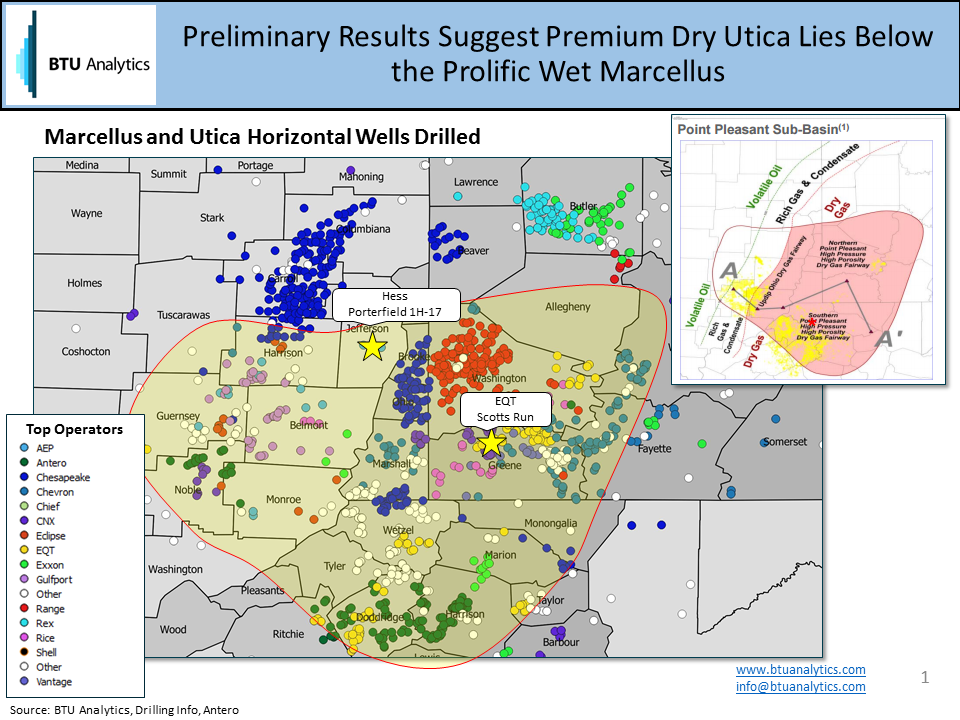

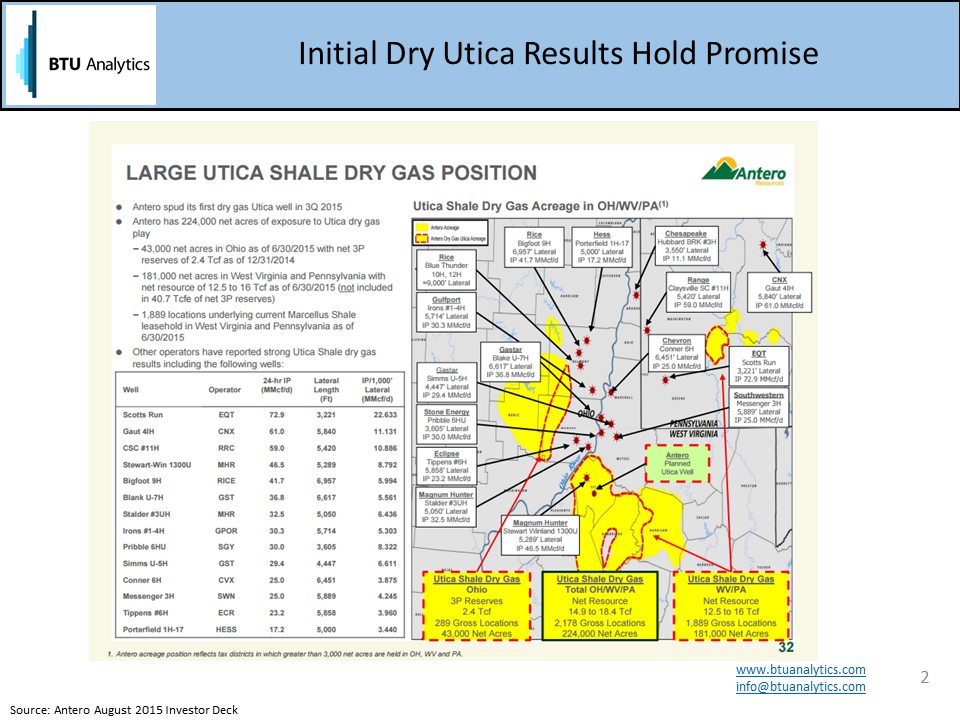

The last thing the market needs is another gas play as prolific as the Marcellus shale. The US is still reeling from, and trying to quantify how, a constrained Marcellus will reshape the landscape once all of its transportation constraints are relieved. In fact, BTU Analytics is publishing a paper (A Firm Dilemma) explaining our view of how market dynamics will change when projects like the Rex East-to-West reversal are completed this fall or when ET Rover is completed in 2017. However, E&P companies are generally rewarded for unlocking new reserves and it seems as though they have found the next big gas play that could rival the Marcellus and Wet Utica – the Dry Utica (Point Pleasant formation). The extent of the play is still being explored, but early reports by Antero Resources (NYSE: AR), Range Resources (NYSE: RRC), and Magnum Hunter (NYSE: MHR) (to name a few) have showed promising results in Southwestern Pennsylvania, the northern panhandle of West Virginia, and eastern Ohio. Shell (NYSE: RDS.A) has even reported Dry Utica drilling as far north as Tioga County, PA.

To-date, only a handful of wells have been drilled, but are exhibiting impressive IP rates. Reported 24-hr IP rates range from 17.2 MMCf/d for Hess’ (NYSE: HSE) Porterfield 1H-17 in eastern Ohio to 72.9 MMcf/d for EQT’s Scotts Run well in Greene County, PA.

EQT’s (NYSE: EQT) Scotts Run reported an initial 24-hr wellhead flowing pressure of 8,641 psi. In the seven days since they have restricted flow, the psi has averaged a pressure of 9,563 psi. In comparison, typical pipeline line pressure is between 750-1,500 psi.

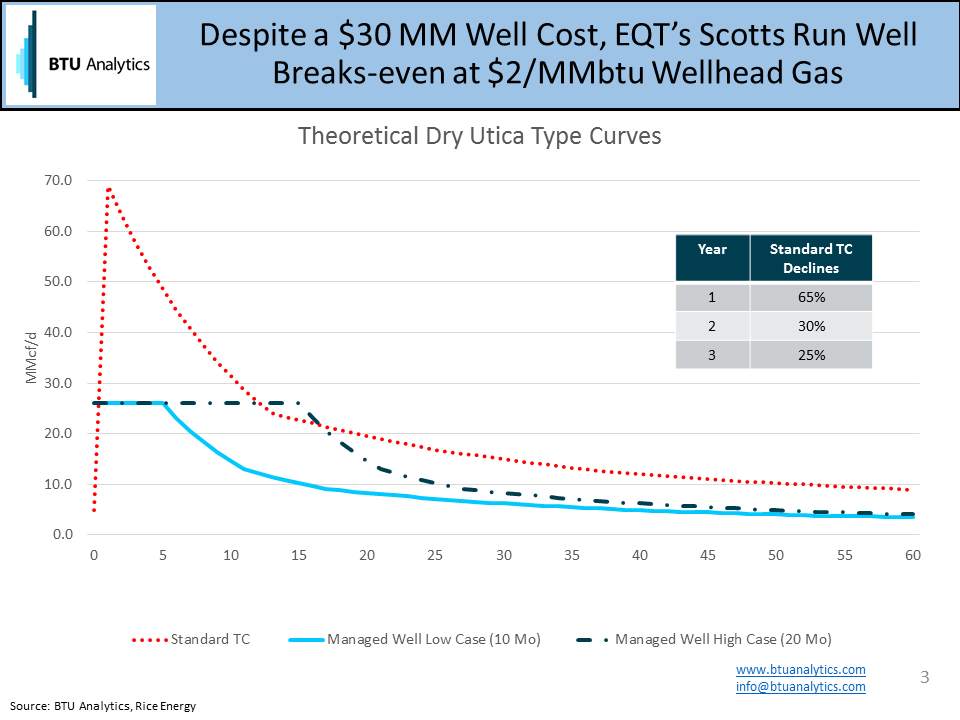

Let’s talk about why this matters to well economics. Well pressures are one of the variables that dictates how wells decline, so depending on what assumptions you make, you can come up with varying type curves; and type curves significantly impact well economics. For this analysis, three different type curves and two well pricing assumptions were used to analyze the potential breakeven point for the monster EQT well. The first type curve assumes that Scotts Run will decline at a standard 65% in the first year and 30% in the second year and is allowed to flow unrestricted (ignores any line pressure issues). The second and third type curves were developed based off of assumptions Rice Energy (NYSE: RICE) has published for its Bigfoot 9H well which had a 24-hr IP rate of 41.7 MMcf/d and is also being restricted due to high line pressure issues. Rice Energy has modeled two cases for expected pressure declines. In the High Production Case, the pressure of the reservoir declines at a rate of 12.5 psi/d before reaching line pressure. The second, Low Production Case, assumes a higher rate of pressure decline at 25 psi/d. Once the well pressure equalizes with the line pressure, the well begins to decline at a more typical first year decline rate of 65%. Applying these parameters to the EQT well, the High Case pressure decline creates a type curve that is flat at 26 MMcf/d for 20 months, and the Low Case generates a type curve that is flat for the first 10 months before declining.

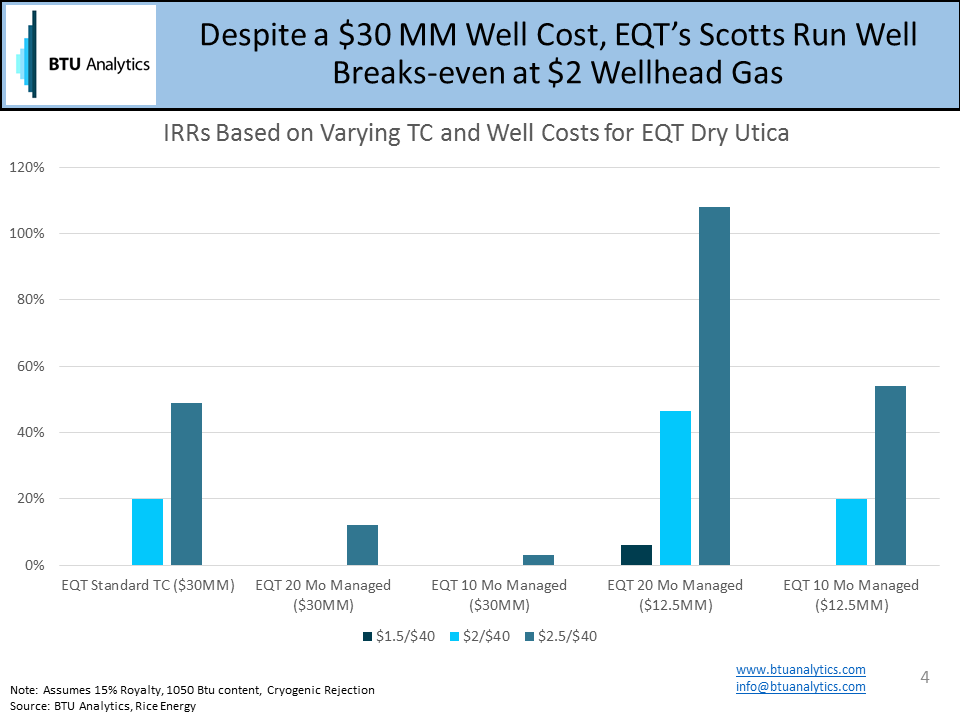

Pairing these type curves with the actual $30 MM well cost, and then with EQT’s projected development cost of $12.5 MM, shows that the Dry Utica has the potential to extend the supply of drilling locations with sub $2.50/MMbtu breakevens. Flowing freely, Scotts Run only needs $2.00/MMbtu gas to breakeven despite a $30 MM well cost. Using the restricted type curves and the targeted $12.5 MM well cost, IRRs for the High Case well at $2.00/MMbtu are over 40% and sky rocket to 108% if wellhead gas prices reach $2.50/MMbtu. While there are still many unknowns, as producers move up the learning curve for the dry Utica, the IRRs, even choked back, suggest that economics could be comparable or even better than the wet Marcellus which sits just above the Dry Utica, especially in a depressed liquids pricing environment. This would allow producers like Range, Chesapeake (NYSE: CHK), EQT, and Rice, who are already drilling Wet Marcellus in this region to substantially increase reserves and have the flexibility to switch between formations depending on commodity prices. While Dry Utica drilling is still in its infancy, early results are encouraging. The Dry Utica poses a significant opportunity for another sub $2.00/MMbtu gas play and is another risk to a production rebound in the Haynesville and other higher-cost gas plays across the US and Canada.

For more BTU Analytics Energy Market Commentary and to get our commentary directly in your email sign up here!

{kind=link}