Among US states, California has often led the way in environmental initiatives. While the merit, implementation, or success of those initiatives is up for debate, there is no doubt that the Low Carbon Fuel Standard (LCFS) regulation spurred additional investment into producing fuels with lower Carbon Intensity (CI) scores throughout the US. From nationwide investment into biofuels and renewable fuels to being cited as a financial driver in the investment decision for recent Direct Air Capture (DAC) projects, LCFS credits (the market aspect of the program) have traded at their peak for just above $200/MT CO2, a much higher price than the 45Q carbon sequestration tax credit, which BTU Analytics recently discussed. Today’s Energy Market Insight will dive into what the credit is, where the price has been, and the potential implications it may have on existing and future investments.

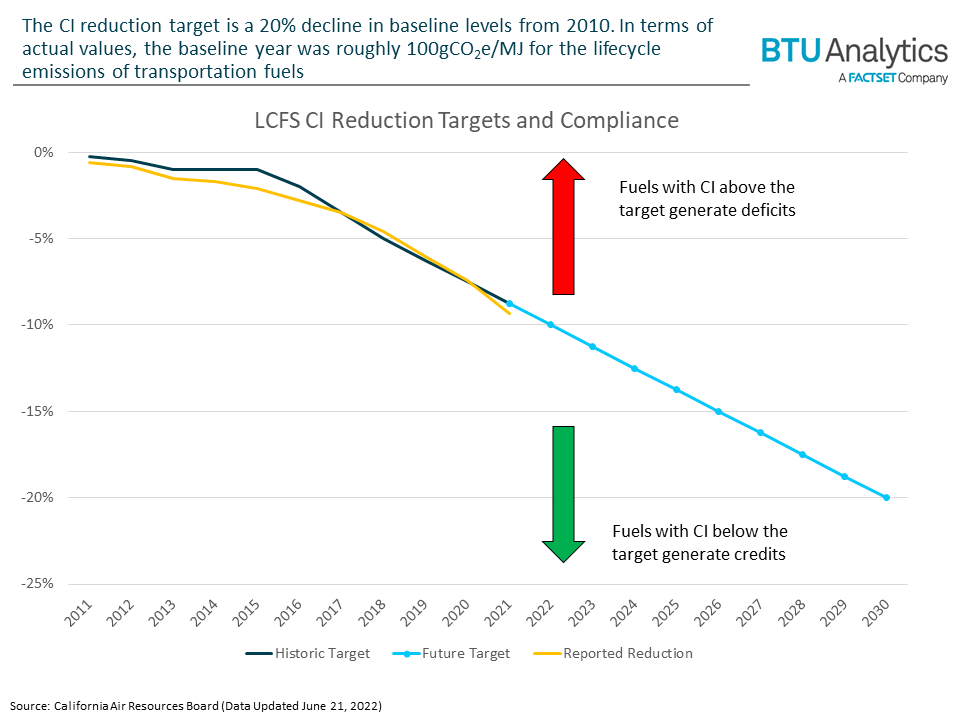

The goal of the LCFS program is to reduce the CI of the transportation fuel mix by 20% from the baseline year of 2010. The mechanism to achieve this outcome is by setting annual CI standards, which are calculated as lifecycle carbon emissions of the fuel. Producers of transportation fuels must meet these CI standards for the product to be consumed in California. If a fuel is produced in a way in which its CI score is higher than the current target value, that producer generates a deficit. Conversely, a credit is generated when a fuel has a CI score lower than the target value. Regulated parties then match their credits with their deficits at the end of each year, and parties with deficits must buy credits in order to meet this requirement.

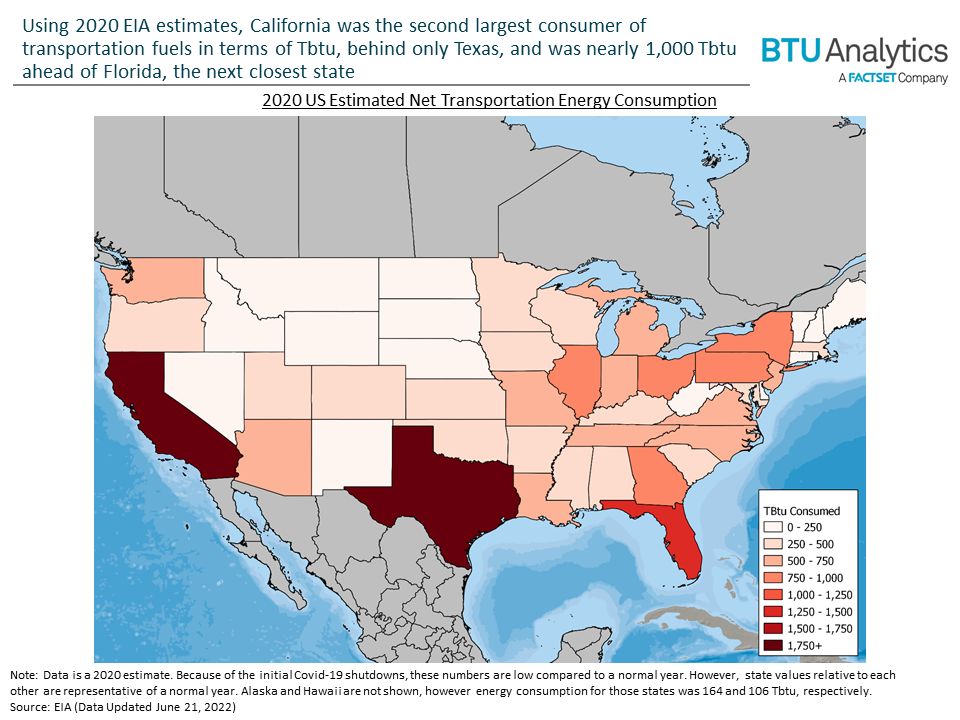

While this only applies to fuels consumed in California, the production of that fuel could occur in other states. This means that a refiner in Texas that sells into the California market would be subject to these regulations. This matters because California is the second largest consumer of transportation fuels in the country (2,352 TBtu consumed in 2020), second only to Texas (2,839 TBtu consumed in 2020). Both states consume far more energy than any other state, with California representing around 10% of all transportation fuels consumed in the US in 2020 by EIA estimates. While 2020 was highly irregular due to COVID-driven lockdowns, California’s share relative to the US is representative of a typical year.

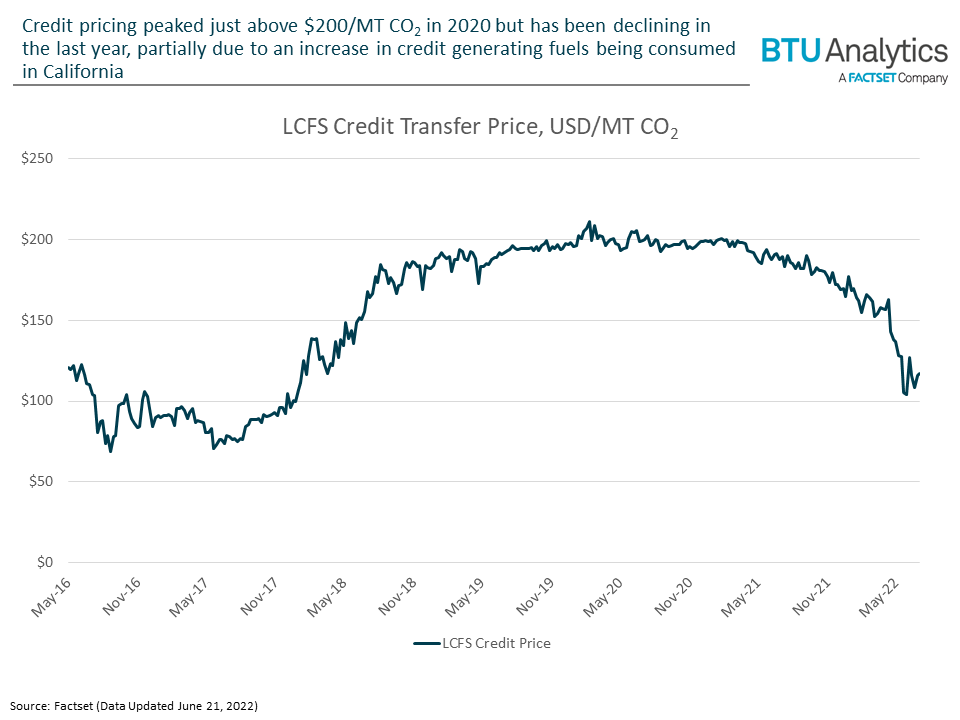

With an understanding of what the credit is, and how big the transportation fuels market is in California, we can look at what has been happening with the price of the credit itself. The program was initially introduced in 2009 but went through some changes until it finally landed in its current form at the beginning of 2016. As such, prices of the credit are often shown back to mid-2016.

As prices climbed to $200/MT CO2, even currently uneconomic projects, like DAC, can become financially attractive, particularly when this credit is stacked on to the 45Q credit and any other voluntary carbon markets. A DAC project uses technology to pull CO2 from the air which can then be used in EOR or sequestered underground. Regardless of how the CO2 is used, the project becomes eligible for the 45Q tax credit, in addition to generating an LCFS credit which can then be sold, even if the project is not located in California. This was part of the rationale for 1PointFive’s (a subsidiary of Occidental Petroleum, NYSE: OXY) DAC project that was announced to be constructed in Texas. This project has an annual capacity of 1MMT and is slated to come online in 2024.

However, prices have recently started to decline, and while there are many factors playing into this, one component is that some of the fuels, such as biodiesel and renewable diesel, not only generate credits but also displace traditional diesel from the market because they burn equivalently. In this instance, one replaces a deficit generator (diesel) with a credit generator (biodiesel), meaning there are more credits and less deficits, leading to a decrease in the price of a credit due to lower demand for those credits. Lower prices have implications for investments that rely on high credit prices in order to make economic sense.

As the global energy transition begins to take shape, regulatory structures like the LCFS are going to be increasingly important to pay attention to because they will create new investment opportunities as well as potential costs for many fossil-fuel driven industries. For additional coverage of related topics, be sure to sign up for the BTU Analytics blog.