With India as the latest country to announce shelter-in-place restrictions to combat the spread of COVID-19, BTU Analytics has estimated the 2Q 2020 impact of COVID-19 will be lower global liquids demand by an average of 8.6 MMb/d. This virtually overnight destruction of demand, coupled with the unraveling of coordinated production cuts from Saudi, Russia, and other OPEC nations has sent crude prices spiraling into the $20/bbl range from above $60/bbl at the start of 2020. Even as the industry slashes budgets and furloughs completion crews, the question remains, will it be enough? What does it take to offset not only global demand destruction from COVID-19, but also increasing production from Saudi, the UAE, and Russia? Will US producers be forced to shut-in oil production?

**BTU will be hosting a complimentary webinar on April 7 entitled, “What Price Makes US Shale Viable?”** REGISTER HERE

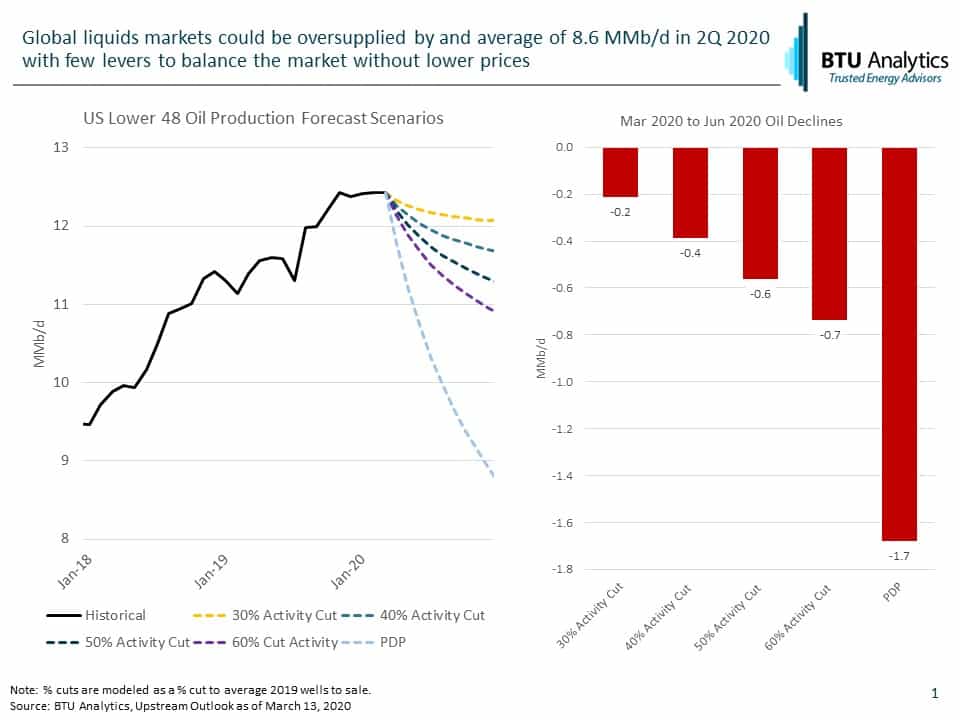

BTU’s latest estimates imply that global oil markets could be long by over 9 MMb/d in 2Q 2020, which leaves very few levers that can be pulled in a timely response. Below is a chart showing the production path over the next 3 months for US Lower 48 oil production under different completion cut scenarios. Even if US producers halt all completion activity today and do not complete any additional wells for the remainder of 2Q 2020, US oil production would be expected to decline by only 1.7 MMb/d, well short of the over 9 MMb/d supply reduction needed to balance the market in 2Q.

This means that we will need to see lower prices to drive responses beyond just activity reductions in the US and other nations. One of the options that is already in play, and quickly becoming a growing concern, is injecting excess crude supply into storage, or using crude tankers on the water as floating storage. The US exported almost 3.5 MMb/d in December 2019, which must compete for the same crude tanker stock in demand for both floating storage and increased exports from Saudi Arabia. If this 3.5 MMb/d of crude oil for export cannot find a ship to be loaded onto, it could begin a domino effect through connected crude markets, with the ultimate impact being oil shut-ins.

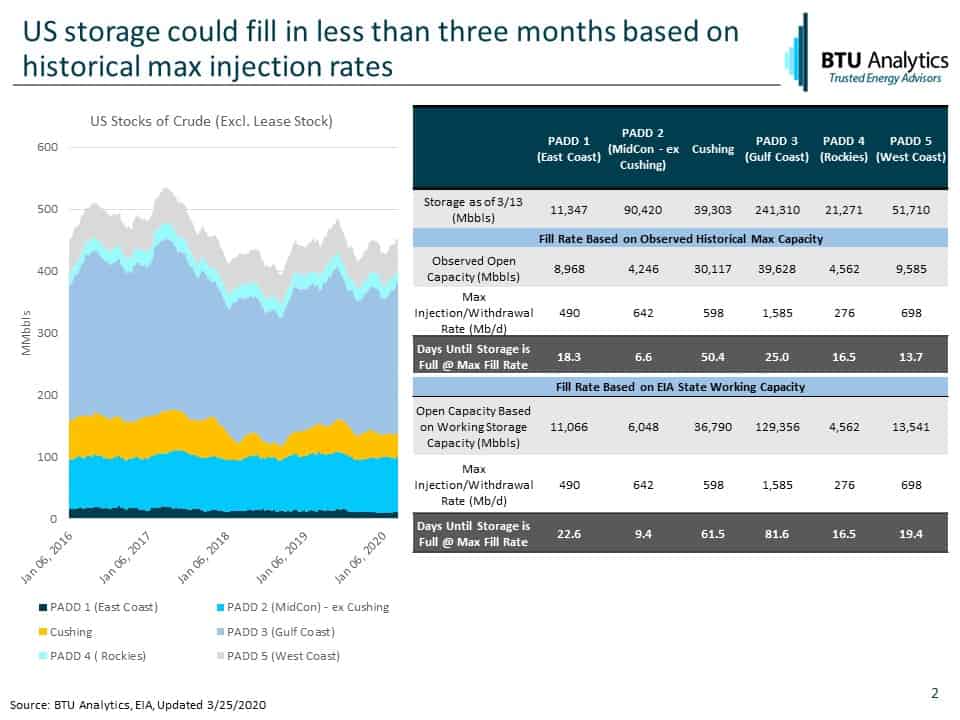

As another data point, the slide above calculates how many days it would take for the US to fill up existing crude storage capacity by PADD based on historical max daily injection rates. Without a change in the current trajectory of fundamentals, US storage bottlenecks are likely to begin emerging, leading to further price impacts and producer shut-ins.

Storage is just one piece of the complex puzzle that is the global market for crude. To stay on top of the drivers in today’s rapidly changing environment we are currently offering our existing clients one-on-one webinars with our latest thoughts on the outlook for gas and oil markets. If you are not currently a client but would like to schedule a one-on-one presentation, please submit an inquiry HERE.