One of the highlights from BTU Analytics’ What Lies Ahead conference last week was that the Eagle Ford has emerged as one of the few plays where infrastructure constraints wouldn’t limit production upside over the next twelve months. (Yes, that means that infrastructure is impacting growth almost everywhere else. For the details on this analysis, find out how to become a client of our Upstream Outlook service here.) Many of the larger independents have shifted investor focus and capital away from the Eagle Ford to fund growth in the Permian, with some looking even to divest out of the Eagle Ford entirely. What does this shift mean for Eagle Ford activity and production volume? Is there even hope for Eagle Ford upside?

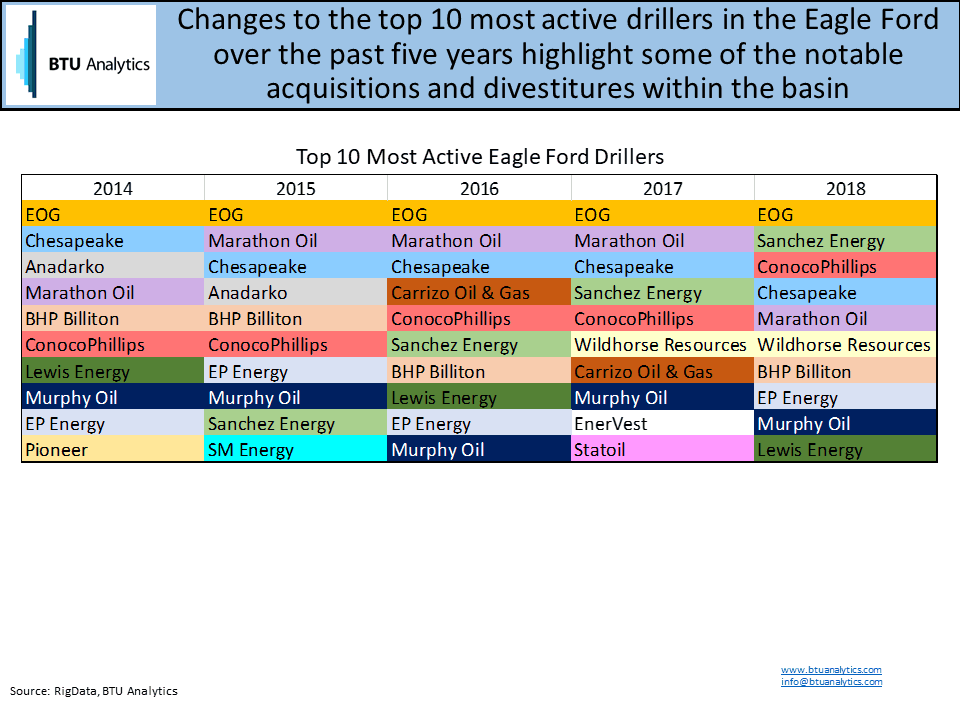

The table below highlights the top 10 operators as measured by wells drilled over the past five years. While many of the names on this chart show steady placement, the names that fall out of the top 10 over the last two or three years illustrate a key part of the narrative around the Eagle Ford’s future.

In 2014/2015, Anadarko was in the top 5 operators, with Pioneer and SM Energy also making appearances on the top 10 list. Anadarko sold its Eagle Ford assets in early 2017 to Sanchez Energy and Blackstone Group, exiting the basin to focus on opportunities in the Delaware Basin, DJ Basin and deepwater Gulf of Mexico. Pioneer has announced plans to divest the company’s Eagle Ford assets in 2018 as part of a plan to become a Permian Basin “pure play”. SM Energy has divested non-operated assets in the Eagle Ford and is expected to spend only 14% of the company’s 2018 drilling and completion budget in the Eagle Ford, with the remaining balance being spent in the Midland Basin. BHP Billiton has also been a top 10 operator in four of the last five years. However, the company has announced that it plans to divest its onshore US shale assets, a process which is expected to occur this year.

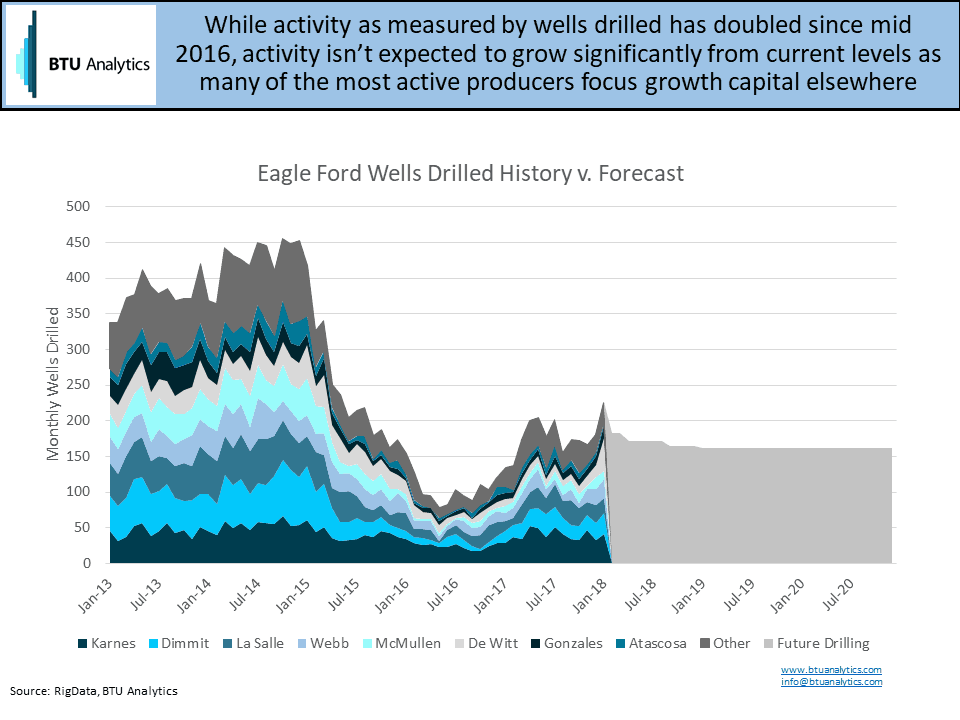

Sure, some producers are leaving the Eagle Ford, but every transaction needs a buyer on the other side, right? Private equity capital has been behind a number of buyers of Eagle Ford assets, but it is too early to say what that will mean to near-term activity and associated production. A look at drilling activity shows that drilling has more than doubled since the trough in mid-2016, yet is still less than half of the record activity in late 2014 and early 2015.

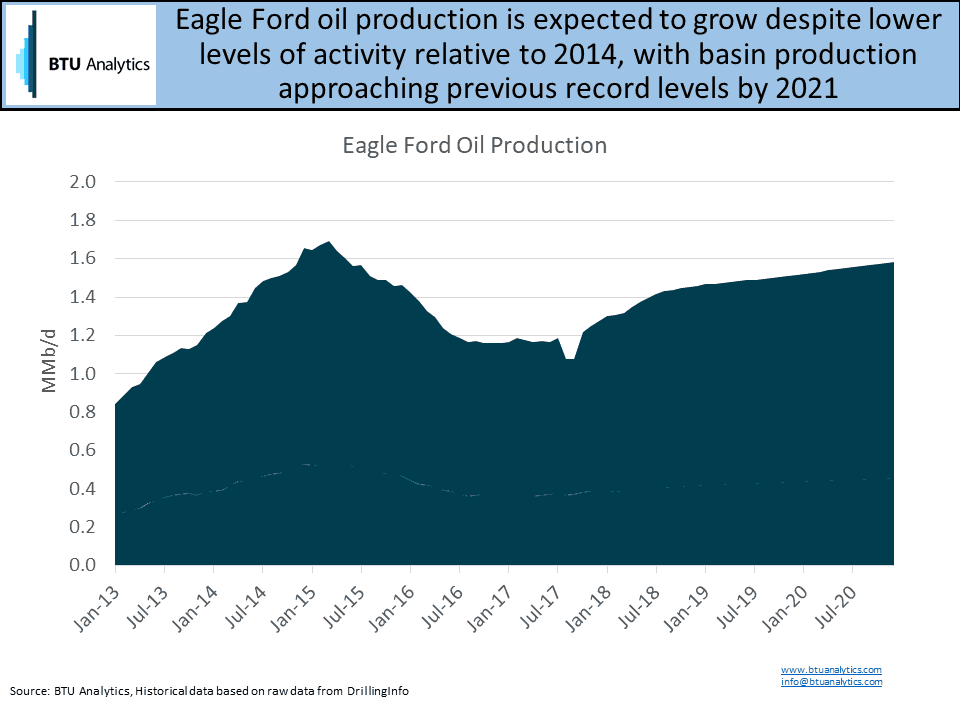

However, this level of activity is enough to grow production back to almost 1.6 MMb/d by the end of 2020, as shown in the next chart.

Unlike other regions, there is upside potential to this forecast, as Eagle Ford oil and gas takeaway and processing aren’t currently at the upper limits of utilization being tested in other plays. Perhaps Eagle Ford upside is not that far off?

For more information on BTU Analytics production forecasts, including the impacts of infrastructure on individual plays, request a copy of our Upstream Outlook.