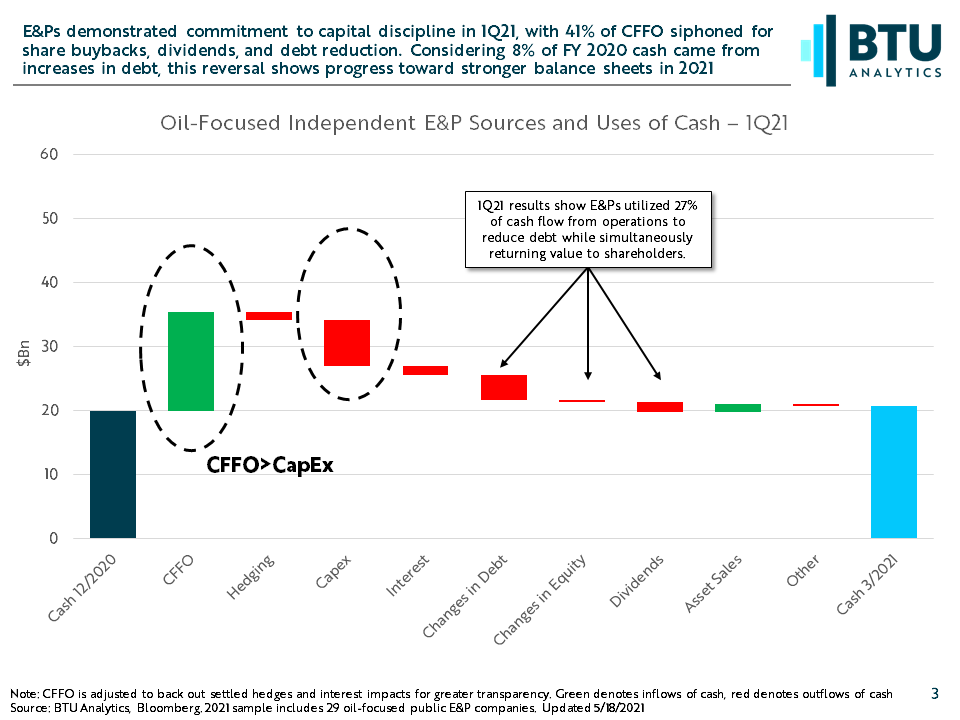

At the end of 2020, many E&P companies vowed to maintain capital discipline when releasing their 2021 plans regardless of newfound commodity price strength. Producers highlighted significant shifts in how they would deploy the cash flow they generated. The shifts favored lower reinvestment rates, greater debt repayments, and returns to shareholders. In 1Q21, E&Ps remained committed to capital discipline by reducing debt, conducting share buybacks, and issuing dividends from the cash generated from higher oil and natural gas prices. As a result, reinvestment rates have dropped. This drop in reinvestment rates challenges the rate of drilling and completion (D&C) activity recovery that has historically accompanied rising commodity prices. Today’s Insight will examine changes in E&P spending behavior and quantify what lower reinvestment rates could mean for production in major basins.

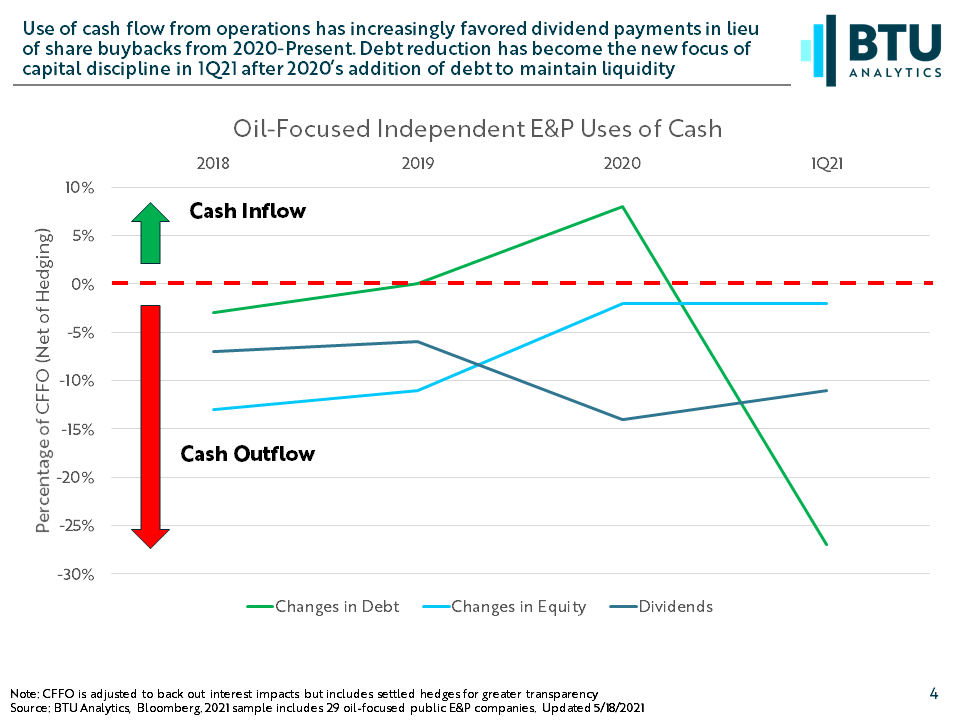

Last year’s commodity price volatility forced E&P companies to deviate from their mantra of capital discipline to keep the lights on amid black swan events like WTI trading below zero in April. Early in the pandemic, producers drew on revolving credit facilities to bolster liquidity and some later issued new debt to pay down revolvers that were at risk of being cut during redeterminations. With crude demand slowly starting to return and continued supply cuts from OPEC+, WTI ramped from $50/bbl by the end of 2020 to the mid-$60’s in 1Q21. Historically, this would have tempted producers to divert additional capital into the ground; however, most oil-focused producers instead funneled additional cash into debt reduction. In fact, many public independents highlighted that they would only reinvest between 50% and 70% of the cash they generated back into the field, far below years past where E&Ps plowed nearly all their cash flow into capex. As the chart below shows, independents reinvested just 50% of their cash flow from operations (CFFO) into capex last quarter.

The greatest debt reduction by company in the sample came from EOG Resources, which repaid $750MM in bonds that reached maturity in February. EOG intends to reduce net debt by $2B through 2023, with the remaining $1.25B currently expected to be repaid in 2023. The next largest reduction came from Continental Resources, which has accelerated its debt reduction from $5.53B at YE20 to below $4B by YE21 (assuming $60 WTI), with $560MM repaid in 1Q21. Devon, Pioneer, and Ovintiv each paid down over $400MM of debt in 1Q21, as well. Strengthening balance sheets after recent M&A is also driving debt reduction as consolidation heated up in the latter half of 2020 and year to date.

In addition to updated debt reduction targets, EOG announced a special cash dividend of $1 per share with its 1Q21 results, totaling ~$600 MM to be paid above the standard dividend and will be disbursed in July. Similarly, Continental doubled their quarterly dividend, which will be paid in May. As shown above, the overall shift to returning capital through dividends in lieu of share buybacks continued among independents in 1Q21, marking a reversal from 2018 and 2019’s buyback-centric returns.

While greater capital discipline among E&Ps is here to stay, the magnitude of that discipline can have significant impacts on longer term production. BTU Analytics highlighted in the March Upstream Outlook Report that the oil price assumptions underlying most producers’ 2021 budgets were quite conservative, typically between $35/bbl and $55/bbl. With 1Q 2021 WTI pricing averaging closer to $60/bbl, E&Ps were able to pay down 70% of the net additions to debt from 2020. Several producers have since revised their free cash flow projections higher in 1Q21 earnings announcements and cited assumed prices closer to current levels. Producers generally have three options for where to direct this additional cash flow: debt reduction, shareholder returns, and capital expenditures.

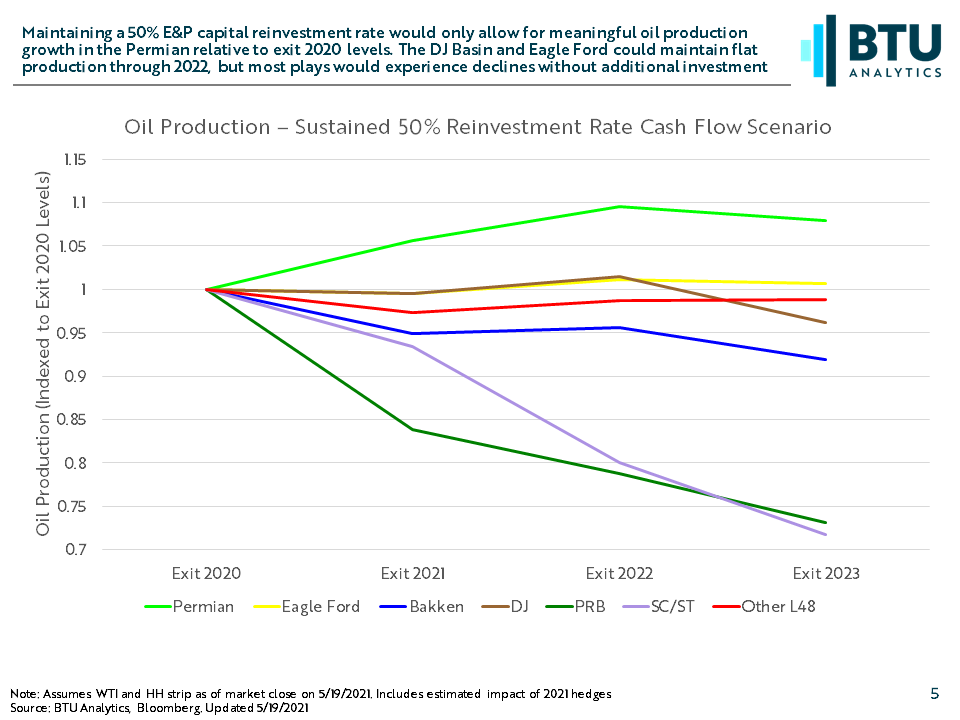

The Shale 3.0 paradigm calls for capital discipline to keep production growth in check regardless of newfound commodity price strength, but can sustain reinvestment near 50% even maintain flat production? For most plays, as illustrated in the chart above, the answer is no (barring improvements in well costs and productivity). Permian Basin oil production could grow relative to exit 2020 levels under current conditions, but most plays would decline at sustained 50% reinvestment rates, especially in 2023 when strip pricing begins to deteriorate, causing cash to dry up in most basins. It should be noted that hedges on 2021 production limit producer-specific realized prices, which BTU Analytics also covered in our March Upstream Outlook Report.

Balancing flat to modest oil production growth targets against promised capex budget indifference to commodity price increases could put several public E&Ps between a rock and a hard place in 2021. If commodity prices continue to provide cash beyond what E&Ps budgeted for, do they dare break their promises to increase D&C budgets and prop up production by exit 2021? For the latest analysis of producer commentary and forecasted production and well counts, check out our Upstream Outlook Report. To learn more about how recent well economics could be driving changes to basin profitability, request information about BTU Oil and Gas View – Economics.