As crude prices stabilize, those with the balance sheets to optimize and expand acreage positions are doing so. Land swaps and purchases are occurring across the country from the Marcellus to the Permian to the DJ Basin with the intention to consolidate positions. Acreage consolidation and contiguous acreage positions are highly desirable to producers because they allow producers to optimize infrastructure utilization and drilling. Historically, we saw Anadarko and Noble conduct a land swap in the DJ Basin in 2013 stating that integrated development plans lead to “significant efficiency improvements including centralized facilities, streamline operation and reduced land work” (Noble 2013). The land exchanges and purchases today are no different. As producers jockey to best position themselves for a price recovery, Noble (NYSE: NBL) and PDC (NASDAQ: PDCE) recently announced a swap in the DJ, and QEP (NYSE: QEP) and Pioneer (NYSE: PXD) both recently purchased land to extend their Permian positions.

A specific efficiency improvement that producers are discussing in this round of acquisition is the ability to drill longer laterals. There is an overall correlation between IP rates and lateral lengths which producers are trying to optimize as they move forward with drilling programs. Looking at Martin county IP rates for various lateral lengths (both QEP and Pioneer expanded their positions here in the latest round of acquisitions) the majority of wells drilled have averaged between 6,000’ and 7,000’ laterals from 2013 to 2015. However, there is an increasing number of slightly longer laterals starting to be drilled, and they are showing promising results. As the chart below shows, laterals in the 7,000’ to 8,000’ range show a gain in IP rates compared to the shorter laterals. A small sample size and advancing technologies limits the conclusions that can be drawn for wells longer than 8,000’, which show lower average IP rates. As technology has improved, producers are increasingly talking about testing longer laterals to flex the boundaries of efficiency to be gained from longer laterals. At the Wells Fargo West Coast Conference held earlier this week, even EOG, who had previously been biased towards drilling shorter laterals, indicated that recent advancements which allow for increased control over well bore placement are changing the company’s disposition towards drilling longer laterals.

However, longer laterals come at a cost. Producers must balance higher IP rates and well productivity with increased upfront capital expenditures. This will be especially important in a rising price environment which will likely drive well cost inflation from current levels. Well cost savings since 2014 have been driven by leveraging a hybrid of new technologies and efficiencies as well as lower service costs. As producers look forward, the cost savings from a reduction in drilling days can be expected to be maintained, but cost savings that came at the expense of service company margins are likely to be lost as more rigs and completion crews return to the field.

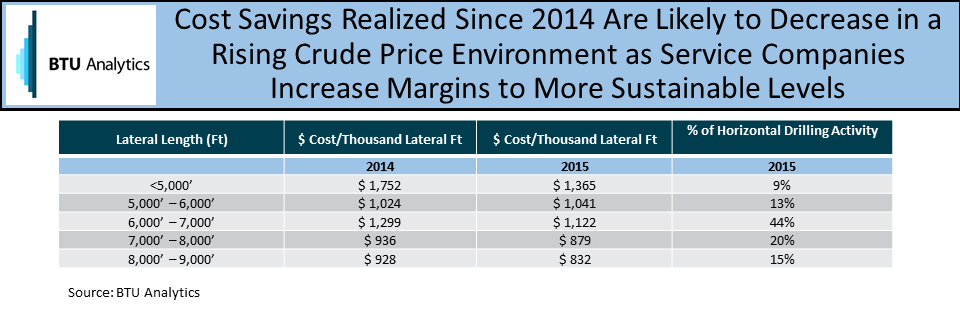

For example, in the Midland Basin where QEP recently expanded its position in Martin County, BTU Analytics estimates that well costs have fallen the most for short laterals (< 5,000 Ft) from an average cost of $1,752/Thousand Lateral Ft to $1,365/Thousand Lateral Ft between 2014 and 2015. However, 44% of 2015 wells were drilled on 6,000’ to 7,000’ laterals in the Midland Basin with costs falling an average of 14% between 2014 and 2015. Focusing on longer laterals, the cost savings have been less significant as longer lateral wells already experience some advantage of economies of scale despite a larger upfront capital investment.

As prices recover, some of these gains are likely to be erased as service costs are likely to increase as well. Producers indicated at a recent industry conference that they estimate they could lose between 30% and 40% of well cost savings in a rising crude price environment.

Therefore, early movers towards drilling longer laterals are well-positioned to capitalize on the likely disconnect between rising crude prices and service costs. Commodity prices are expected to rise first, providing these producers with more cash flow from wells with longer laterals and higher IP rates at a lower cost than in the future.