We look forward to seeing you all at our first annual, What Lies Ahead conference in Houston this Thursday. If you haven’t already done so, you can sign up HERE

Last week, BTU Analytics looked at reconciling producer reported results surrounding the SCOOP and STACK plays with IP rates reported from the state of Oklahoma. This gave us the idea to dig deeper into some of the well results that producers touted as big successes in the past year.

In an ideal world we would be able to pull real-time individual well data to verify reports by producers. However, state level data can be prohibitively lagged, so what can we do to get around that? While not as satisfying, we can look at producers’ past claims and verify those against state reported data, to better understand how operators report well results.

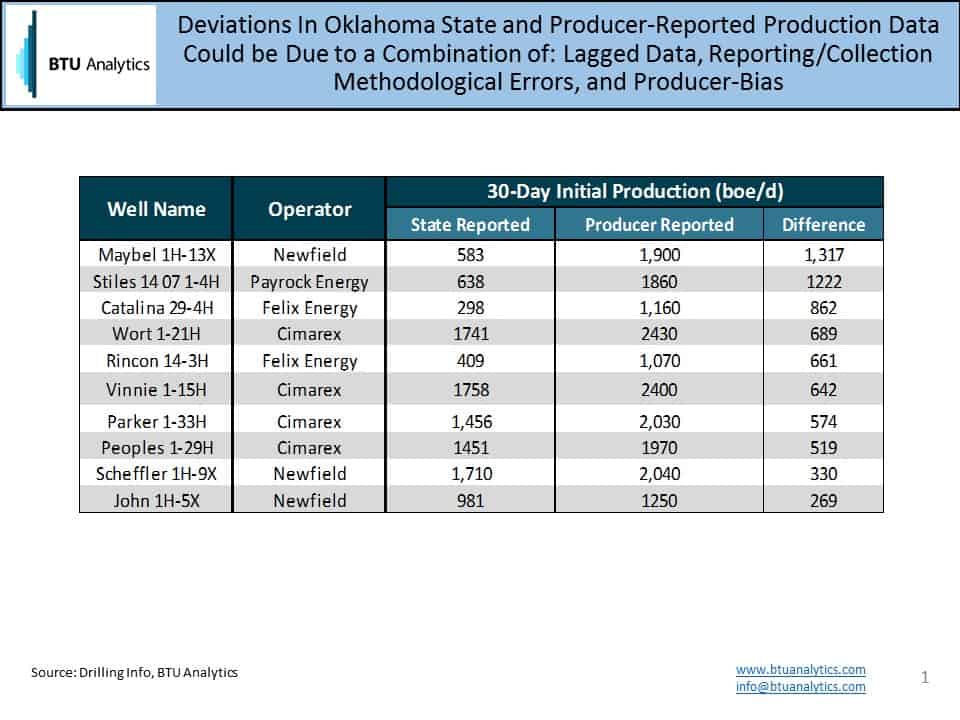

Keeping with last week’s post, let’s look at a selection of wells from the SCOOP and STACK.

Figure 1.

While each well shows a much larger producer reported initial production rate than what is reported to the state, there are several possible explanations other than operator over-promotion. The largest driver of deviation is in how BTU Analytics calculates IP rates from state-reported data. In order to derive clear and consistent IP rates for plays across the country, BTU Analytics looks at monthly well-level data and determines the first full month of production. For most shale wells, this first full month of production is the maximum production reported over the life of the well, and by dividing that production by the number of days in the month we calculate a 30-day IP. Unfortunately, in some states, data collection by state agencies is not always robust or occurs at the lease level and can muddy the waters when trying to match individual wells with producer reports. In Oklahoma, reporting responsibilities are bifurcated between two agencies: the Oklahoma Corporation Commission (OCC) and Oklahoma Tax Commission (OTC). Because of their unique motivations for collecting production data, the state-wide data can be incomplete in places. Along similar lines, the discrepancy between monthly reported state data and producer daily data from the field by operators can also cause variation.

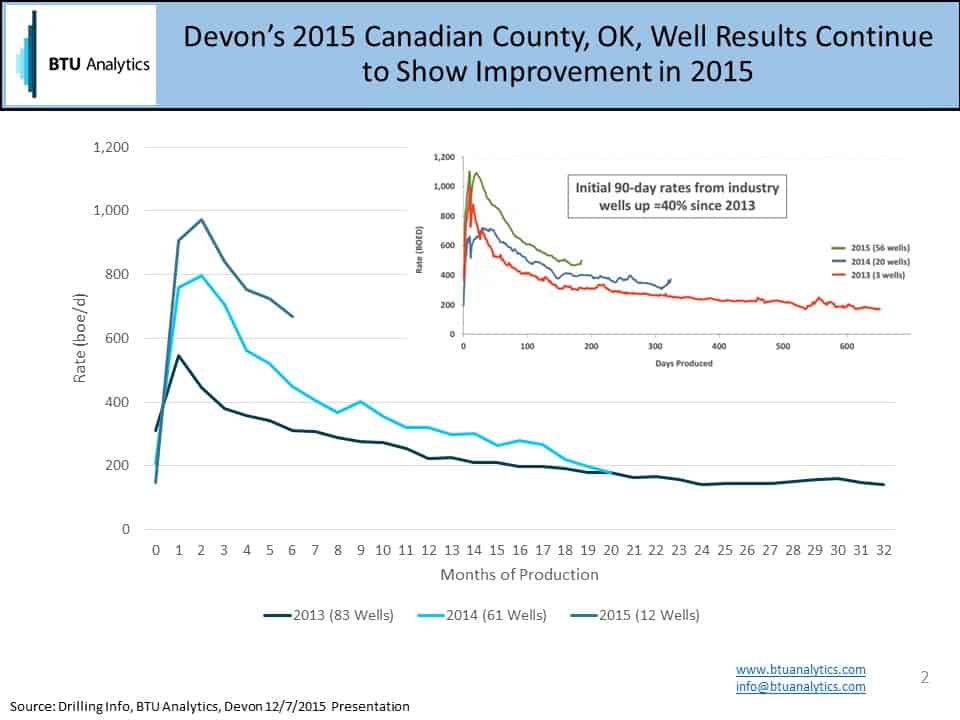

So for the reasons listed above it is not always reliable to match data on a well level, but nonetheless there is still information to be garnered from aggregating the data. Let’s take for example, Devon’s STACK wells, and compare what Devon reported in a December 2015 presentation against what we are seeing in the state reported data. The graphic below shows the type curves gleaned from state reported data with Devon’s reported results for Canadian County, OK.

Figure 2.

While the state reported data from 2013 and 2014 deviate from Devon’s reported data, likely from differences in aggregation by plays or target formations, we can see that 2015 data has so far been tracking with results reported to the state. The gains that are being reported and showing up in Oklahoma data are driven by improving drilling and completion designs. Devon reported that its 2015 gains are driven by increasing lateral lengths, more frac stages, higher proppant volumes, and a conversion to slick water fracs with diversion. As producers continue to explore and develop the SCOOP and STACK, BTU Analytics will be watching both producer-reported and state-reported data to determine if this will be one of the drivers of gas and oil growth despite weaker commodity pricing.

While Devon’s data appears to be consistent with investor material, deviations in the IP rates in Figure 1 highlight the fact that data is not always clean or unbiased. There are several reasons to cross check both producer and state data to ensure that results make sense. Differences in calculation methodologies, cherry-picked results, and state-reporting errors apply not only applies to Oklahoma, but to many places in the country, making it important to look at information not only at a well-level but also holistically in the context of all major US plays. As a data-oriented shop, this is a problem we are all too familiar with and we use several outside data sources to supplement, validate, and triangulate on accurate type curve and IP rate assumptions for our production and economics models.

To learn more about our economic models and BTU Analytics’ market outlook, be sure to attend our first annual What Lies Ahead Conference in Houston on Thursday.