The safety, security and convenience of modern life is often taken for granted. For much of the developed world, with the flip of a switch, the lights come on, our indoor environment finds a consistent temperature, sanitation happens, and hunger isn’t a primary concern. But providing this modern life to all the world’s people has impacted the climate as greenhouse gases accumulate in the earth’s atmosphere. Countries around the world are focused on expeditiously reducing greenhouse gas emissions, and policy makers are intent on crafting incentives and regulations that force market behaviors aligned with their goals.

The electricity sector was an early target of policy focus, and is transforming rapidly, with renewables contributing to grid decarbonization. But the goals of policy makers cannot be achieved without transforming other sectors as well – manufacturing goods and materials, transportation, agriculture/land use and waste being other catch-all categories for significant emissions. Notably, industrial demand is responsible for 36% of total liquid fuel and natural gas demand (EIA, 2020 IEO). Changes to energy intensive industries will have broad based impacts. Today’s energy market commentary focuses on laying the groundwork for understanding the emissions challenges in manufacturing goods and materials, setting a foundation for future analysis on the opportunities and challenges to decarbonizing specific industry sectors.

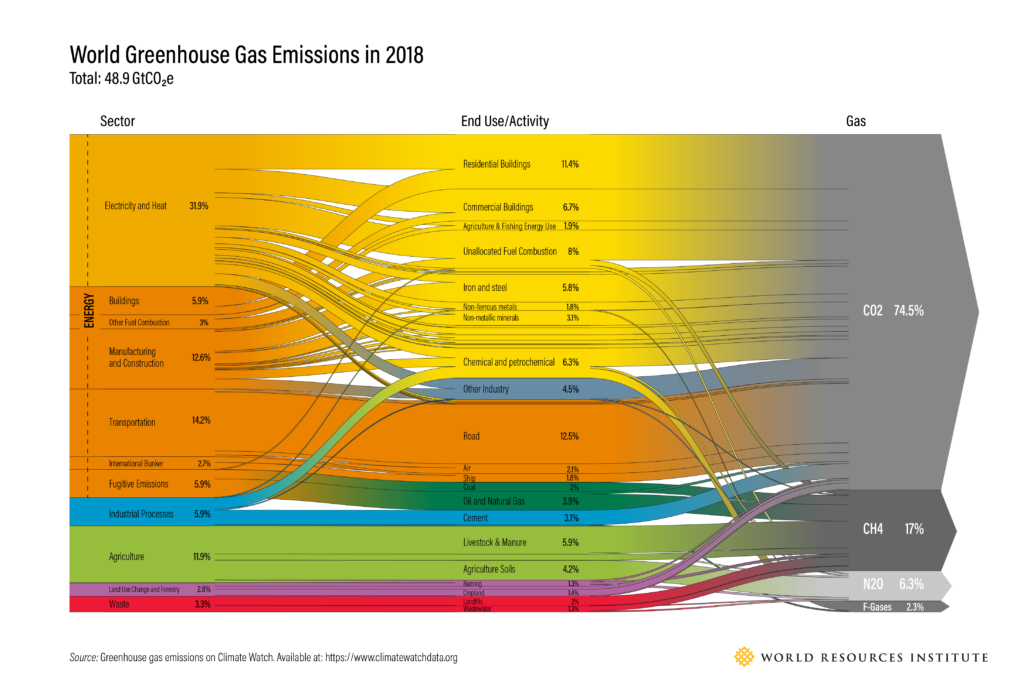

A global issue requires first understanding the data at a global level. The diagram below shows global GHG emission estimates from 2018 by sector, end use/activity and gas emitted. One immediate takeaway from the analysis from the World Resources Institute is that emissions from industry is highly dispersed. While no single end use/activity in the analysis makes up more than 13% of total emissions, end uses associated with activities we often think of as energy-intensive (iron and steel, non-ferrous metals, chemical and petrochemical, cement, and “other industry”) together represent 22% of emissions. Adding in other end use emissions such as non-metallic minerals, food and tobacco, machinery, and paper, pulp and printing brings those estimates closer to 30% of overall global GHG emissions.

Despite highly dispersed end-uses, the source of those emissions by end use tends to fall into three economic sector categories. Breaking down the ~30% of emissions associated with named industries in the previous paragraph, 13% of emissions from those end uses fall in the Energy: Manufacturing and Construction reported economic sector category, 12% in the Energy: Electricity and Heat and 5.7% in the Industrial Processes category. These categories provide early insight in the fact that transformation of the electricity sector will have downstream impacts for emissions from industry.

Changing industrial processes and businesses to reduce emissions will take pressure, whether from governments, capital providers or other stakeholders. Stakeholder pressure is likely to be disproportionately applied, with maximum pressure likely coming from companies with publicly traded securities or capital needs and in nations where regulatory regimes are mature and the population focused on the topic of climate.

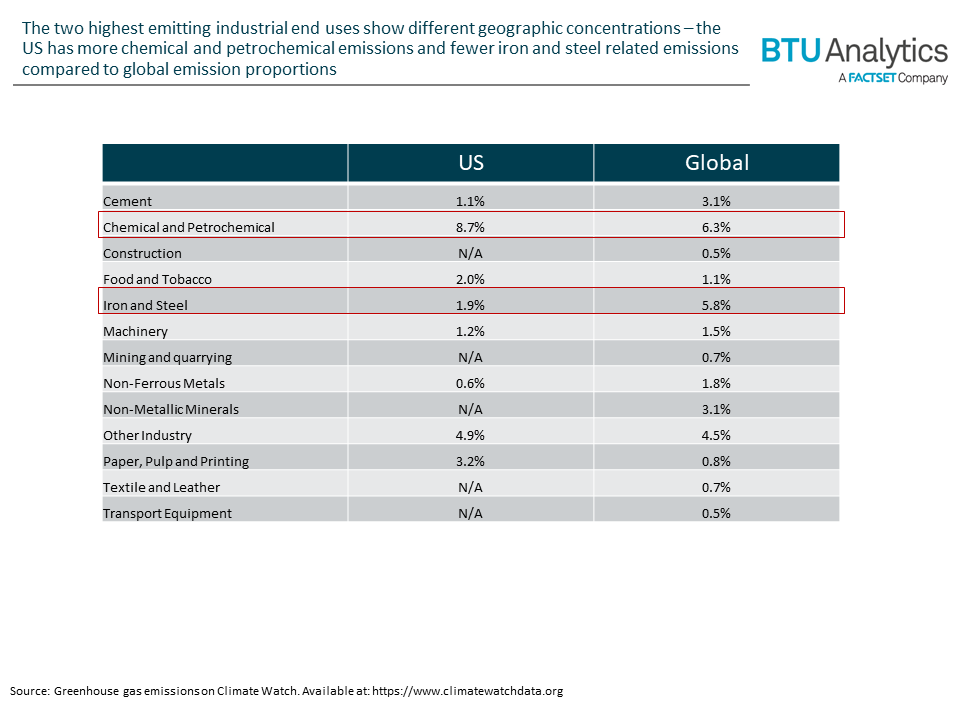

The potential impact of governmental pressure on industry is evident when comparing US industrial emissions to global emissions. The WRI published a similar analysis to the one above for US GHG emissions for 2018. A table below compares the proportion of emissions by end use to the global figures.

The two highest emitting industrial end uses show different geographic concentrations. Chemical and petrochemical production is concentrated in a few hubs around the world, often located near low-cost feedstocks. The US is one of those major hubs, due to the number of complex refineries located here. In contrast, iron and steel production is concentrated in China with 54% and 50%, respectively, of global operating capacity located in China, according to the Global Energy Monitor. Governmental policy intervention on iron and steel manufacturing in the US is not likely to be as impactful as the same intervention in China, and inconsistent governmental policy action across the globe is likely to relocate emissions rather than reduce them.

The world needs energy and manufactured goods and materials to support modern life as we know it. Technological breakthroughs in energy and industry are responsible for improving the quality of life for billions of people across the globe. However, emissions are squarely at the forefront of stakeholder concerns, and pressure to reduce emissions and decarbonize is likely to impact not only the electricity sector, but other energy-intensive industries as well. For more coverage of the impact of ESG pressures on the outlook for the oil and gas sector, request more information on our Upstream Outlook Service.