As the impacts of COVID-19 on the global economy remain in flux, it’s important to understand where we are at today based on the current information. Already some of the largest airlines in the world, including United, Delta, and American, have lowered their expected flight capacities in 2020 around the globe. Given that travel, and subsequently, jet fuel demand, are likely to be some of the hardest hit areas by the COVID-19 pandemic, today’s Energy Market Commentary will focus on how much of global oil demand is made up by jet fuel and what these announcements could mean for the global jet fuel market.

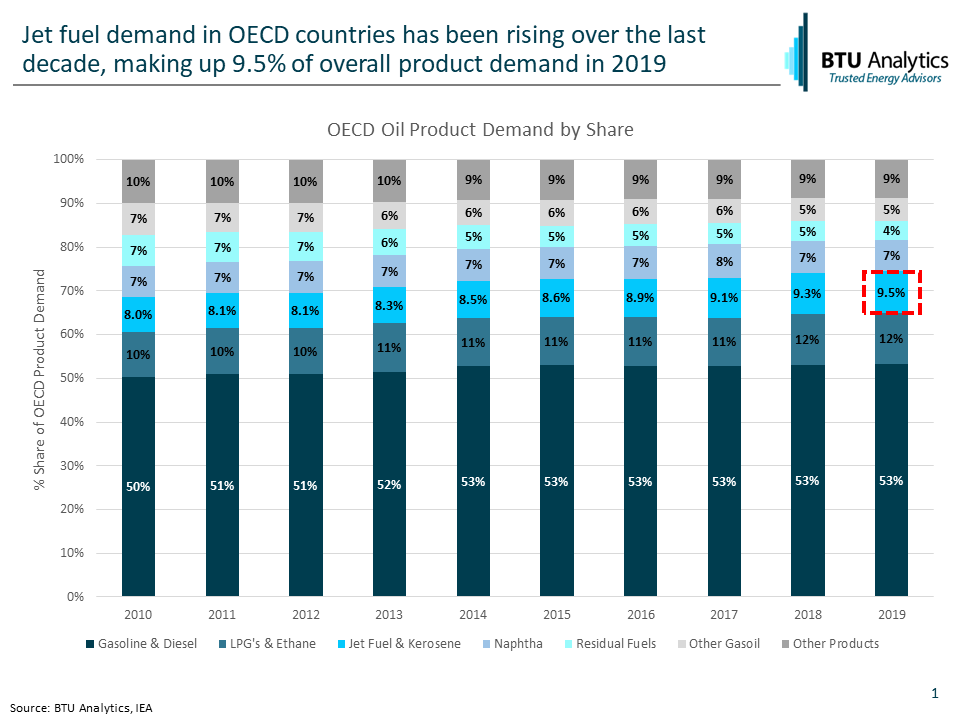

The chart below highlights annual product demand by category across all OECD countries. While jet fuel makes up a small portion of overall demand consumption, it has been rising over recent years. Jet fuel in 2019 accounted for 9.5% of overall product demand. If we extrapolate this relationship out and assume that non-OECD countries utilize air travel slightly less than their OECD counterparts, then non-OECD jet fuel demand could represent roughly 6% of overall refined products demand in those countries. With that, 2019 jet fuel demand would equate to approximately 7.97 MMb/d based on the EIA’s forecast of 100.75 MMb/d of global liquid fuels consumption in 2019.

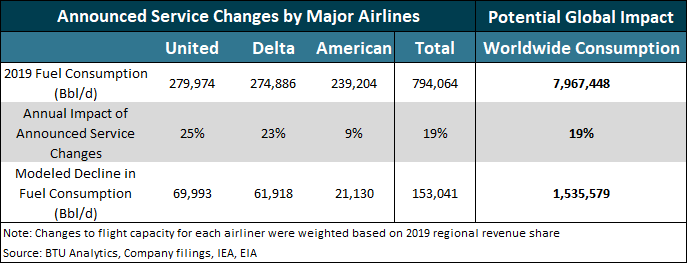

As was highlighted above, major US-based airlines have already announced service changes over the next several months that are set to significantly impact their consumption of jet fuel. United announced that it would cut May and April capacity by 50%., with similar cuts expected for the remainder of the summer months. Delta announced that its domestic flight capacity would likely be down 10% to 15%, trans-Atlantic down 15% to 20%, Pacific down 65%, and Latin American flights suspended. American announced its domestic capacity would be down 20% in April and 30% in May, while international flight capacity would decline by 75% from March to May. The table below summarizes these changes in annual term and estimates the potential annual impacts to jet fuel consumption based on 2019 consumption levels. Just from these three large airliners, the announcements would represent a decline in jet fuel demand of 153 Mb/d or roughly 19% of their 2019 consumption. In an extreme extrapolation where the remaining airliners globally follow suit with similar cuts to air travel, jet fuel could fall by almost 1.5 MMb/d from 2019 levels.

While this extrapolation is based on just a few known data points, the potential impact to global fuel demand from just a few months of impacted flight capacity is staggering. As COVID-19 is expected to continue to spread, especially across the US and Europe, additional travel restrictions may be put in place that could further impact global jet fuel demand. Not to mention, jet fuel is just one area of a much larger refined products sector expected to be impacted by the virus. BTU Analytics is currently offering all of our existing clients one-on-one webinars with our latest thoughts on the outlook for gas and oil markets in this rapidly evolving market. If you are not currently a client but would like to schedule a one-on-one presentation, please submit an inquiry HERE.