As oil prices climbed to record highs following the Covid-19 Pandemic, production in the Uinta Basin rebounded in force, with production increasing 20% between January 2021 and May 2022. BTU previously noted the region’s historically muted activity; however, record-high horizontal rig counts, improved well performance, and basin consolidation suggests the Uinta is on an expansionary path. Unfortunately, the basin is approaching midstream infrastructure limits, and production may be constrained if the current pace of growth continues. In today’s Energy Market Insight, BTU discusses the implications of the Uinta’s recent ramp in production and how the basin’s midstream limitations could affect this increase going forward.

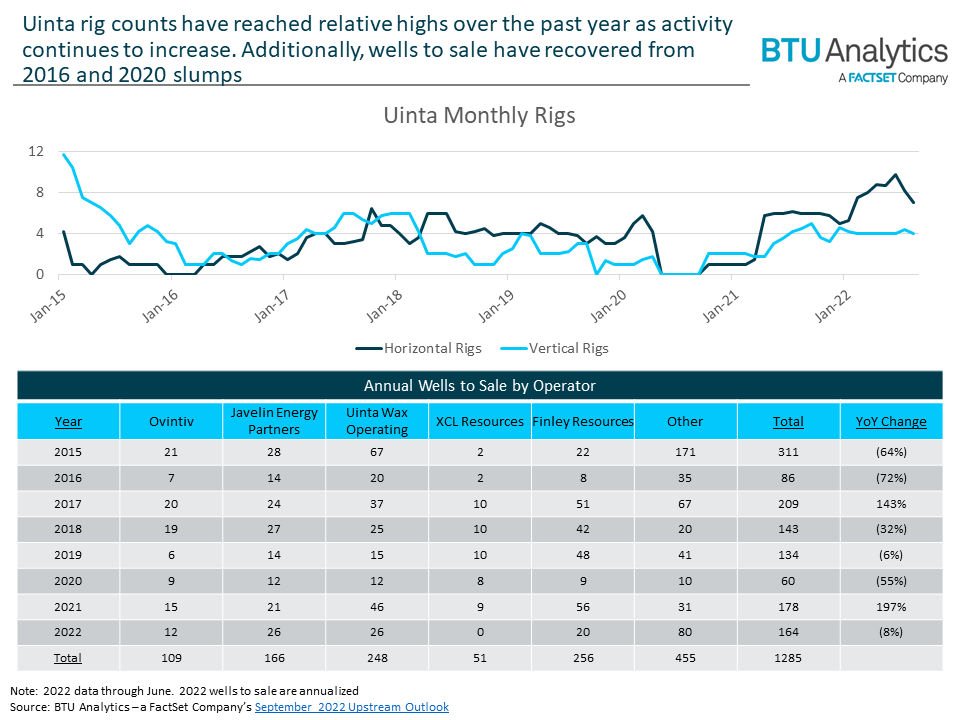

With total rigs in the region reaching levels not seen in several years, 2021 wells to sale increased year over year for the first time since 2017. Ovintiv, Javelin Energy, and Uinta Wax Operating represented 46% of the basin’s wells to sale in 2021 and lead current activity in the basin. Between 2018 and 2021, Ovintiv and Javelin reduced completions by ~20%, while Uinta Wax increased completions by 86%.

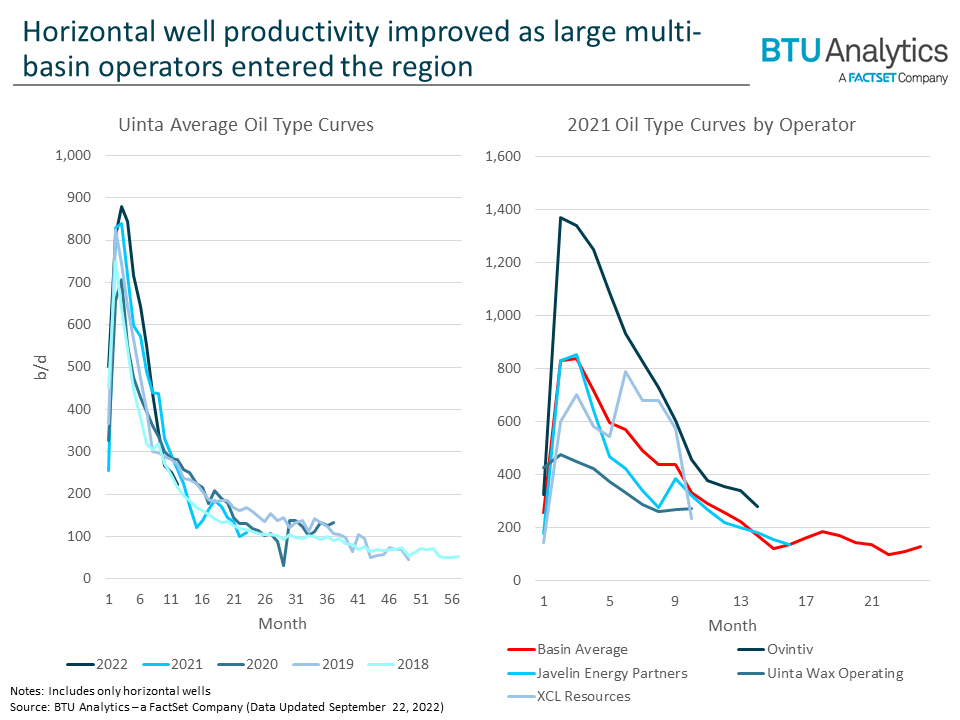

Peaking at levels eight times higher than that of vertical wells, Uinta horizontal well performance has improved over time and recently reached record levels. Ovintiv currently leads the pack with 2021 wells recording 30-day average IPs of nearly 1,400 b/d, or 75% higher than the basin average. Javelin Energy Partners’ and XCL Resources report well performance slightly below the basin average. If other producers continue to improve completion designs and increase lateral lengths, there is potential for basin well performance to improve.

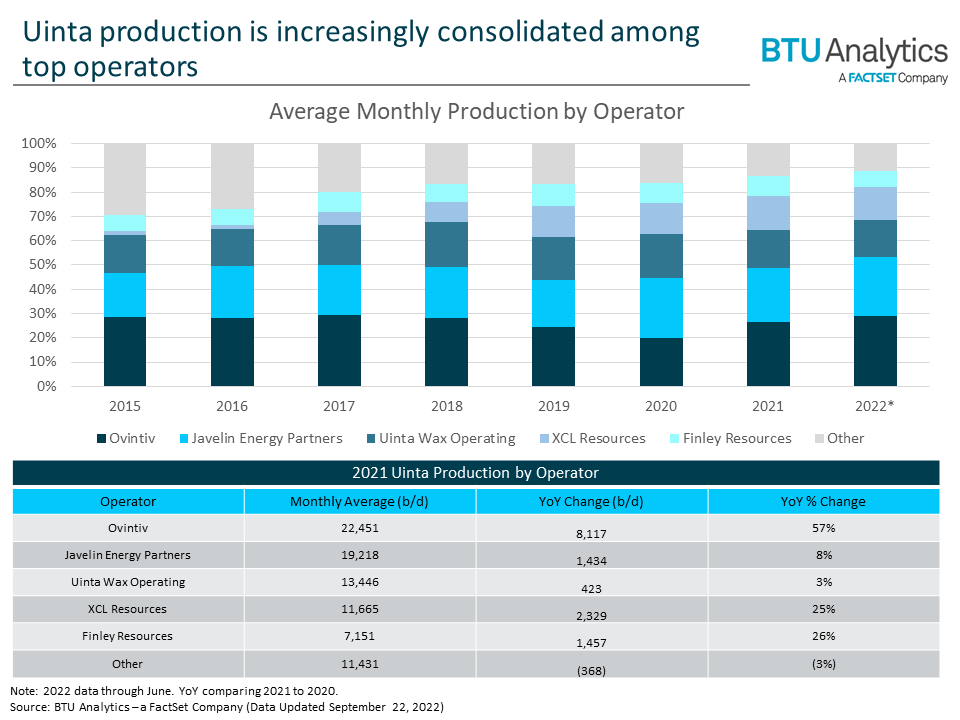

Prior to Ovintiv’s 2019 acquisition of Newfield Exploration, Newfield’s share of basin production fell from 29% in 2017 to 24% in 2019. Since the acquisition, Ovintiv regained their position to represent 29% of production as of May 2022. In regaining the market share, Ovintiv grew 8 Mb/d in 2022 on 15 wells to sale compared to Newfield growing 4 Mb/d on 21 wells to sale in 2015, thus showing the significance of Ovintiv’s well performance to their overall production. Javelin Energy Partners and XCL Resources, recent acquisitions of Crescent Energy and EP Energy, respectively, suggest the basin might not be done improving. Crescent Energy is a multi-basin operator with similar basin experience to Ovintiv and provides opportunity for Javelin to apply new expertise to their operations. The recent M&A activity may allow operators to access a larger knowledge base and drill more productive wells moving forward.

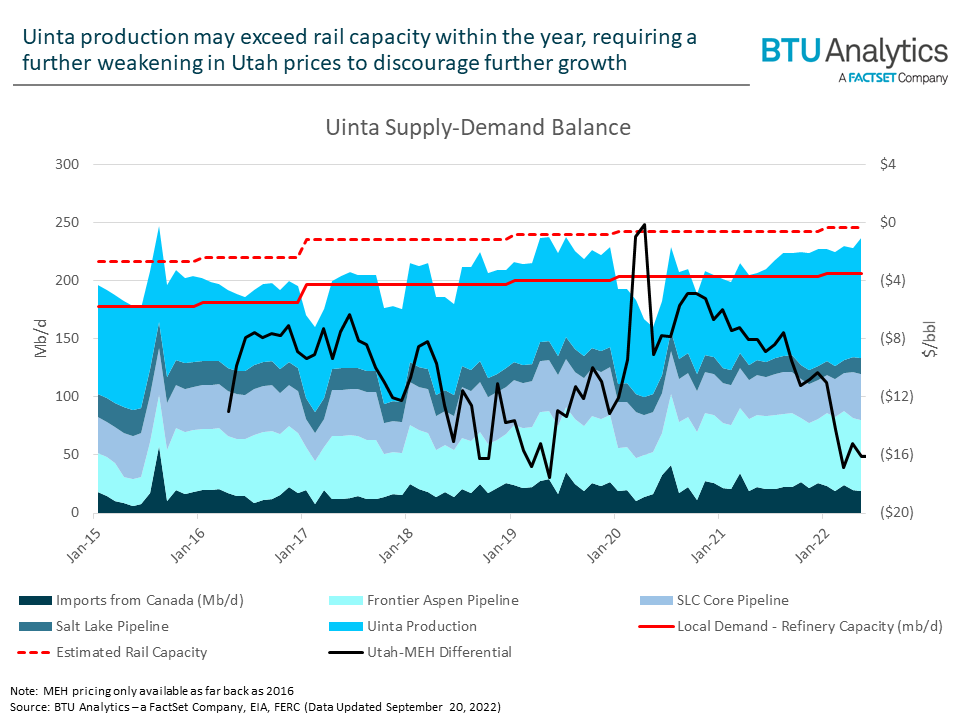

Uinta production increased 21 Mb/d during the first five months of 2022 and is quickly approaching its transportation limits. The unique characteristics of Uinta crude limit transportation to rail and trucking, as heated pipes are not currently used, thereby contributing to a wider differential compared to traditional crude basins. Uinta production primarily feeds Salt Lake City refinery demand as a component of their blended inflows. Combining with Canadian imports and other domestic pipelines, any production in excess of the 207 Mb/d plant capacity must be exported, typically by rail, to Gulf Coast refineries. As rail capacity is currently limited to around 39 Mb/d, the recent production ramp is steadily approaching maximum rail utilization and would force any incremental supply to be trucked or new rail facilities to be built.

While a rail line directly out of the basin has been approved, would alleviate a portion of transit costs, and could spur investment in new transloading terminals, the plan has been under litigation by environmental groups since February of this year. If approved, this project wouldn’t provide relief until 2024. With other sections of long-distance rail transport also under legal contention, additional midstream infrastructure for the Uinta remains somewhat uncertain. Therefore, BTU expects any production above rail capacity to be sold at heavy discounts, potentially discouraging further growth. For monthly analysis and regional forecasts on the Uinta and other plays, check out BTU’s Upstream Outlook.