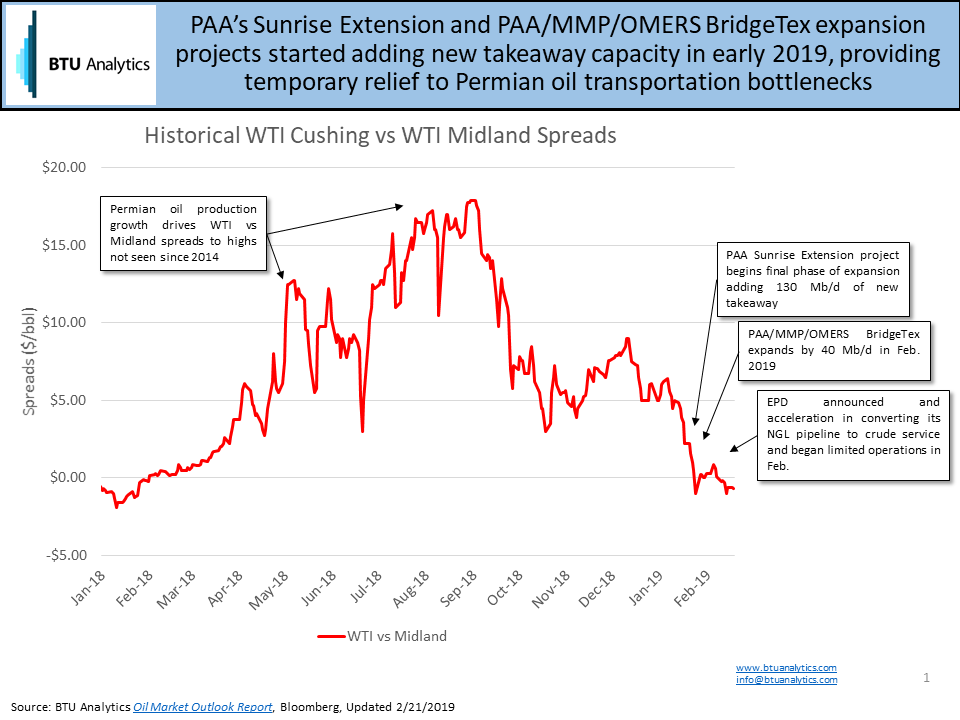

In 2018, the spread for WTI quality crude at Midland versus Cushing captured headlines. The spread widened to almost $13/bbl in May before reaching new peaks of almost $18/bbl in September. Fast forward to February 2019 and the spread between Midland and Cushing has collapsed. Midland is now at a small premium to Cushing by an average of $0.52/bbl since February 11. Both prices, though, remain at a significant discount to crude oil prices in Houston and St. James markets. The widespread is a direct result of Cushing pipeline bottlenecks. Not surprisingly, several new project announcements and open seasons have occurred to debottleneck the Cushing pipeline network. However, are these projects really necessary to tighten spreads between Midland, Cushing, and the Gulf Coast?

Starting with the Permian, three brownfield projects have been relieving pressure on Midland differentials in January and February. First, the final phase of PAA’s Sunrise Extension project entered service to Cushing. The project has contributed to the tightening of the Midland to Cushing differential by transferring supply to Cushing. Second, the BridgeTex pipeline expanded. The addition of 40 Mb/d of capacity from Midland to the Houston market lifted Midland prices further. Finally, Enterprise announced an accelerated timeline for the conversion of the Seminole pipeline from NGL to crude service. Limited service on the converted line began in February. By April of 2019, the line will add 200 Mb/d of new takeaway capacity to the Gulf Coast. BTU Analytics expects this new capacity to fill quickly and forecasts Permian production to grow by 230 Mb/d in the first half of 2019. As a result, differentials at Midland should remain wide to the Gulf Coast.

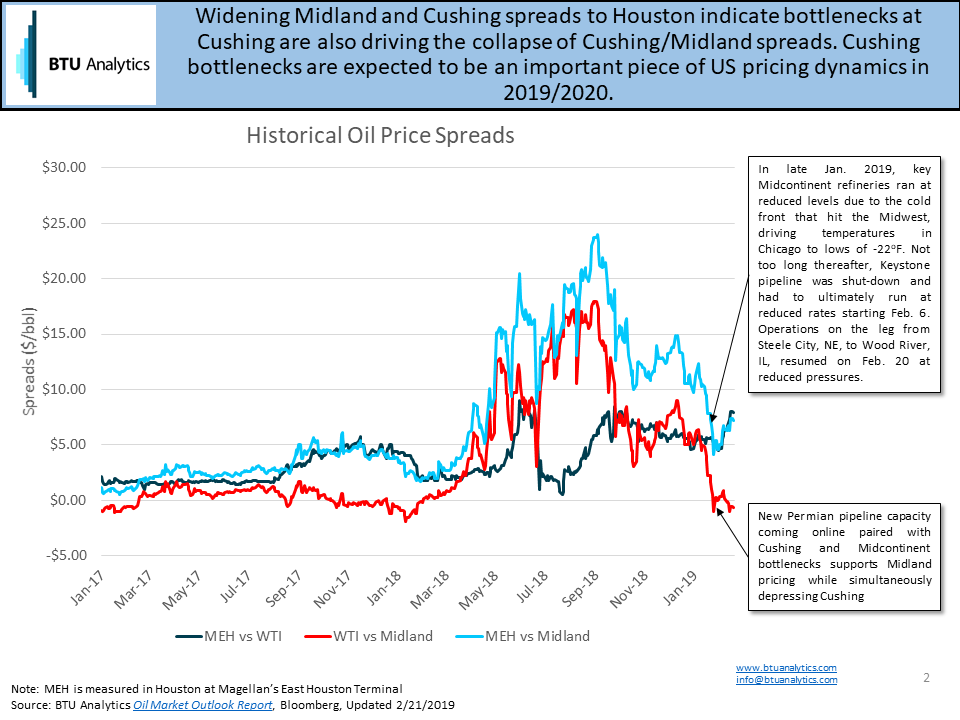

Additionally, Cushing pipeline bottlenecks are emerging in force, depressing Cushing prices. Small additions to Permian pipeline capacity to Cushing is only one piece of the puzzle in depressed Cushing prices. The chart below shows the spreads between Cushing, Midland, and Houston. At the same time, Cushing to Midland spreads have improved, the Cushing and Midland spreads to Houston (MEH) have widened driven by weather and pipeline disruptions. In late January 2019, Midcontinent refineries ran at reduced levels due to the cold front that hit the Midwest. Arctic temperatures in Chicago with lows of -22 F resulted in operational curtailments. Additionally, the Keystone pipeline was shut-down from Steele City, NE to Wood River, IL on Feb. 6, 2019. The outage resulted in additional supply hitting Cushing. The leg to Wood River resumed service on February 20 at reduced pressures providing the option to divert supply back to the Wood River refinery.

The pipeline outage and lower refinery runs are short-term disruptions. However, new pipelines out of the Rockies and Canada are expected to increase supply into Cushing and the Midcontinent. The increased spreads this winter due to pipeline and refinery outages highlights the tightness of pipeline capacity between Cushing and the Gulf Coast. Thus, should new supply enter the equation, then the market is ripe for new pipeline projects to the coast. Publicly, nine oil pipeline projects have been announced to address this bottleneck and allow US and Canadian producers to tap into premium coastal and global markets. In order to help our clients keep track of the Cushing and Gulf Coast markets, BTU Analytics recently added a page to our Oil Market Outlook report tracking Cushing to Gulf Coast pipeline projects. Additionally, BTU Analytics will be adding forecasts for LLS and MEH pricing based on pipeline and export facility tracking in the March Oil Market Outlook report.