As U.S. gasoline consumption approaches pre-pandemic levels, gasoline exports have risen in response to realigned supply routes following the Russian invasion of Ukraine. This rise in demand, in conjunction with U.S. refinery retirements, has tightened domestic gasoline balances. While most refined product markets have been impacted, motor gasoline storage specifically has steadily declined to seasonally low levels. This is due to both reduced operating capacity limiting supply and demand spikes abroad having increased exports. These dynamics have caused U.S. gasoline storage to fall to levels not seen since 2014.

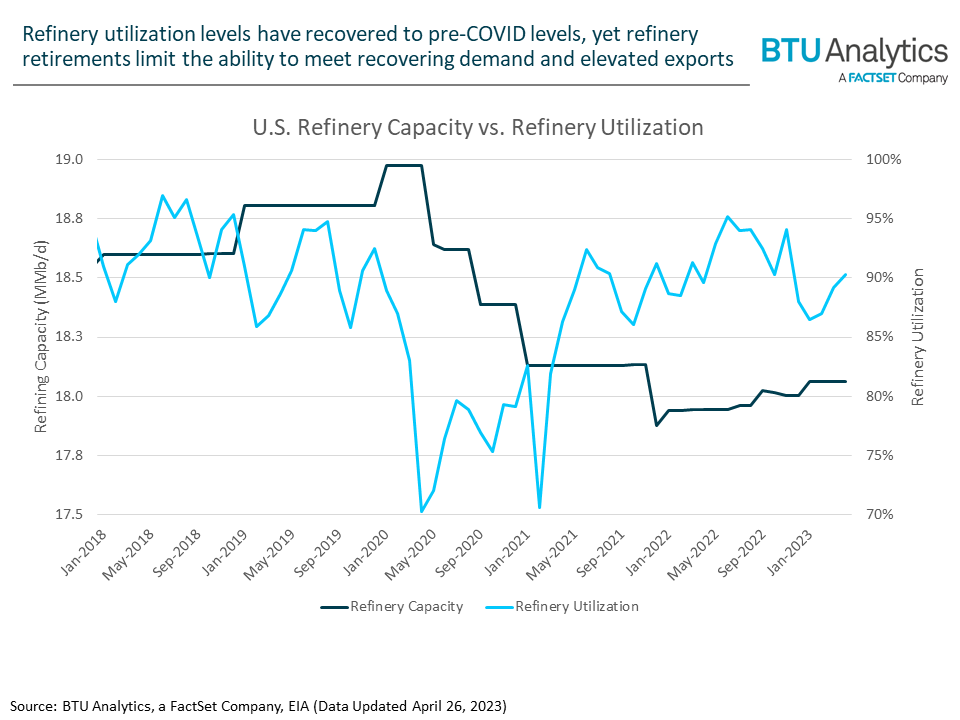

The U.S. refinery complex is tooled to run heavier quality crude than the quality produced domestically, and the high cost of retooling refineries is a barrier for shifting throughput towards lighter crudes. These high costs, combined with the pandemic, triggered many refineries to shut down operations entirely. And while refinery utilization levels have rebounded from pandemic-era lows, averaging nearly 94% last summer, refinery retirements between 2019 and 2023 have reduced total U.S. refining capacity by 1.0 MMb/d to 18 MMb/d.

The West’s sanctions on Russian product exports have altered global supply and demand dynamics. The undersupplied global gasoline market caused margins to improve and incentivized increased U.S. exports. Meanwhile, gasoline production has failed to keep pace with domestic consumption, which is currently 3% below the 2017–‘19 average. Light crude oil represented 88.2% of U.S. oil production by volume in 2022, but, as stated above, refineries are optimized for specific crude qualities and are slow to retool. For example, PADD 3 refiners’ crude throughput had an average API gravity of ~34 in 2022, compared to an average API gravity of less than 30 in 2010 before the shale revolution. Under current refinery designs, increasing light barrel throughput would reduce utilization levels and likely reduce refinery margins, thus making it unlikely refineries will be able to increase production to meet demand.

To assess the ability of U.S. gasoline storage to stave off further declines, BTU Analytics built two potential scenarios for 2023. Scenario A assumes supply (production and imports) and demand (consumption and exports) are held flat to 2022 month over month storage changes. This would put end-of-summer gasoline storage at decade lows this year. Scenario B assumes gasoline production increases with ExxonMobil’s Beaumont refinery expansion and consumption rises to pre-pandemic levels. Gasoline consumption currently sits ~3 percentage points below the 2017–‘19 seasonal average, but demand rising to historical levels would push gasoline storage to levels not seen since 2008. The low inventory levels would likely drive gasoline pricing higher and put downward pressure on elastic domestic demand.

Currently, U.S. oil product balances are well undersupplied, but gasoline is facing headwinds that may disrupt its already fragile market balance. The U.S. EPA recently issued an emergency waiver to allow greater blending of ethanol into gasoline to increase supply this summer. Russian sanctions have allowed for increased outputs to China and India at a discounted price, leading to an inherent increase of their refining output and export capabilities. This influx into the global market can depress refining margins and may cause U.S. refiners to readjust their export volumes. Further insight into how global supply and demand affects price dynamics and future production models can be found in the May 2023 edition of BTU Analytics’ Oil Market Outlook.