US shale development has redefined global energy supply. One of the most striking attributes of shale development is the production profile. Detractors love to point out that production from shale can decline by over 80% in just three years of first production. However, proponents point to investments that can return capital quickly. The decline of a single well is one thing, but when we have a cyclical business where activity rises and falls with prices, underlying shale base declines are a fundamental piece of information to consider when trying to predict inflection points in US production. Today’s commentary compares the underlying base decline profiles producers are fighting against in the major shale basins, and what levels of activity might be necessary to stave them off.

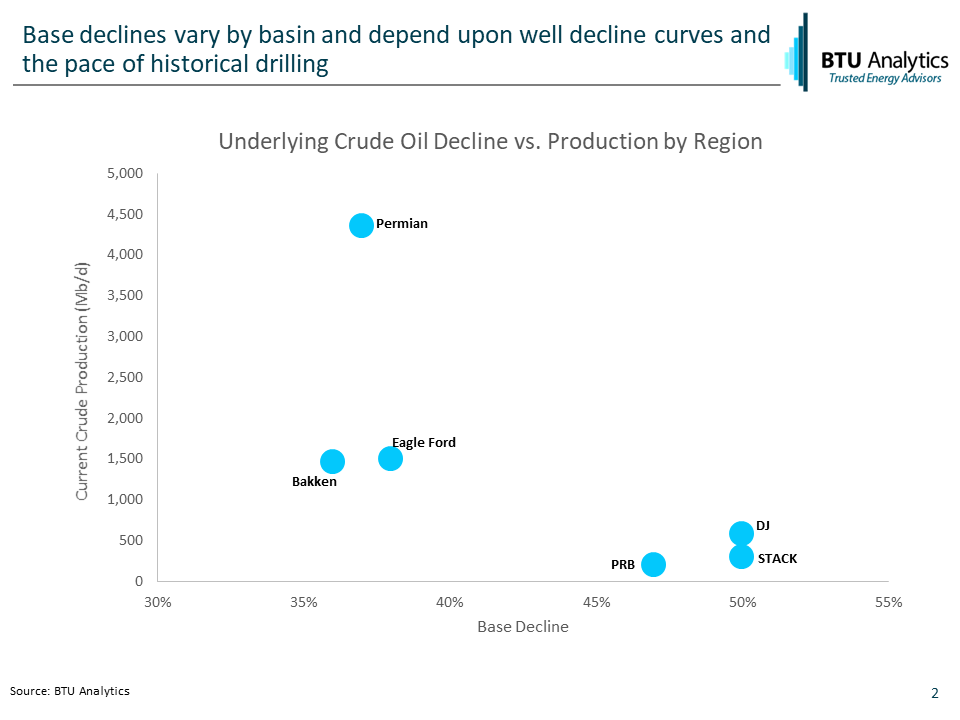

The Permian, Bakken, and Eagle Ford represent almost 60% of total US crude production today. The expected 12 month declines for underlying production in those plays are estimated to be 37%, 36%, and 38%, respectively, at this time. If all drilling and completion activity ceased in these plays, over the next twelve months production would decline by 2.7 MMb/d.

Looking at a few of the smaller plays shows that producers in these plays are swimming against a swift current. In the DJ, STACK, and Powder River areas, base declines are estimated to be 50%, 50%, and 47%, respectively. The chart below highlights base decline by region as compared to current crude oil production for the same areas.

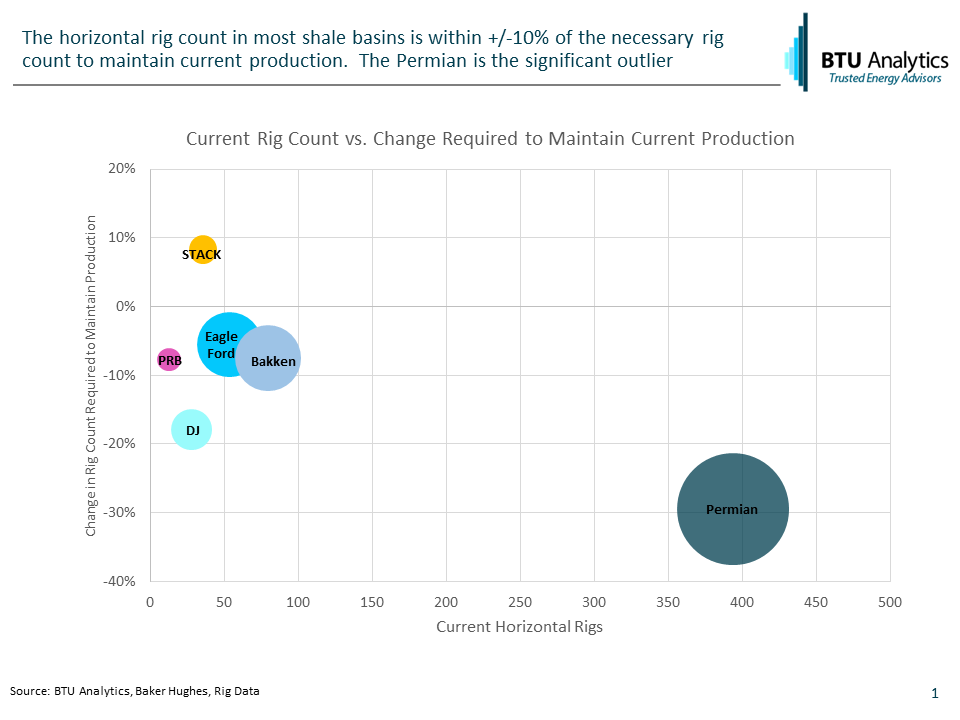

Will any of these base declines translate into actual declines based on the current rig count? Modeling the activity necessary to maintain current production in each of the plays through 2020 shows that only the STACK has a rig count that is below the rig count necessary to maintain production.

Despite higher relative base declines, the PRB and DJ are on a trajectory to grow based on the current rig count.

But will more rigs come out of the field? How long can producers hold out at current prices? What role does well productivity play in these projections? For these answers and more, request a sample of our Upstream Outlook service. This month’s Upstream Outlook features a spotlight feature on the impact of well spacing in the Permian and a drilldown on activity in East Texas.