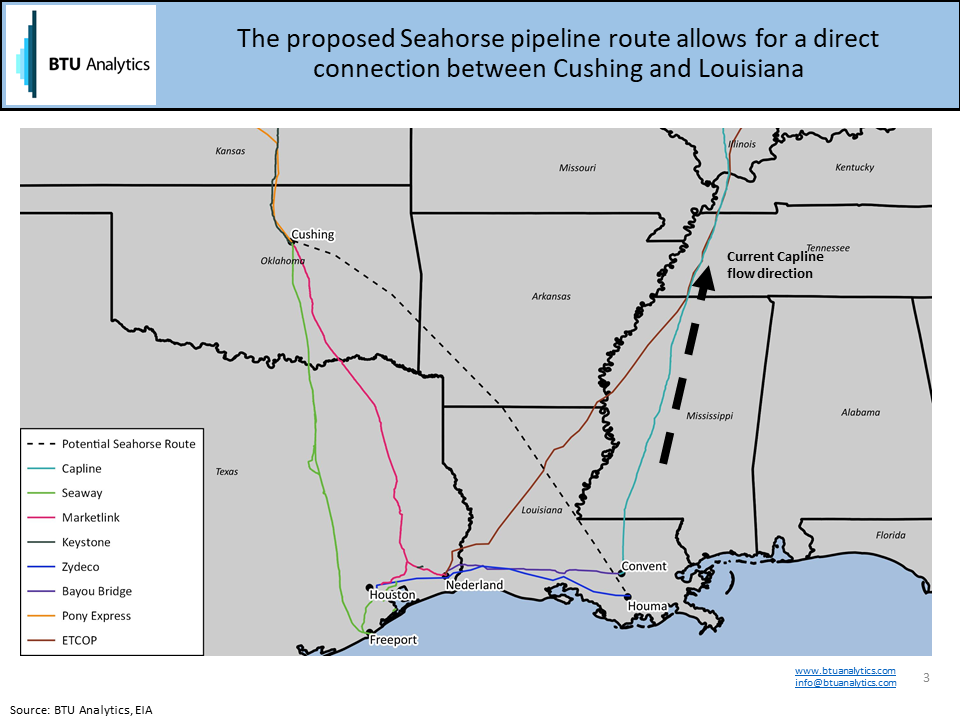

Tallgrass Energy announced an open season on August 15, 2018, to solicit shipper commitments to construct the Seahorse Pipeline, a new 800 Mb/d crude pipeline from Cushing to St. James. Cushing spreads to the Gulf Coast have been highly volatile since April as pipelines like Keystone, Marketlink, and Seaway have been operating at high utilizations to move increasing inbound Rockies and Canadian oil production to Gulf Coast refineries. A combination of growing production from the Powder River, DJ Basin, and SCOOP/STACK and increasing Canadian pipeline flow is likely to continue pressuring spreads between Cushing and the Gulf. This leads to several key questions. First, are WTI/Gulf spreads being driven by bottlenecks getting out of Cushing? Or is there a bottleneck further downstream to connect barrels flowing from Houston to Louisiana? And if so, will the bottleneck at Houston worsen as new Permian pipeline projects are completed and potentially flood Houston with Permian crude?

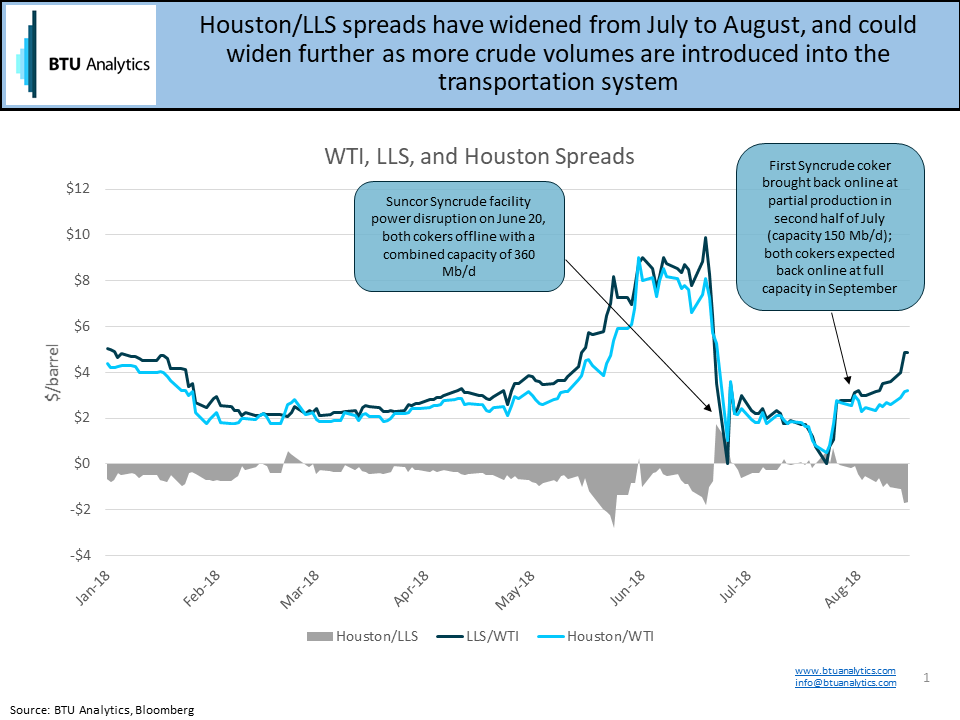

Since April, not only has the Cushing to Houston spread widened, so has the spread between Houston and LLS, this indicates that there could be a growing bottleneck not just between Cushing and Houston, but also between Houston and St. James. Spreads temporarily collapsed in late June and July because of reduced crude supply and inbound crude from Canada at Cushing due to the outage of Suncor’s 300 Mb/d upgrader. The partial restoration of service has already begun to pressure spreads between Cushing and Gulf Coast and full service is expected to begin in mid-September.

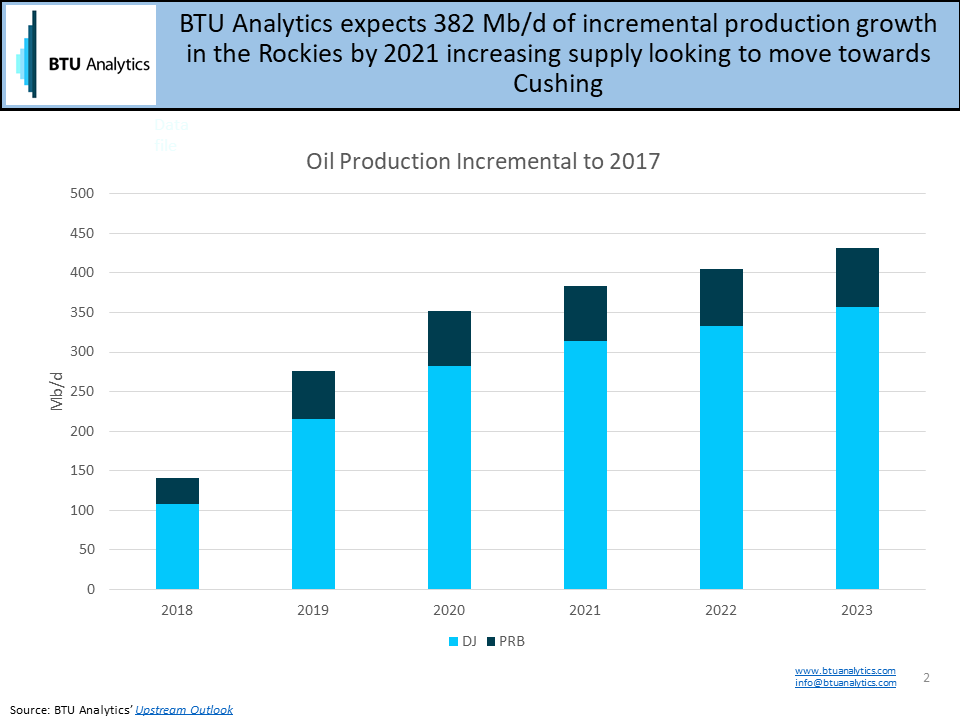

Production in the DJ and Powder River Basin is expected to increase by a combined 430 Mb/d by 2023 relative to 2017. Growth could be higher as several producers have announced plans to grow activity in the Powder River Basin based on promising results in 3Q 2018 earnings. (See our commentary from August 2nd and our Upstream Outlook published on August 15 with additional analysis). Most of this incremental production will flow to Cushing and on to Houston via Enterprise and Enbridge’s Seaway pipeline or TransCanada’s Marketlink. Given that these pipelines are already flowing at high utilization rates, if volumes on this route increase, bottlenecks could worsen.

There are a few infrastructure expansion projects in the works that could provide short-term relief to Gulf Coast and Cushing bottlenecks as Rockies production increases. Drag reducing agents will be used on Seaway starting by September 2018 to increase capacity by 100 Mb/d to 950 Mb/d, which may reduce the potential for Cushing bottlenecks near term. However, once volumes arrive in Houston, many continue to Louisiana on Zydeco (formerly Houston-to-Houma) and Bayou Bridge where spreads indicate a bottleneck is likely as well. Zydeco has been flowing at close to 90% utilization this year, contributing to the Houston bottleneck, and the completion of Bayou Bridge to fully connect to Louisiana continues to face opposition from environmental groups and regulatory delays. The completion of the Bayou Bridge extension from Lake Charles to St. James will add 280 – 480 Mb/d of increased connectivity between Houston and St. James and could help ease bottlenecks along the Gulf Coast. But if the Bakken, DJ, or Powder River Basin grows more than expected or Keystone XL is completed and increases inbound Canadian flows, a new pipe out of Cushing or Patoka would be needed to provide relief.

As a solution for the Rockies producers facing bottlenecks at Cushing and Houston, Seahorse could allow Powder River and DJ producers a direct pipeline route to the Gulf Coast. As a Tallgrass asset, Tallgrass could offer single joint tariff with Pony Express and Seahorse. This option allows for seamless supply-basin to demand market transportation, reduces or eliminates pump-over fees, and the need to stack rates across pipelines which could make this a very cost competitive rate compared to existing rates. This route also allows producers to avoid potential Houston bottlenecks and transport volumes directly to the LLS pricing area which trades, on average, at a premium to Houston.

The other potential project to help debottleneck Cushing is the Capline reversal project which would connect Patoka, IL, to St. James as well. Even though Capline does not connect to Cushing, it could divert volumes that would otherwise flow through Cushing and provide relief.

Both the potential Capline reversal and Seahorse have the advantage of moving volumes directly to Louisiana, avoiding Houston bottlenecks. Seahorse may appeal to producers as it allows a direct route for DJ Basin and Powder River Basin producers to the Gulf Coast. Given its wellhead to market capabilities and access to Louisiana markets, Seahorse could provide welcome relief for Rockies producers. For more on BTU Analytics’ view on oil prices and infrastructure development, request a sample of BTU Analytics’ Oil Market Outlook Report.