any of our consulting projects over the years have included an analysis of well economics in specific areas or work on comparative economics with a focus on the marginal cost of producing oil and gas in North America. The recent drop in oil prices has changed our discussions from “How and when will this play/acreage be developed?” to “Does anything work at this oil price?”.

The short answer is that the vast majority of unconventional plays targeting oil in North America are currently out of the money when you consider differentials for transportation and quality. Which presses another question — with completions representing over 50% of the well cost for horizontal wells, are we nearing a point at which it makes economic sense to defer well completions? If we aren’t there, what sort of scenario might bring that to reality?

Let’s play with Bakken well costs and production data and see what those numbers tell us about the economics of deferred completions.

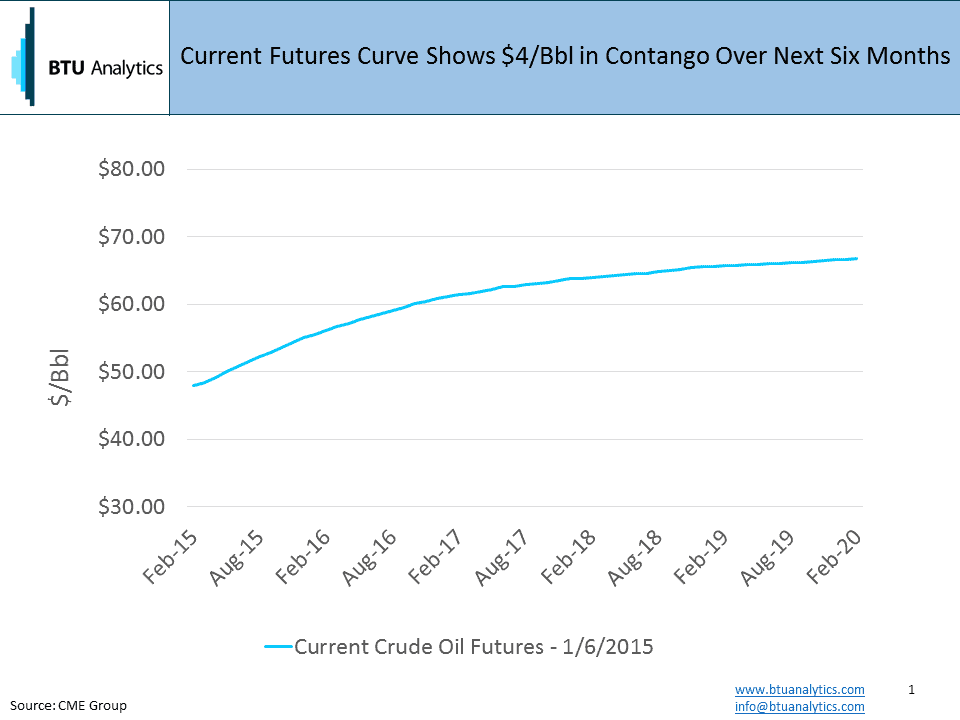

For the prospect of deferred completions to make sense, you need contango in the futures curve and/or falling service costs. (Contango occurs when future prices are higher than the spot price.) The WTI curve below shows the February contract settled at $47.93/bbl yesterday. Looking forward six months, the August contract settled at $52.23/bbl, or $4.30 higher than February. Looking out a year, the February 2016 contract settled $8.19/bbl higher.

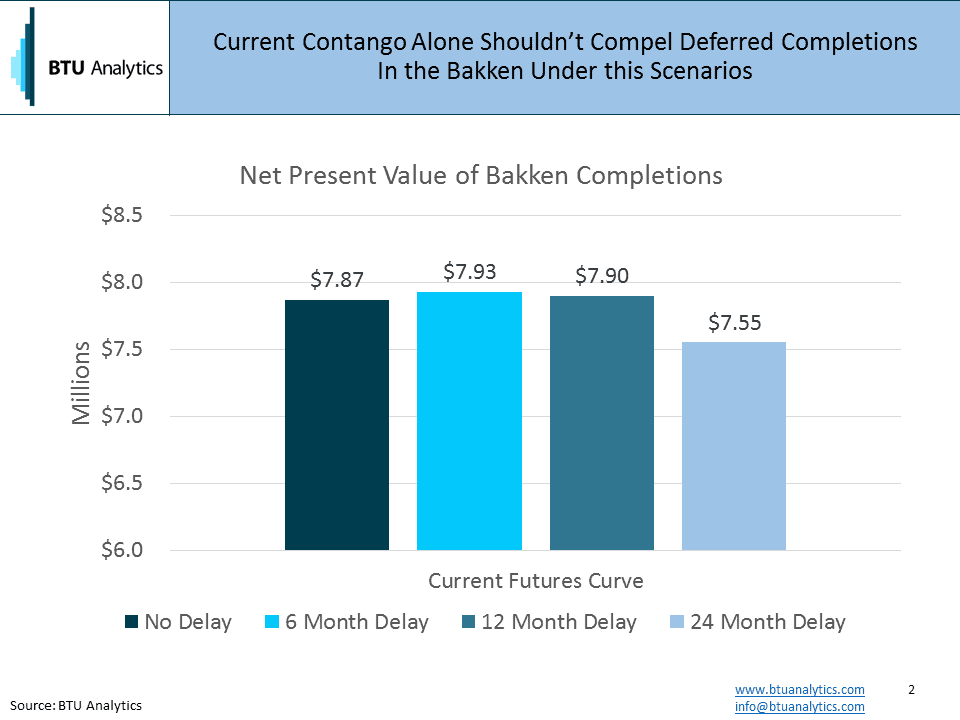

Does the current contango incentivize deferred completions? Assuming in this case a well cost of $9.2MM and that the well completion represents 60% of the total cost of drilling and completing a well, we calculated the net present value (NPV) effect of delaying the well completion. For those of you who aren’t financial types or the financial types who haven’t had enough coffee yet, let me take a few steps back to explain what factors are at play in this economic model.

Unconventional wells are known for production profiles marked by high decline rates over the first year of production. Generally, this decline is somewhere in the 55% – 75% range. So all else equal, a producer would like the first year of production to occur in a higher price environment. But what keeps a producer from waiting years to drill and (or) complete that well? The time value of money concept is one of the guiding principles of finance. If we assume monetary inflation (and generally we do) a dollar today is worth more than a dollar a year from now. So for this analysis, we are looking at the futures curve to see if the allure of higher oil prices in the future is enough of an incentive to wait to complete a well (and delay a well’s highest rates of production until prices are higher) taking into account that $1.00 a year from now is only worth about $0.91 today assuming a 10% discount rate.

The resulting calculations of net present value created from the $5.5 MM cost of completing the well are charted below. Note that the drilling cost of these wells is already sunk, so it is not considered in the analysis. Delaying the completion of the Bakken well by six and twelve months did very little to change the economic value of that well compared to the immediate completion. In the 24 month delay case, the NPV is actually lower despite the well benefiting from higher oil prices due to the discount rate applied to those cash flows.

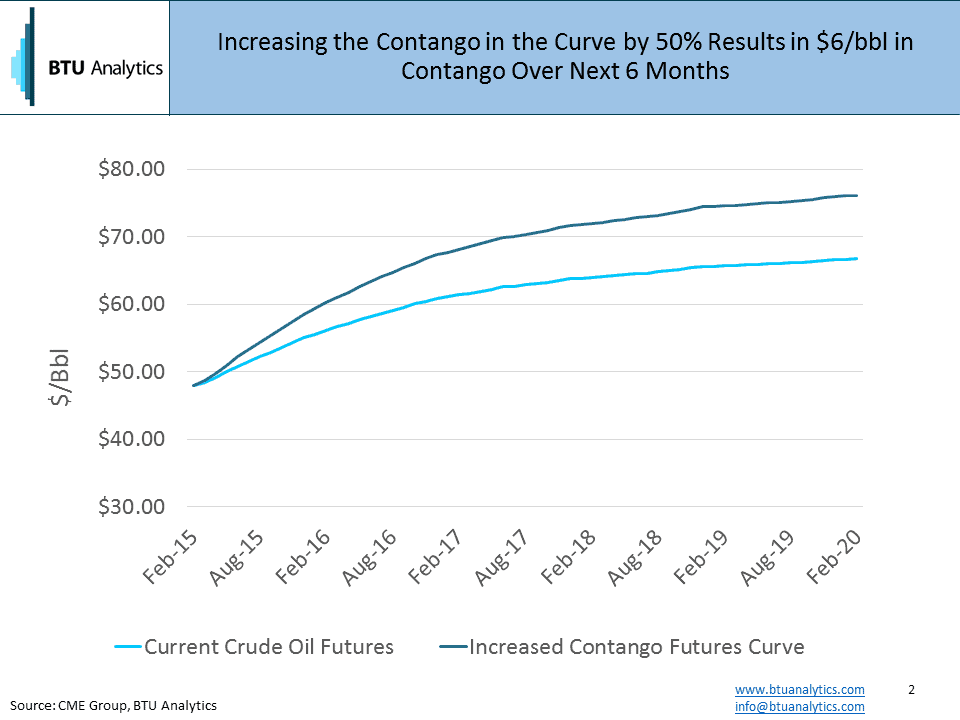

But we couldn’t end the analysis there. How much contango do we need to make deferrals feasible? The chart below shows what the futures curve looks like if we increase the curve contango by 50%. This would assume that we would see $6.45/bbl of contango over six months and $12.29/bbl over twelve months. Could this be enough to promote the idea of deferring well completions?

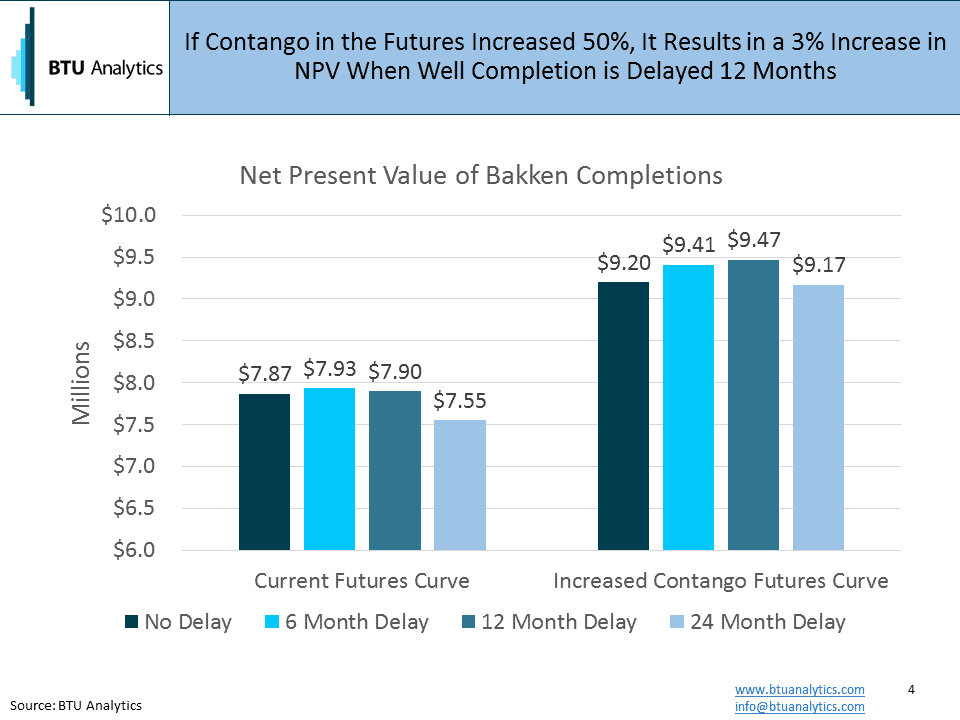

The next chart shows the result of the increased contango on the net present value. Ignore for a moment the fact that these NPV levels are higher, they are higher because we assumed higher prices. For this analysis, the real focus is the variance between the numbers, and that deferring the completion twelve months results in a value 3% higher than completing the well immediately.

Three percent isn’t much to cheer about. For this Bakken example at least, contango alone doesn’t provide a compelling change in value creation.

But contango in the futures curve isn’t the only factor impacting the economics of deferred completions in this market.

Yes, here comes the teaser.

For a more robust analysis of deferred completion economics, including the potential impact of falling service costs, discount rates, and other considerations, see BTU Analytics’ forthcoming edition of the US Upstream Outlook.