On January 25th, 2022, Continental Resources announced that it will purchase Chesapeake Energy’s (NASDAQ: CHK) Powder River Basin Assets in Wyoming. This represents Continental Resources’ (NYSE: CLR) second investment into the basin to date, having purchased Samson Resources II LLC’s Powder River assets in February 2021. Today’s Energy Market Insight will examine production trends in the Powder River Basin, the evolution of horizontal well economics in the basin, and the economics of wells acquired by CLR from CHK.

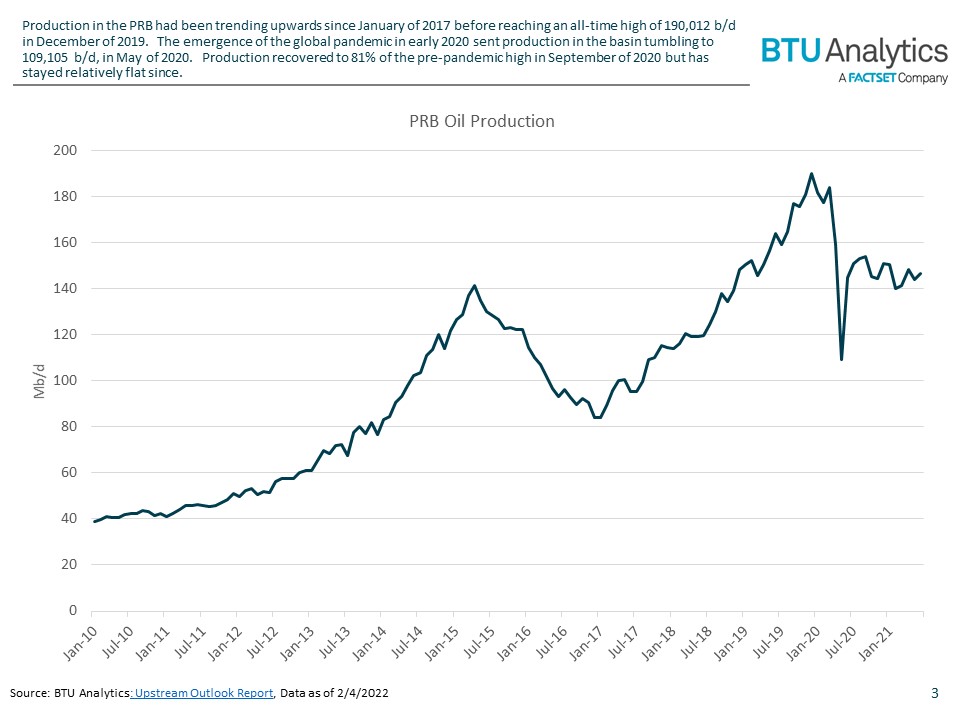

Production in the PRB had been trending upwards since January of 2017 before reaching an all-time high of 190 Mb/d in December of 2019. The emergence of the global pandemic sent production in the basin tumbling to 109 Mb/d, in May of 2020 as operators shut-in production in response to collapsing prices. After producers ended shut-ins, production recovered to 81% of the pre-pandemic high in September of 2020, but has stayed relatively flat since.

Now, with Continental doubling down on its initial investment into the Powder River Basin, is it possible for production in the Powder River Basin to begin growing again? Do the economics of wells in the region support additional investment?

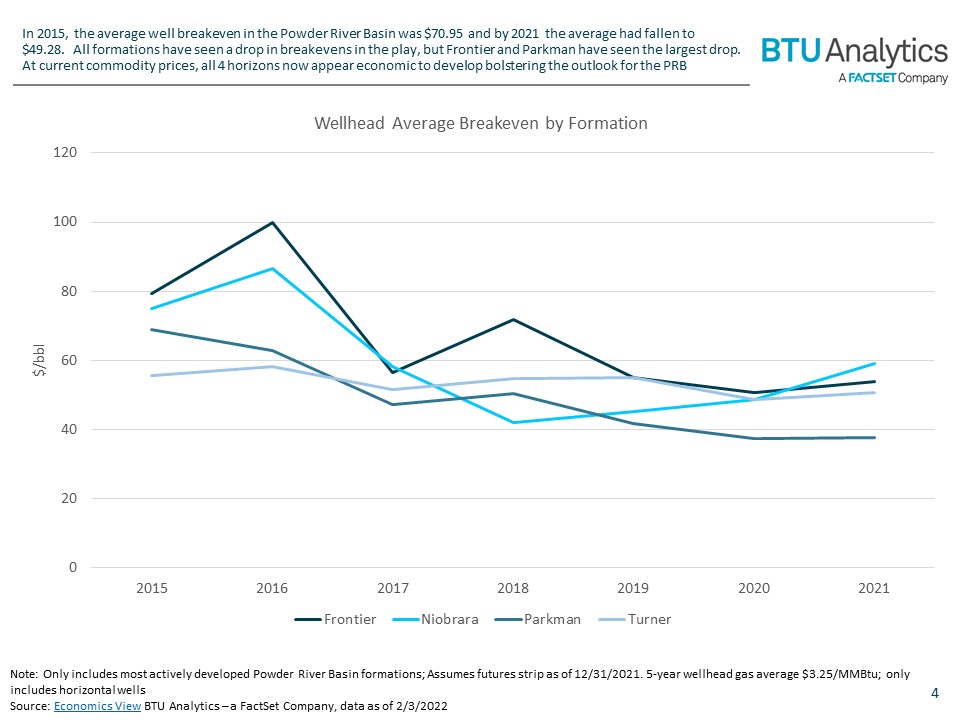

In 2015, the average well breakeven in the Powder River Basin was $70.95/bbl compared to average WTI price of $48.66/bbl for 2015. In 2021, the average well breakeven in the PRB had fallen to $49.28/bbl and WTI prices in 2021 averaged $68.13/bbl. Over the last decade, the PRB has garnered interest for its multi-horizon development. However, historically, this has not borne much fruit as variability across geography and geology drove overall breakeven estimates higher except for distinct pockets of success. The chart below shows the improvement in well economics for four of the most drilled formations in the Powder River Basin. Wells drilled targeting these formations constitute 82% of all wells drilled from 2015 to 2021 in the basin.

The graph above shows these top four formations and their change in average breakeven from 2015 to 2021. The Turner formation, which in 2015 had the best average breakeven amongst the top four formations, has seen the smallest reduction in average breakeven relative to 2015. Despite the relatively small reduction, the Turner formation had the second lowest average Relative to 2015, the Parkman formation has seen the largest reduction in average breakeven amongst the top four formations, declining 46%. Even though the Parkman formation has had the lowest average breakeven amongst the top four formations since 2019, the Turner and Niobrara formations were both targeted more often in 2019, 2020, and 2021.

The Heath, Mowry, Muddy, Shannon, Sussex and Teapot formations are some the other producing formations in the Powder River basin that have historically not been the subject of a great deal of activity. One thing to note, is that in 2020 and 2021, the percentage of wells being drilled targeting these formations has grown. A new record high percentage of wells drilled targeting these formations was set in 2021 potentially improving the outlook for multi-horizon development in the basin should the productivity and well economics in these formations pan-out.

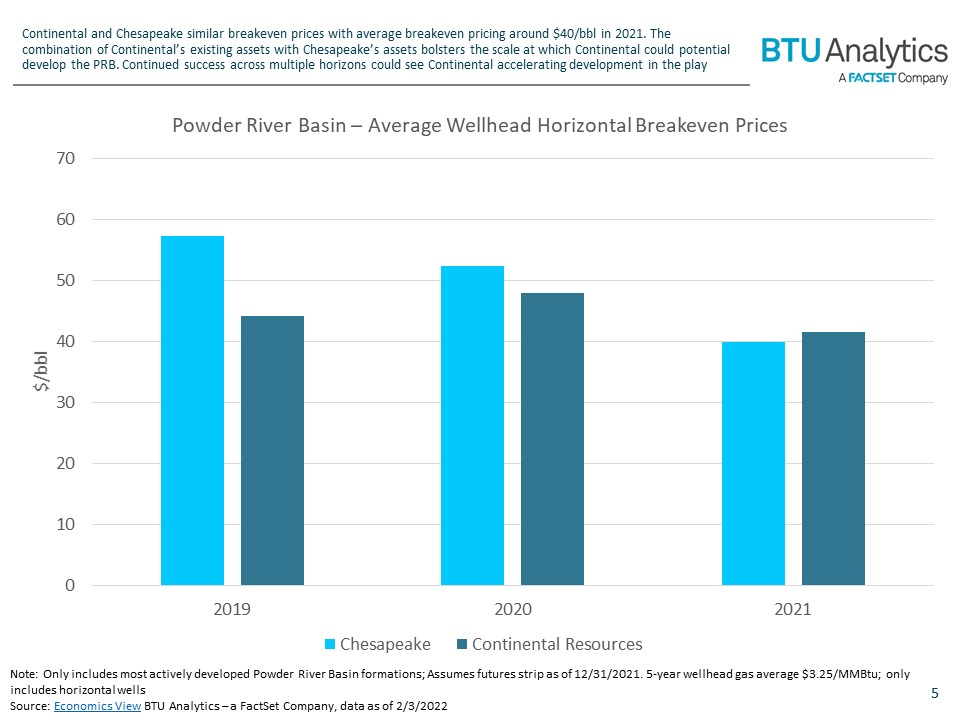

With breakevens improving across the board in the Powder River Basin, let’s compare the acreage Continental acquired from Samson Resources against Chesapeake’s assets. The wells Continental acquired from Samson Resources that started producing in 2019 and 2020 had marginally lower breakeven prices than the wells Chesapeake turned-in-line during the same timeframe. In 2021, both Continental’s and Chesapeake’s wells have performed similarly, with average breakeven prices around $40/bbl. It is worth noting that there are significantly fewer wells in Continental’s sample than Chesapeake’s. This is notable because despite having a much larger sample size of wells, Chesapeake’s wells have relatively similar economics. The larger sample size allows us to be more confident that Chesapeake’s economics could be more representative of average performance, whereas Continental’s wells may be less representative of what they are able to achieve moving forward.

The Powder River Basin will provide Continental a new option to grow production. With improving economics, a new operator for two large acreage positions, the improved potential for multi-horizon development, and oil prices near $90/bbl, the outlook for investment in the PRB is looking better than it has over the last 5-years. For more information on BTU Analytics’ outlook for Powder River Basin production request a sample of sour Upstream Outlook report.