Since 2010, the chemical manufacturing industry has been among the fastest growing sources of US energy demand. Chemical manufacturing is a broad category, including everything from plastics to fertilizer to pharmaceuticals. The industry has a meaningful US presence, although facilities span the globe, with a heavy concentration also found in China. Overall, chemical manufacturing is highly energy and carbon intensive, and many processes require hydrocarbons as feedstocks. Without including the production of fluorinated gases, BTU estimates from EPA and EIA data that chemical facilities in the US released nearly 280 MMt of scope I CO2e in 2018. Chemical producers have responded to mounting ESG pressure with plans to aggressively reduce or eliminate these emissions. The effect will likely have an outsized impact on demand for natural gas and NGLS; though only making up 4.2% of US emissions, the chemicals industry consumed 9.7% of US natural gas in 2018.

This Energy Market Insight examines the growth of energy use in chemical manufacturing and the end-use source of the emissions within the chemical manufacturing process. Note that today’s insight is an excerpt of a longer analysis on the potential impact of ESG goals on chemical sector energy demand, to be published in the Upstream Outlook report later this month.

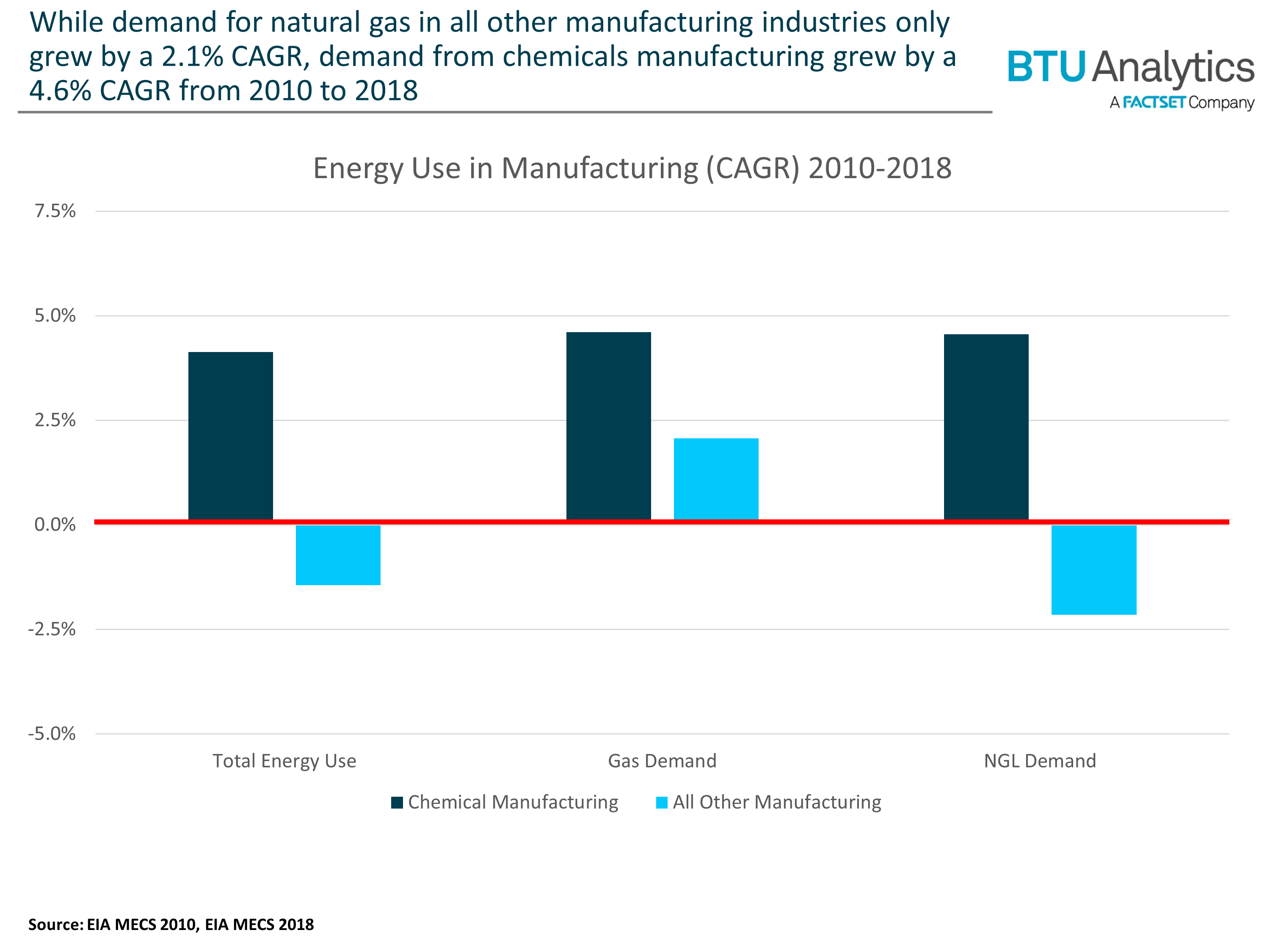

In the last 15 years, inexpensive natural gas and NGLs have made the US a highly competitive location for manufacturing chemicals, particularly chemicals involved in the production of plastics and materials. Total energy consumed by chemical manufacturing grew by 38% in the period from 2010 to 2018, while total energy consumption from all other manufacturing industries shrunk by 11%. The growth in natural gas demand was especially acute. Chemical manufacturing’s demand for natural gas grew by 2.7 Bcf/d from 2010 to 2018, representing a 61% share of all industrial demand growth. As of the EIA’s most recent Manufacturing Energy Consumption Survey (MECS) in 2018, the chemicals industry made up 38% of all industrial gas demand at 8.9 Bcf/d. Additionally, the industry consumed 2.4 MMb/d of NGLs, primarily ethane used as feedstock.

Despite this past trajectory, chemical manufacturing’s demand for energy commodities may be impacted by emerging ESG commitments. Firms promising net-zero emissions by 2050 represent a significant portion of the US chemical sector. Plants owned by companies with net-zero commitments made up more than 46% of greenhouse gas emissions for chemical plants reporting to the EPA in 2020. If these companies were to achieve their net-zero goals, the chemical industry’s demand for energy could shift materially.

Achieving net-zero would require action across multiple strategies, as emissions come from multiple processes. Based on company disclosures, four strategies emerge as pathways toward net-zero chemicals manufacturing:

- Efficiency improvements

- Electrification

- Carbon capture

- Feedstock replacement

Improvements to efficiency and carbon intensity are already underway through means such as reducing the use of coal, recovering waste heat, and switching from steam boilers to steam/power cogeneration. This has allowed some producers to reduce carbon intensity per ton of product. However, to achieve absolute emissions reductions, each of the other three pathways will likely have to be implemented to some degree, and each will have important implications for energy demand.

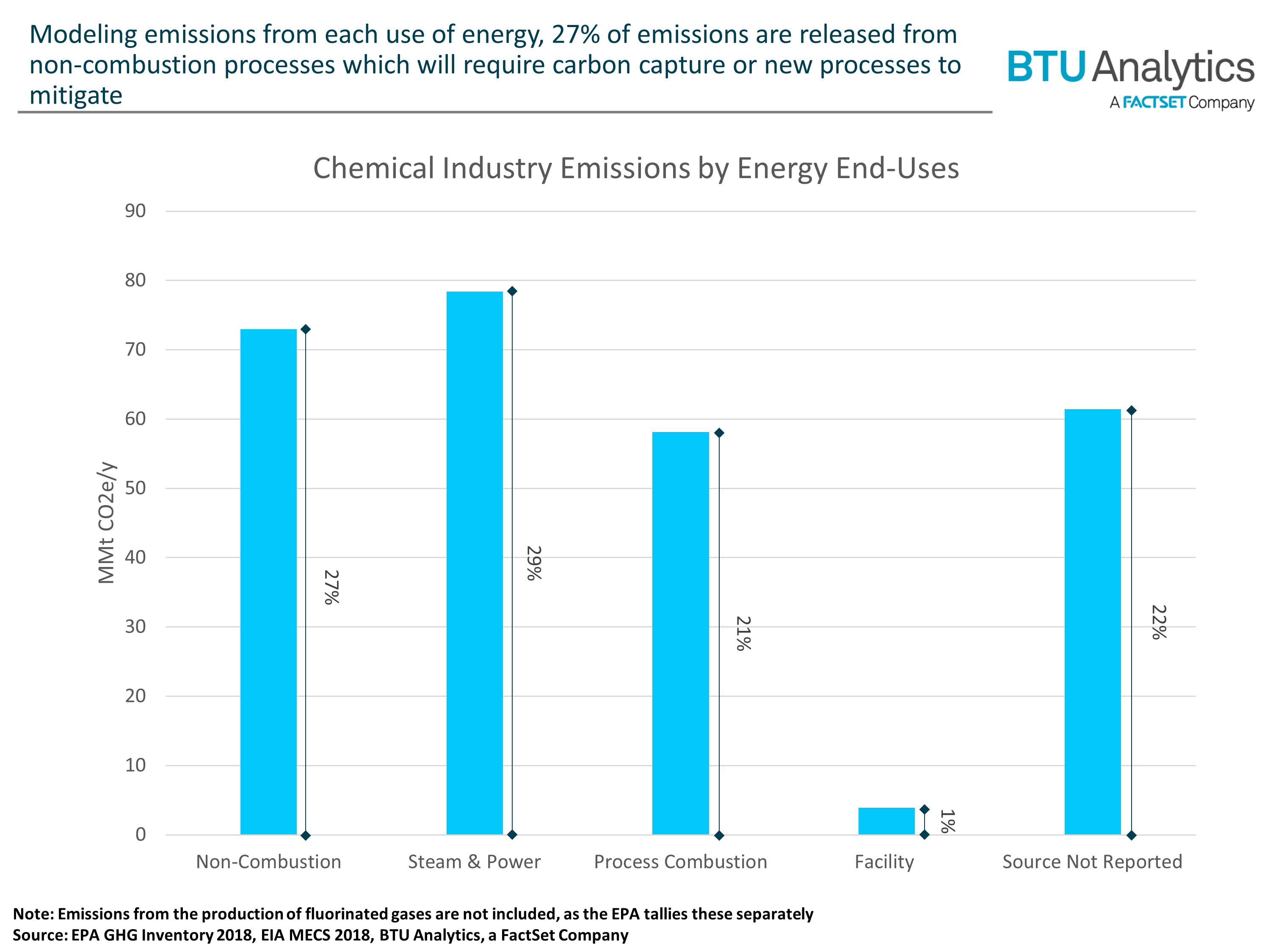

Carbon capture, in various forms, could allow the use of fossil fuels to continue in applications that are difficult to electrify. Additionally, carbon capture could help address the roughly 27% of emissions that are released directly from chemical reactions in manufacturing processes. Ineos, ExxonMobil, Air Products, Eastman, and Celanese are among major firms to list carbon capture highly among their sustainability strategies. Posing a challenge for carbon capture is that currently available technology is itself highly energy intensive and costly. The Global CCS Institute estimates most chemical industry applications would cost between $50 and $90 per ton. Factored by BTU’s estimate for the industry’s 2018 scope I emissions, this would suggest an annual expense between $14 B and $25 B to capture all emissions, or roughly 2 to 3% of the US chemical industry’s gross annual revenue. Applications are likely to be much easier in certain cases where the concentration and pressure of CO2 is much higher in flue gases, such as fertilizer and hydrogen production. The direct effect of carbon capture on energy markets would depend on the specifics of its deployment, but the indirect effects would support a stronger outlook for natural gas as it could continue to be used with less impact on producers’ scope I emissions goals.

The full effect of net-zero commitments will remain unclear until new emissions reducing strategies begin to be more widely implemented. However, the potential downsides for US gas and NGL markets are meaningful. Previously a source of demand growth, successful implementation of net-zero strategies may reverse that trend in coming decades. For the full copy of this analysis, including discussion of the potential for electrification and feedstock replacement, request more information on BTU Analytics’ Upstream Outlook.