}

{kind=link}

{kind=link}

{kind=link}