In 2021, US residential and commercial customers consumed 21.7 Bcf/d of natural gas and as a result emitted 467 MMtCO2e. By comparison, this represents slightly more than the total annual emissions of the United Kingdom. While there may be potential to lower net emissions through wider adoption of renewable natural gas or hydrogen, the prevailing strategy to date has been to propose replacing natural gas appliances with electric alternatives. This Energy Market Insight examines the opportunities and limitations for electrification of residential and commercial buildings, and what effect this may have on long run natural gas demand.

Since 2019, laws banning natural gas in new buildings have been passed in New York City, San Jose, San Francisco, Seattle and Portland, among others. More municipalities, including Los Angeles, have begun considering similar actions. In January this year, Governor Kathy Hochul of New York proposed a statewide ban to take effect 2027, while leaders in Rhode Island, Maryland, Massachusetts, and Washington state are weighing similar proposals. Simultaneously, incentive programs are encouraging the adoption of high efficiency electric appliances, including a $3.5 B federal appropriation inside of the recently passed Build Back Better Act. The extent to which these efforts displace natural gas demand will differ region-to-region, as can be seen by comparing New York state and California.

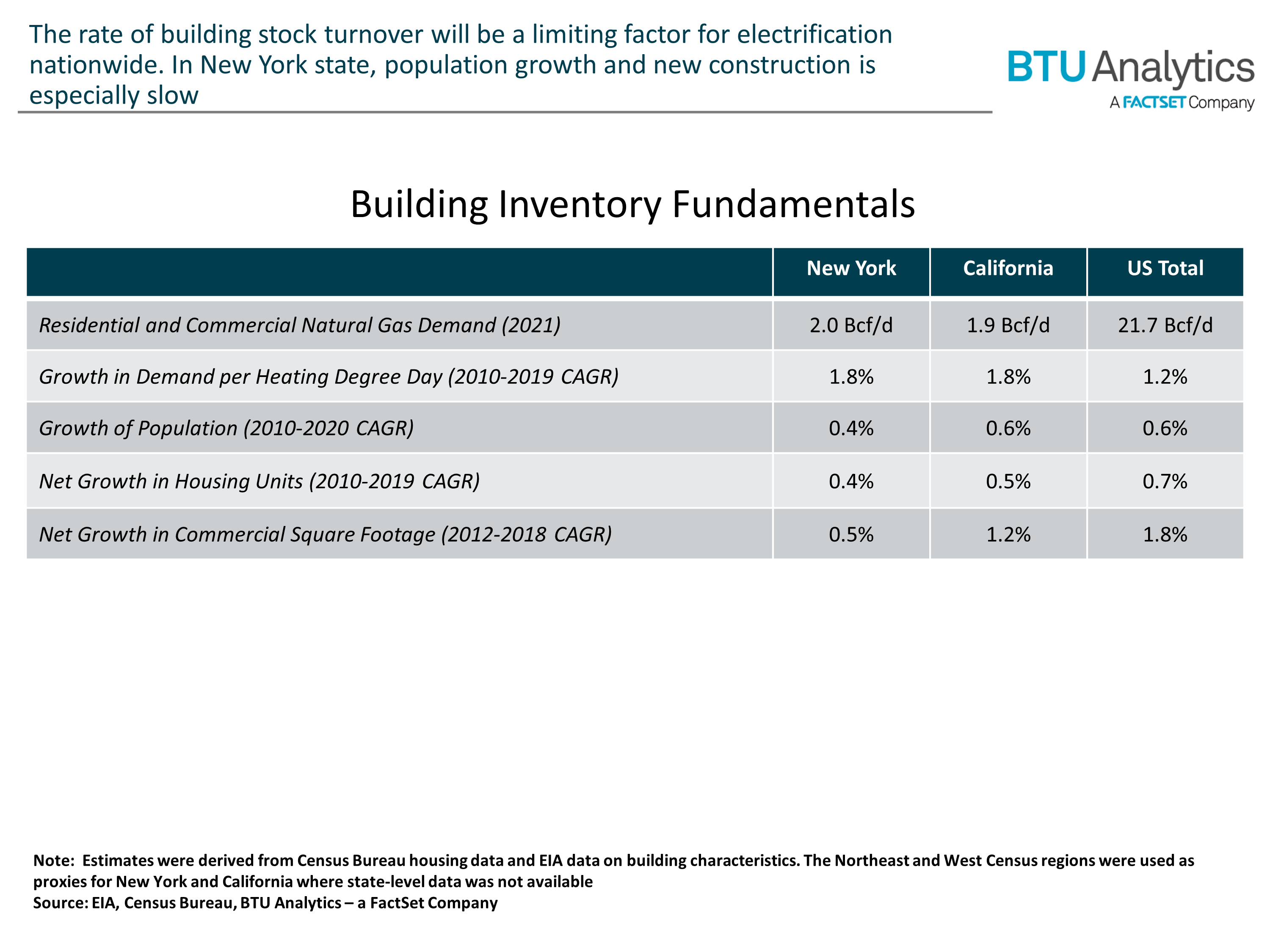

The table below shows trends in natural gas consumption, population, and new building construction for California and New York. In both states, population growth and building growth have contributed to steady growth of residential and commercial natural gas demand since 2010. However, population and building inventory in New York are growing slower than in California and nationally.

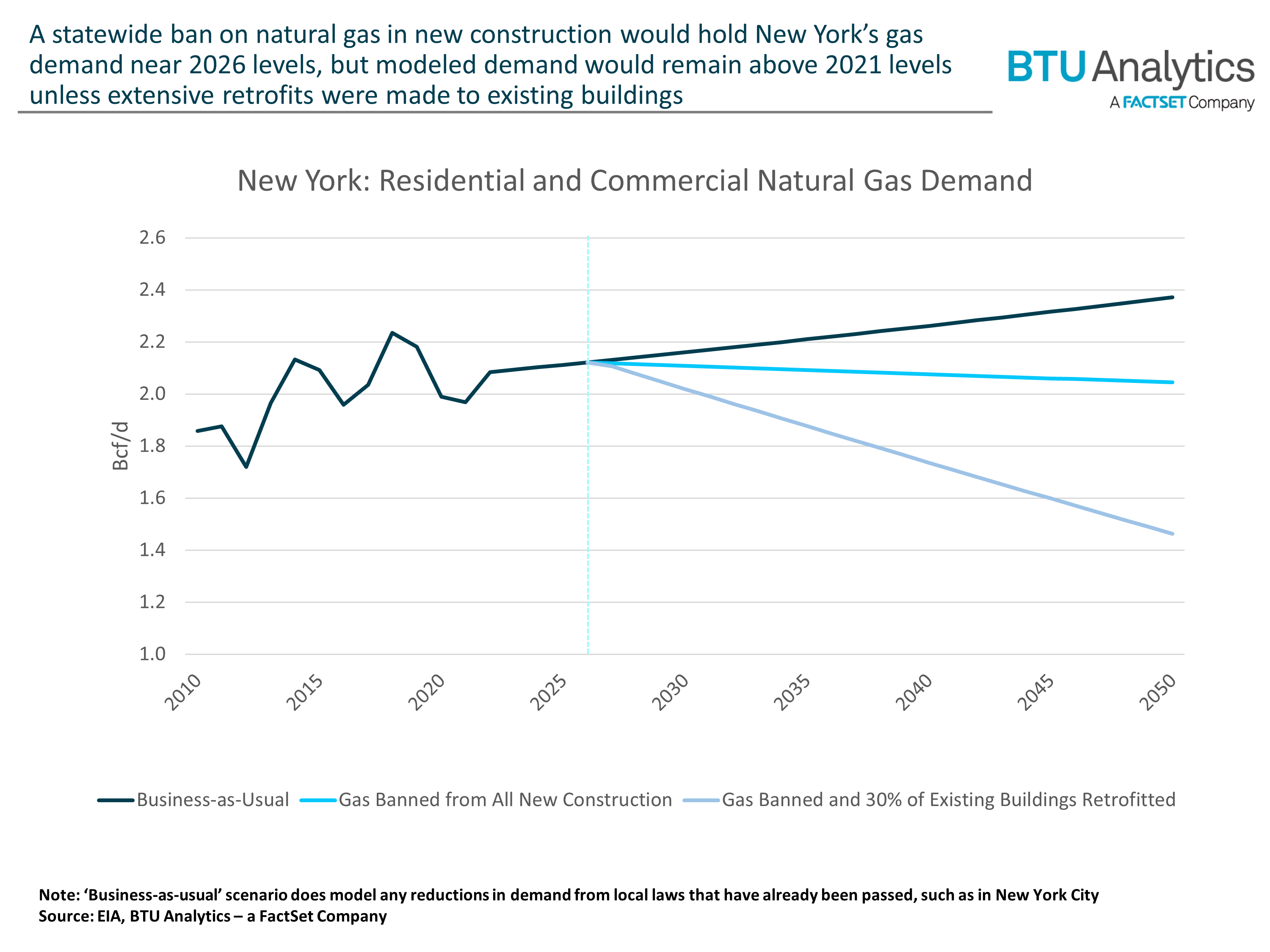

One limitation on the effect of a statewide ban on natural gas in New York would be the slow turnover of building stock. The comparison table above shows New York’s housing stock has grown slowly and only a small portion of older stock has been replaced each year. Commercial real estate is estimated to turn over at a faster pace of 0.4% compared to less <0.1% for housing units in NY. Using the growth rates above in residential and commercial building stock, natural gas demand in New York would be expected to continue to grow over the next 30 years as shown in the business-as-usual case below.

Even if New York passes a ban on natural gas in new construction and all new construction after 2027 was 100% electric, natural gas demand would only be expected to fall slightly after a 2026 peak of 2.1 Bcf/d. By 2050, natural gas demand would only be 0.1 Bcf/d lower than the peak in 2026 and 0.3 Bcf/d lower than a business-as-usual scenario. While this path would reduce the growth in emissions from natural gas in the residential and commercial sector, it would have little impact in reducing emissions from current levels.

For natural gas demand in New York to be significantly reduced, a portion of existing structures would have to be retrofitted with all electric appliances. If 30% of today’s already existing structures in New York state were electrified between 2027 and 2050, then a larger reduction in gas demand can be made: 0.9 Bcf/d from the business-as-usual case. However, this would require policy actions beyond the bans discussed above, likely including incentives that would make electric heating more cost competitive versus existing natural gas infrastructure.

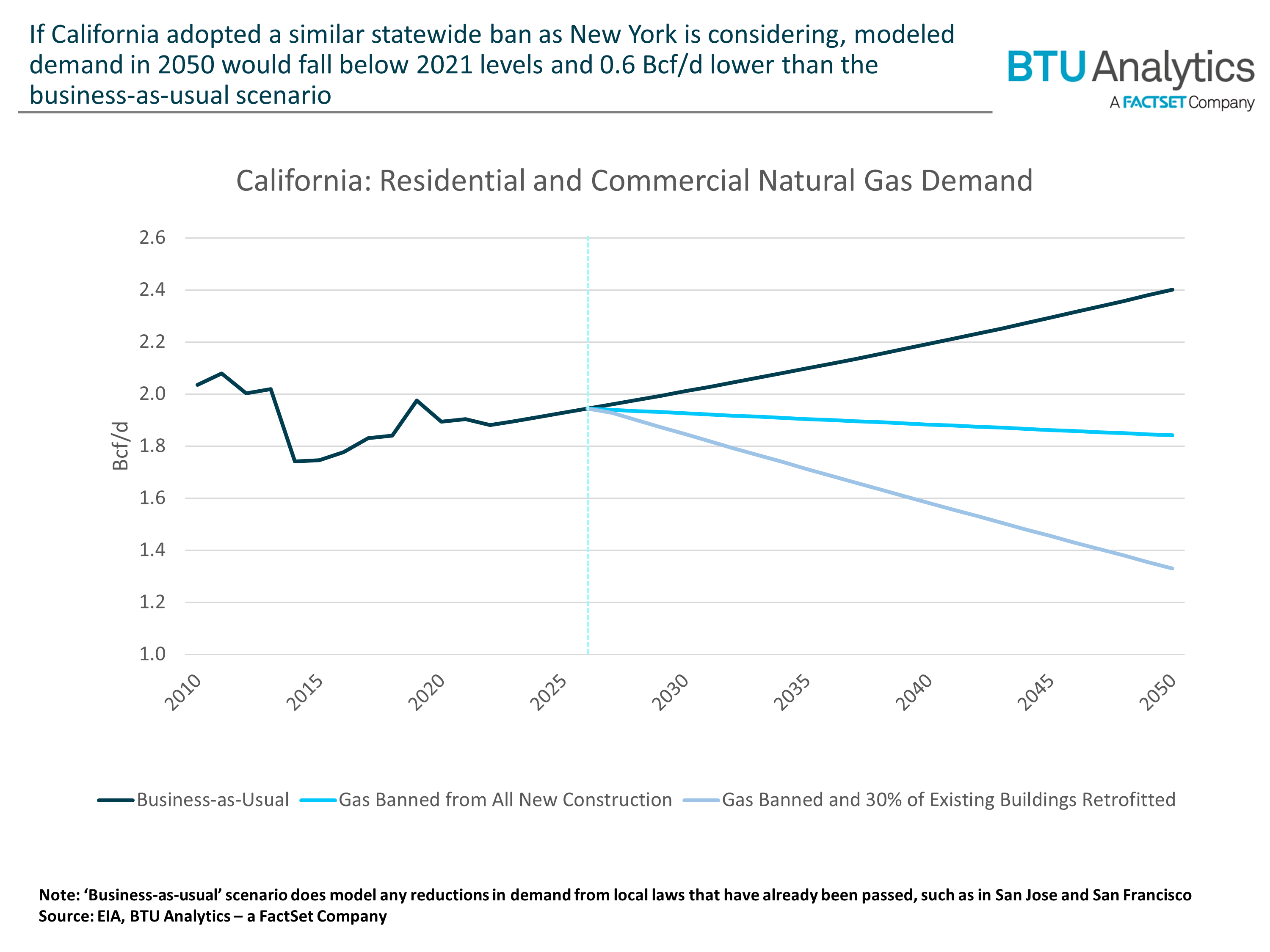

While California has a slightly higher replacement rate in existing construction than New York, the impact of ban on natural gas in new construction would affect natural gas demand similarly, as shown in the chart below.

Just like New York, California natural gas demand would be expected to grow in the business-as-usual projection over the next 30-years. If natural gas were banned from all new buildings in 2027, modeled demand would be 0.6 Bcf/d lower in 2050 compared to the business-as-usual scenario, but barely below current levels. To materially move demand, existing infrastructures would also need to be retrofitted. If 30% of existing structures were additionally retrofitted with electric appliances, demand in 2050 would be 1.1 Bcf/d lower than the business-as-usual scenario and 32% below peak 2026 demand.

While bans on natural gas in new construction would reduce the future potential of natural gas demand in the residential and commercial sector, the bans would have little impact in reducing consumption and thus emissions from current levels. In order to materially reduce demand, states would need to provide incentives to convert existing structures from natural gas to electric heat.

For more on the outlook for natural gas demand and emissions from the natural gas sector, inquire about BTU Analytics’ Long Term Gas Outlook, next published in May. The biannual report includes detailed forecasts and analysis of the long-term trends affecting natural gas supply and demand.