The EPA estimates that the emissions from airplanes used in commercial aviation and large business jets account for 10% of all U.S. transportation greenhouse gas (GHG) emissions and 3% of total U.S. GHG emissions. Lowering aviation GHG emissions through electrification has proven difficult since current battery technology is not capable of powering long-haul flights. Alternative fuels with lower emissions, such as green hydrogen, are also still in their infancy in terms of production and implementation in aircraft engines. Therefore, the U.S. government and major airlines have turned to Sustainable Aviation Fuel (SAF), a low-to-negative carbon intensity fuel that is nearly identical to traditional jet fuel in terms of its chemical makeup and physical characteristics. In this Energy Market Insight, we will look at the current status of SAF production in the U.S. and discuss various factors that may impact future SAF projects.

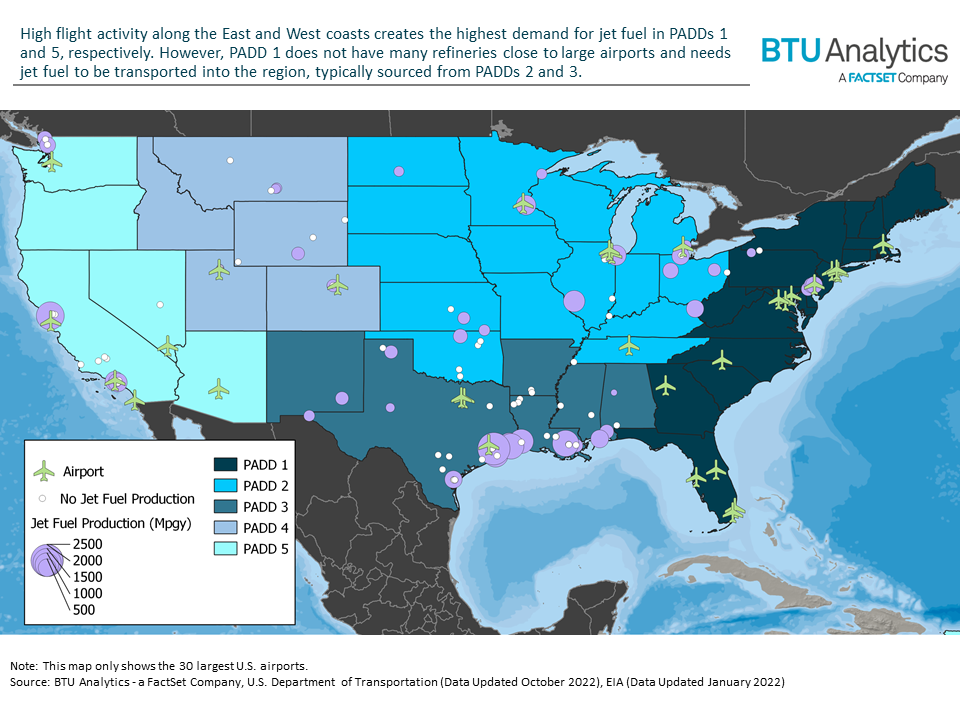

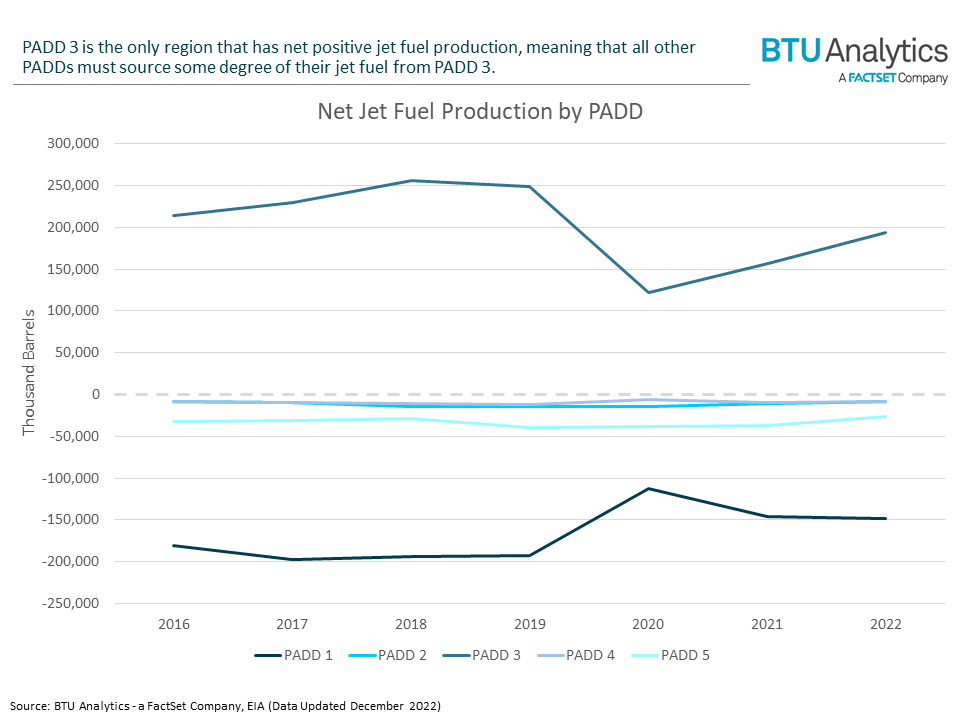

The vast majority of jet fuel in the U.S. is currently produced from crude oil at refineries. The U.S. is divided into five Petroleum Administration for Defense Districts (PADDs) and the ratio of jet fuel production to consumption varies within each PADD. Most PADDs consume more jet fuel than they can produce, such as PADD 5 on the East Coast, which typically produces less than 16% of its own jet fuel. However, PADD 3 is the one exception, producing over 60% of U.S. jet fuel at refineries along the Gulf Coast and consuming less than a third of its own production capacity. Therefore, jet fuel is mainly transported out of PADD 3 to accommodate other PADDs with higher flight activity.

SAF is a biofuel that can be made using a variety of different feedstocks, including used cooking oils, fats and greases, municipal solid waste, woody biomass, and dedicated energy crops. SAF has a lower carbon intensity than traditional petroleum-based jet fuel, with some production pathways even resulting in net-negative carbon intensities. Therefore, SAF is viewed as an important near-term solution for lowering the life cycle GHG emissions of the aviation sector.

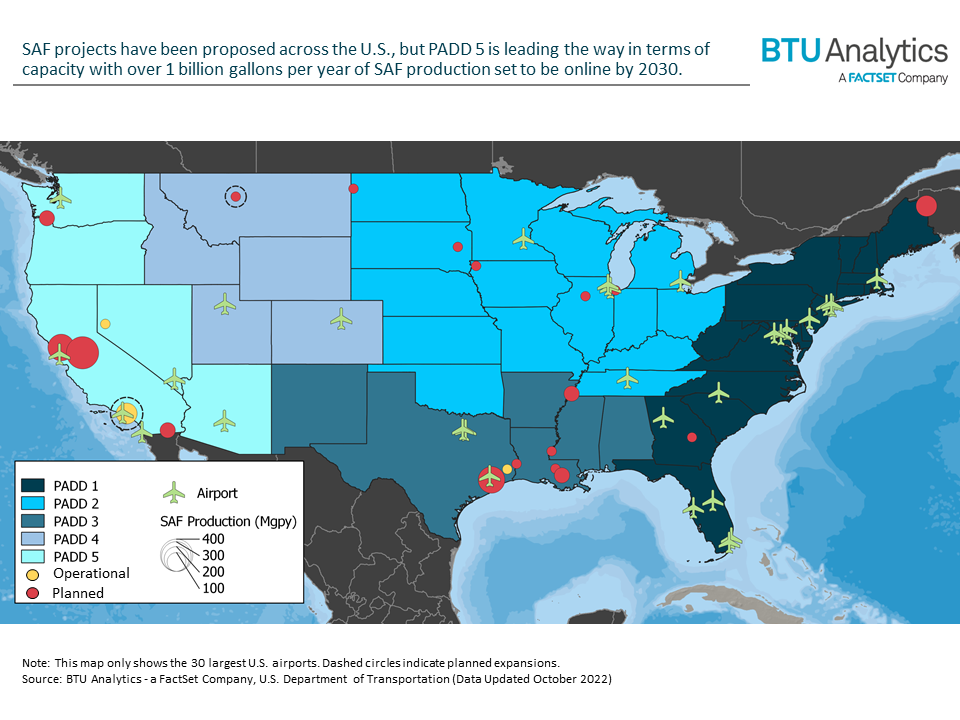

In September 2021, the Biden administration announced the Sustainable Aviation Fuel Grand Challenge, which aims to increase SAF production in the U.S. to 3 billion and 35 billion gallons per year by 2030 and 2050, respectively. With the U.S. having produced between 21 and 26 billion gallons of jet fuel per year over the past five years, this 2050 SAF goal would account for the entire current jet fuel market. While there are only a few facilities currently producing SAF in the U.S., there are nearly 20 new SAF projects that are set to be operational by 2030. Together, these facilities have already secured long-term offtake agreements with various airline companies for a total of over 7.2 billion gallons of SAF. However, BTU Analytics estimates that all of these facilities combined would only be able to produce around 2.1 billion gallons of SAF per year by 2030, falling short of the government’s 3-billion-gallon goal.

U.S. SAF production will need to ramp up in the coming years and decades in order to meet government goals and rising demand from the aviation industry. Higher production could be achieved in various ways, including the expansion of current operations, conversion of existing refineries to produce SAF, or the buildout of new SAF facilities. Unlike petroleum refineries, which are clustered near oil resources, SAF project locations can be flexible since they can utilize a variety of feedstocks that are readily available across the country, such as municipal solid waste or woody biomass. With more U.S. SAF projects likely to be announced in the future, BTU Analytics anticipates that jet fuel production will become less concentrated along the Gulf Coast since SAF facilities take advantage of diverse feedstocks that exist throughout the country.

To see more analysis and insights from BTU Analytics about the Energy Transition, and to be the first to see new BTU products on the Energy Transition, email info@btuanalytics.com with the subject line “Energy Transition”.