Drilling has made a robust return to the Uinta basin in 2021 with a strong WTI price stimulating oil-focused development. Current rig counts in the Uinta are the highest since early 2018. If this activity is sustained, it would quickly carry oil production to a new peak. Today’s Energy Market Insight examines the companies behind the recovery and the potential implications for regional supply, pricing, and refining markets.

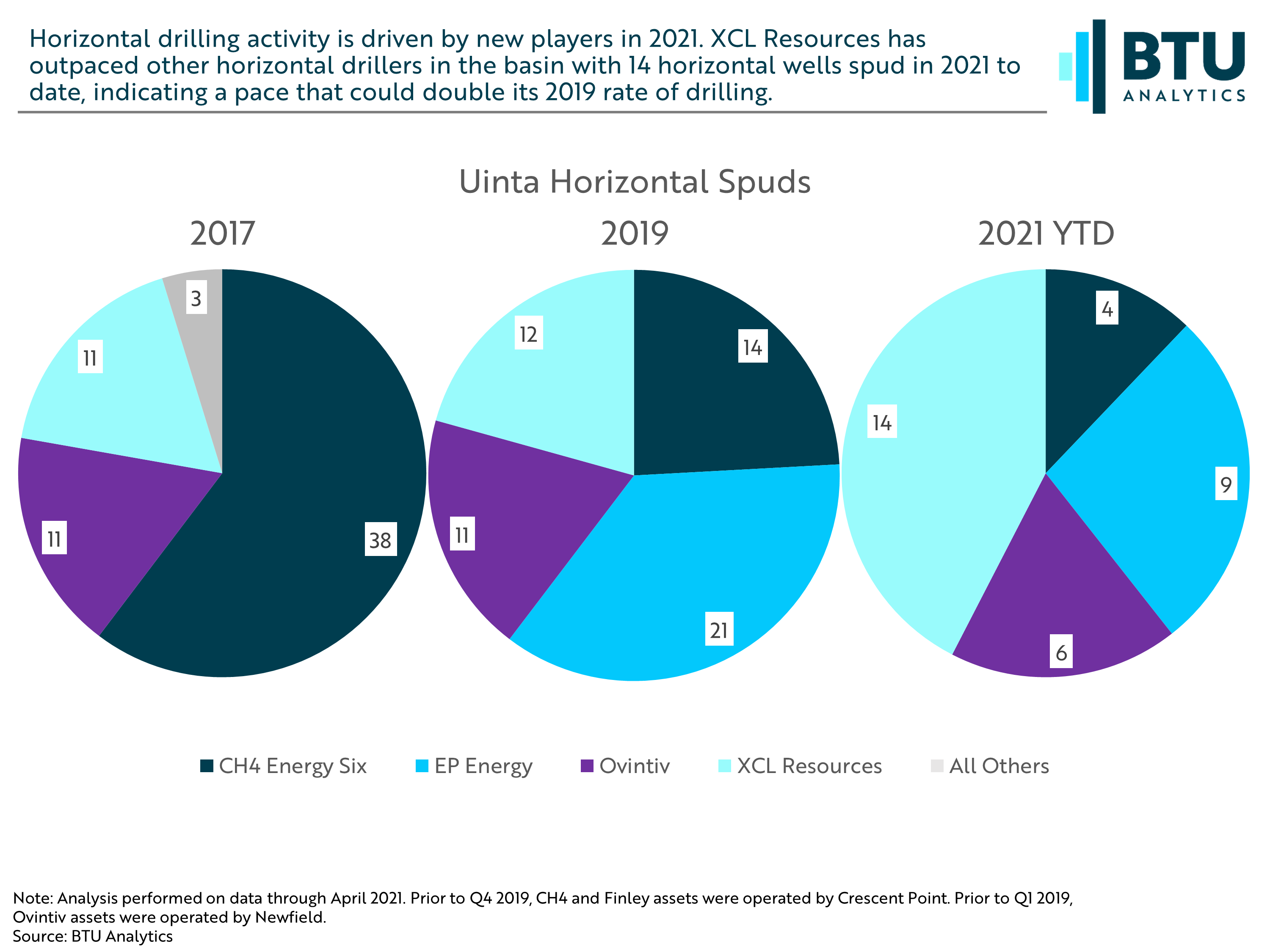

Drilling activity in the Uinta has historically been dependent on strong oil prices. In 2014, more than 20 rigs were operating in the basin drilling vertical wells, and operators were testing horizontal drilling with a peak of 7 rigs before oil crashed. Activity began to rebound in 2017 as oil prices recovered, but vertical activity stalled at 5 rigs. Meanwhile, horizontal activity climbed to 5 rigs and maintained that level up until the oil crash in March 2020 when activity across the basin went to zero. However, since October, drilling has been on the rise in the region. The chart below highlights the horizontal drilling since 2017 for key operators in the basin from BTU Analytics Production View Platform.

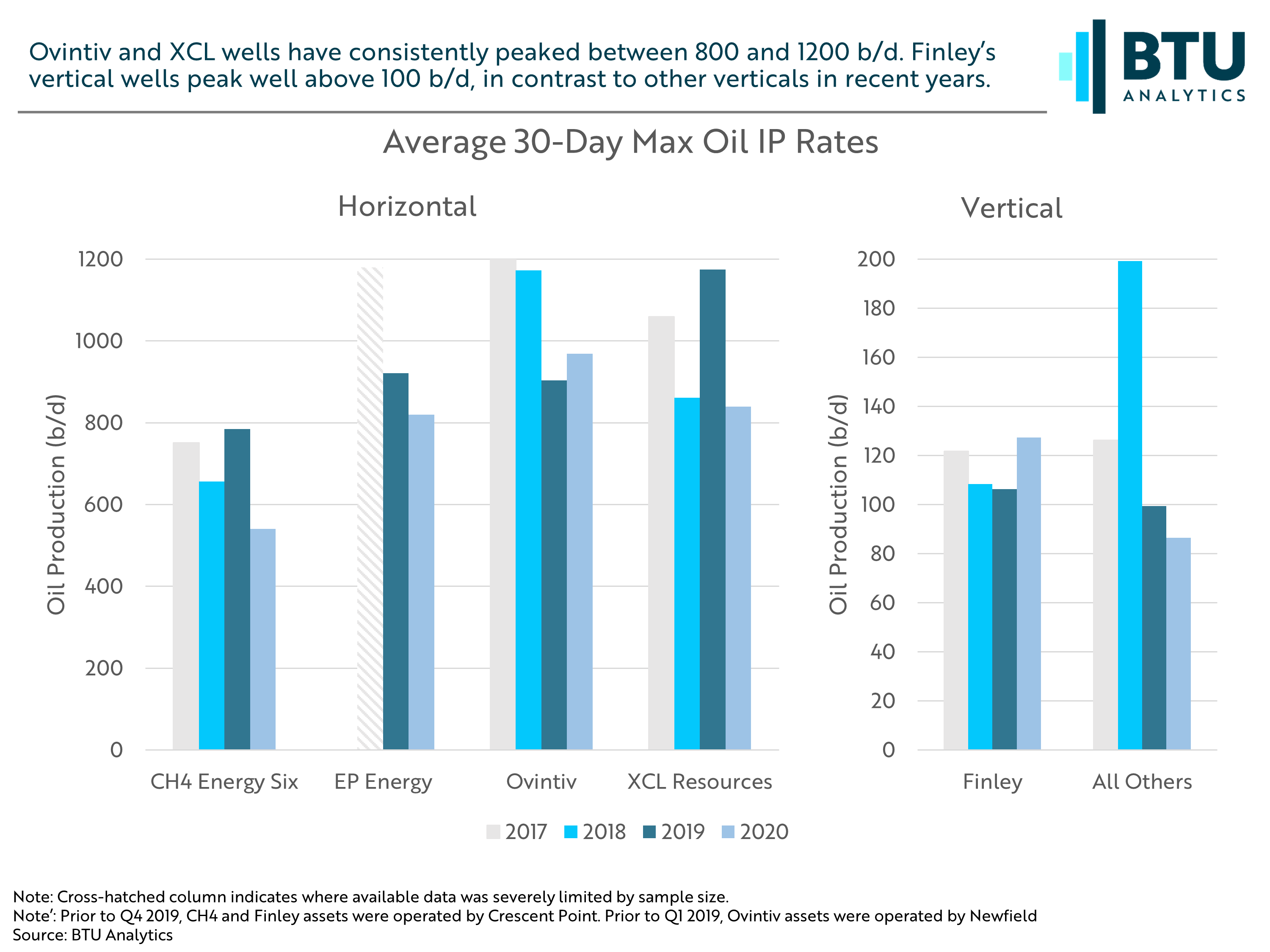

The formerly dominant local operators are no longer driving activity in the Uinta, with four other players developing their local presence. Since 2019, Crescent Point Energy has exited the play, and Ovintiv has been slow to develop its Uinta holdings. Ovintiv’s purchase of Newfield Exploration in 2019 gave the company a substantial foothold in the basin with high-performing wells. However, while Ovintiv has resumed drilling, its recent activity remains below pre-Covid levels, and the firm continues to prioritize other assets in the Permian, STACK, and Montney basins. According to its 1Q 2021 earnings report, only 5% of Ovintiv’s capital expenditures were directed to the Uinta in 2020.

Having emerged from bankruptcy, EP Energy is also falling below its 2019 benchmark. However, unlike Ovintiv, EP has made clear that Uinta will be a key focus for the firm going forward, with two rigs operating in the basin throughout 2021.

Drilling by three private E&P companies has largely driven the recent increase in activity. XCL Resources particularly has outpaced all other horizontal drillers in the basin. With 14 horizontal wells spud in 2021 to date, the company is on track to double its 2019 rate of drilling. Average 30-day max IP rates, consistently between 800 and 1200 b/d, put XCL’s productivity in the same tier as Ovintiv’s.

Meanwhile, the Uinta holdings of Crescent Point Energy, which were sold off in 2019, are now being developed by CH4 Energy Six and Finley Resources. Taking over Crescent Point’s western fields, CH4 continues to drill horizontally with wells historically peaking between 500 and 800 b/d. Finley is taking a unique strategy in Crescent Point’s eastern fields surrounding Ouray, UT. Virtually the only operator drilling vertically, Finley has already spud 46 vertical wells in 2021.

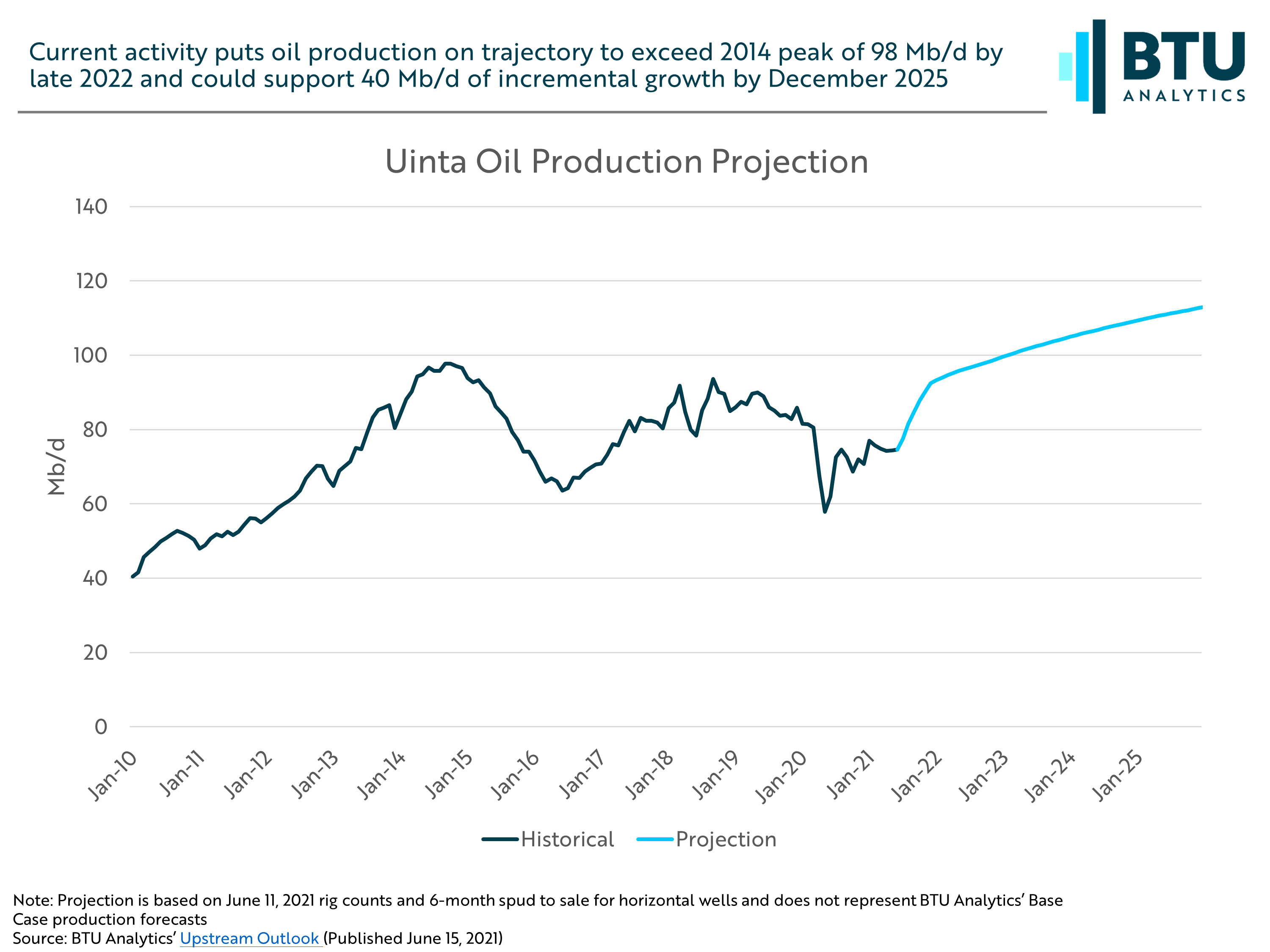

Based on current vertical and horizontal rig activity, projections call for Uinta oil production to reach its 2014 peak of 98 Mb/d by 2022. Continued activity at current levels through December 2025 would add 40 Mb/d of incremental crude production from the current level. Sustaining this rate of activity, however, faces headwinds given the limitations of regional midstream and refining capacity.

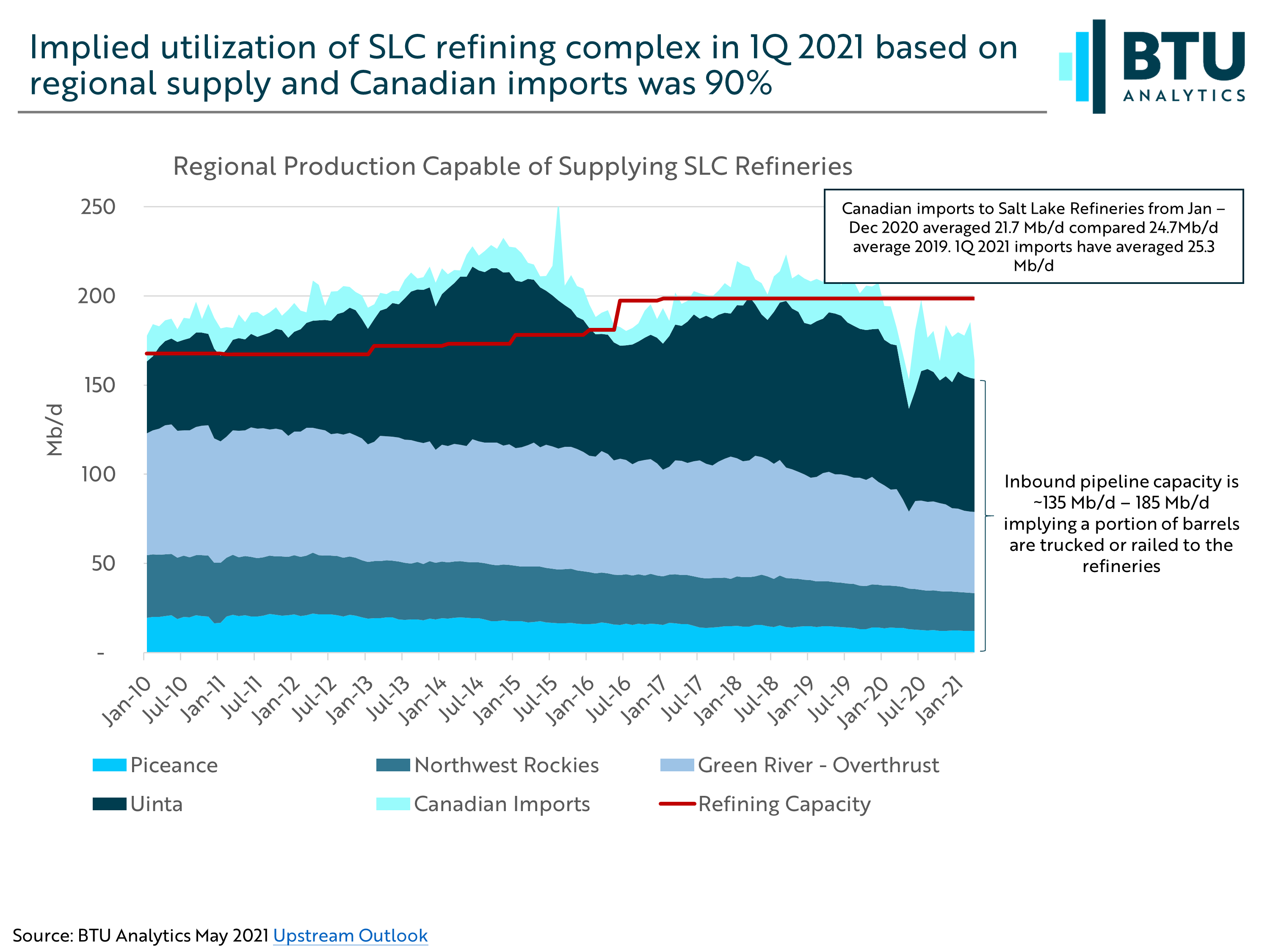

As of 1Q 2021, Salt Lake City refineries had access to 155 Mb/d of regional crude supply and an average of 25Mb/d of Canadian imports. This implies a 90% refinery utilization rate in the Uinta basin’s primary market. If Uinta production swells by 40 Mb/d and Canadian imports are held constant, a total of 220 Mb/d would be available to supply the 200 Mb/d refinery complex. Even if utilization increased to 95%, a surplus of 30 Mb/d of crude would need to be diverted into alternative markets.

A production increase of this magnitude would widen differentials for Utah crudes, as transport for surplus would require the more costly use of rail. A similar effect was observed during the historical peak of production in 2014, when implied Utah differentials approached -$17/Bbl. Moving forward, regional midstream constraints and a widening differential may check the pace of development in the Uinta.

For more analysis and regional production forecasts, see BTU’s Upstream Outlook.