Last week, BTU Analytics’ Energy Market Insights touched on how the various outlooks for global liquids demand have vastly different implications for the recovery of the oil industry. While getting a complete picture on how oil demand recovers will take time, global supply is also in flux and will significantly impact any recovery in crude supply. Recently, conversations amongst Saudi Arabia and Russia to potentially extend the deepest cuts agreed upon in the April production deal for up to two more months, combined with reports of a lack of curtailment compliance in Iraq and Nigeria, has shed light on the uncertainty of global liquids supply going forward. This commentary will compare various scenarios on the path of OPEC+ production and how that could impact the path to recovery.

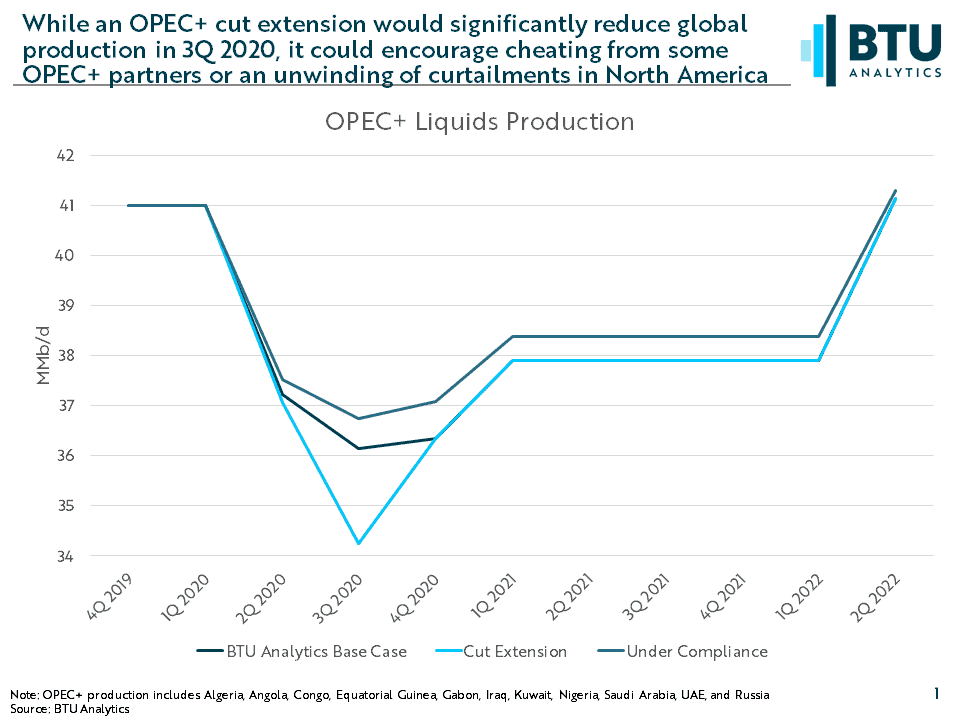

While no amendment to April’s historic OPEC+ production deal has been finalized, Saudi Arabia and Russia are discussing a potential extension of the deepest production cuts utilized in May and June for as much as two months. This would result in an extension of the 9.7 MMb/d of production cuts for July and August, instead of increasing production by 2 MMb/d (representing 7.7 MMb/d of cuts) for the remainder of 2020. However, at the same time, reports of a lack of compliance from Iraq and Nigeria, which have only cut 20% to 40% of pledged cut levels, could lead to a slow deterioration of the production deal. This could be exacerbated in the face of recently rising crude prices. The chart below details how production from select OPEC+ producers could evolve in the months to come based on an extension of current cuts or a slow deterioration in compliance. If cuts are extended, BTU Analytics assumes that current cuts (including voluntary, additional cuts from Saudi Arabia, UAE, and Kuwait) are extended through August before returning to BTU’s base case. In the ‘Under Compliance’ scenario, BTU Analytics assumes that low compliance from Iraq and Nigeria of 40% leads other countries like Russia, Algeria, and Angola to gradually increase production.

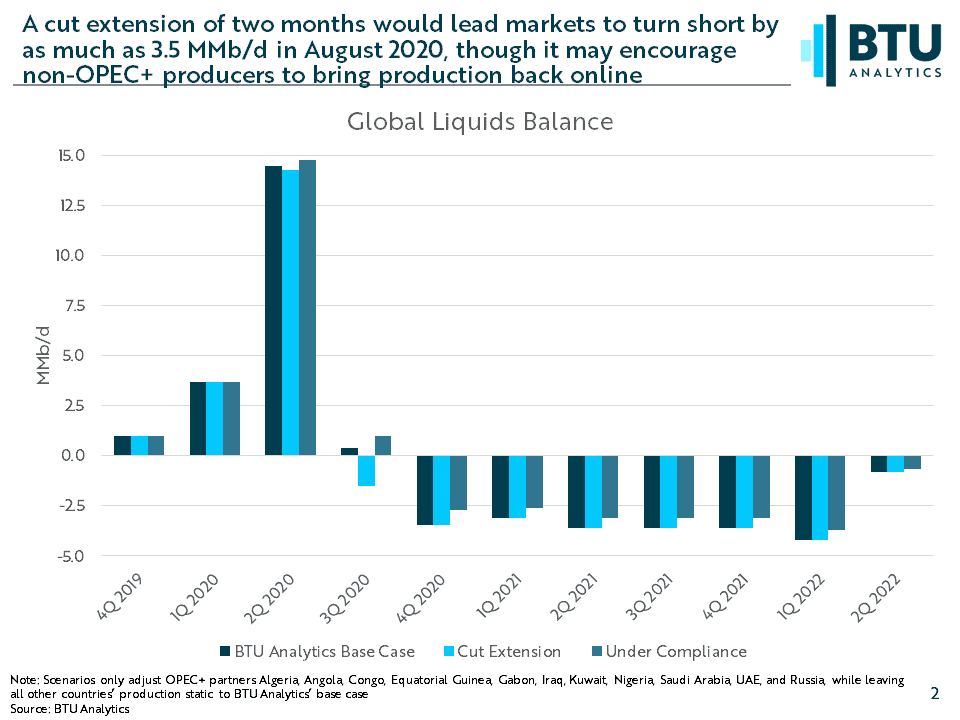

These two scenarios have implications for the balance of global liquids supply and demand, all else equal, shown in the chart below. If current production cut levels are extended in July and August, global liquids balances would turn short by as much as 3.5 MMb/d. This would help quicken the drawdown of global crude inventories, while BTU’s base case assumes markets remain slightly long on average in 3Q 2020. On the other hand, a lack of curtailment compliance spreading from Iraq and Nigeria to other OPEC+ nations could keep markets long by nearly 1 MMb/d in 3Q 2020. This could be further exacerbated if pricing continues to improve, encouraging US and Canadian producers to bring curtailed volumes back online, which some have already started to do.

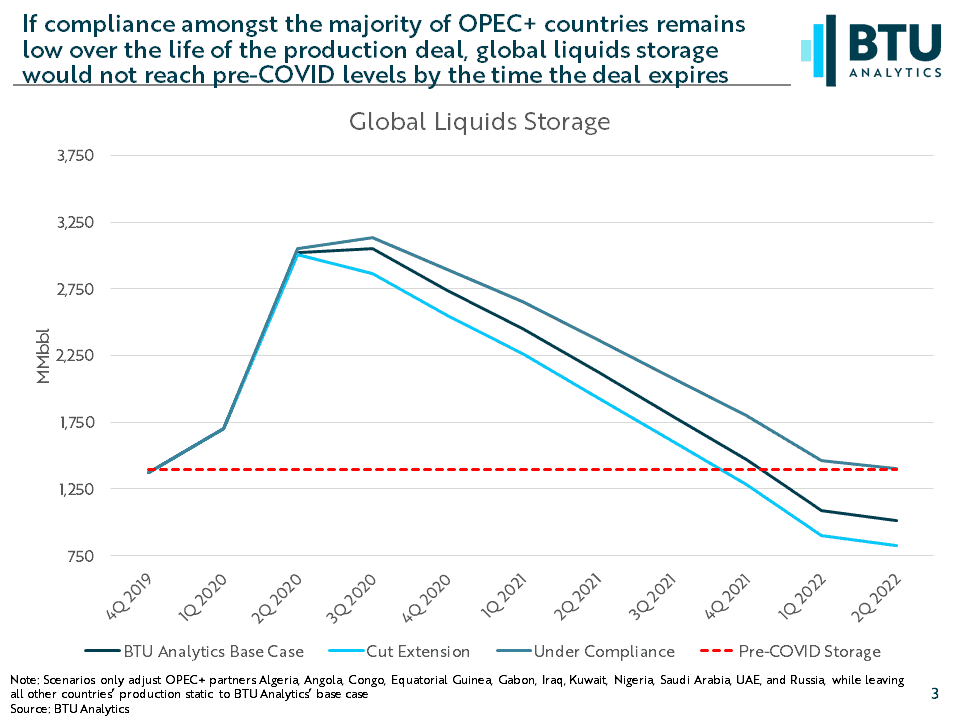

Depending on how these scenarios play out, global crude markets may not see storage fall to pre-COVID levels. In the chart below, after skyrocketing from the rapid impacts to demand from COVID-19, global liquids storage levels could decline at much different rates depending on each scenario outlined earlier in this commentary. In fact, if current cut levels are extended and compliance remains robust, global storage could fall to previous levels by 4Q 2021. In comparison, BTU’s base case assumes that it will take the entirety of the current production deal with high compliance to work storage levels down to prior levels, while the low compliance scenario will not result in storage declining to pre-COVID levels.

A full recovery from the impacts of COVID-19 is far from certain for liquids markets, even in the long term. Recovery will depend both on the gradual rebound in demand as the effects of the pandemic wear off, as well as a cautious response by producers to increase production in lockstep. This recovery could be derailed to the extent that producers fail to adhere to their pledged production cuts. To see how BTU Analytics forecasts the recovery in crude pricing, request a copy of the Oil Market Outlook today.