Little is known about how the large-scale development of low-carbon hydrogen would ultimately affect traditional energy commodities, like natural gas. Different forms of hydrogen could either displace or increase demand for natural gas. But as many proposed projects aim to export their products and others are focused on producing transportation fuel, these projects could meaningfully increase demand for U.S. natural gas if they enter operation. Therefore, this Energy Market Insight will take a look at the current slate of proposed and existing hydrogen projects in the U.S. and the end-markets they’re intending to serve to glean a clearer picture of how the ongoing hydrogen buildout could affect natural gas demand.

There are many modes of producing hydrogen, but three methods attract the most attention. In the U.S. today, most hydrogen is considered “gray”, meaning it is produced from natural gas without any form of carbon capture. This releases between 9 and 11 kg of CO2 per kg of hydrogen, making this form of hydrogen production very carbon intensive. If carbon capture is installed, emissions can be lowered dramatically to create “blue” hydrogen. Blue hydrogen is already being produced at commercial scale and most of the proposed hydrogen capacity currently in development falls into this category. “Green” hydrogen requires the electrolysis of water using renewable electricity, thereby producing no direct emissions.

Green hydrogen production would be expected to displace demand for traditional energy commodities, but the effect of blue hydrogen is more uncertain. Since natural gas is used in its production, the net effect would depend on how efficiently it could be produced and into which end-market it is sold. While the net effect of blue hydrogen used as utility gas might be negligible, for instance, blue hydrogen sold as transportation fuel or sold into export markets could be a net boost for U.S. gas demand.

Aside from its pure form, hydrogen is also produced as a precursor for manufacturing ammonia and methanol. Both of these related commodities could also be produced in “blue” or “green” forms, either by applying carbon capture or using electrolysis. In addition to their traditional uses, ammonia and methanol are also capable of storing or transporting hydrogen or being used as alternative fuels in themselves.

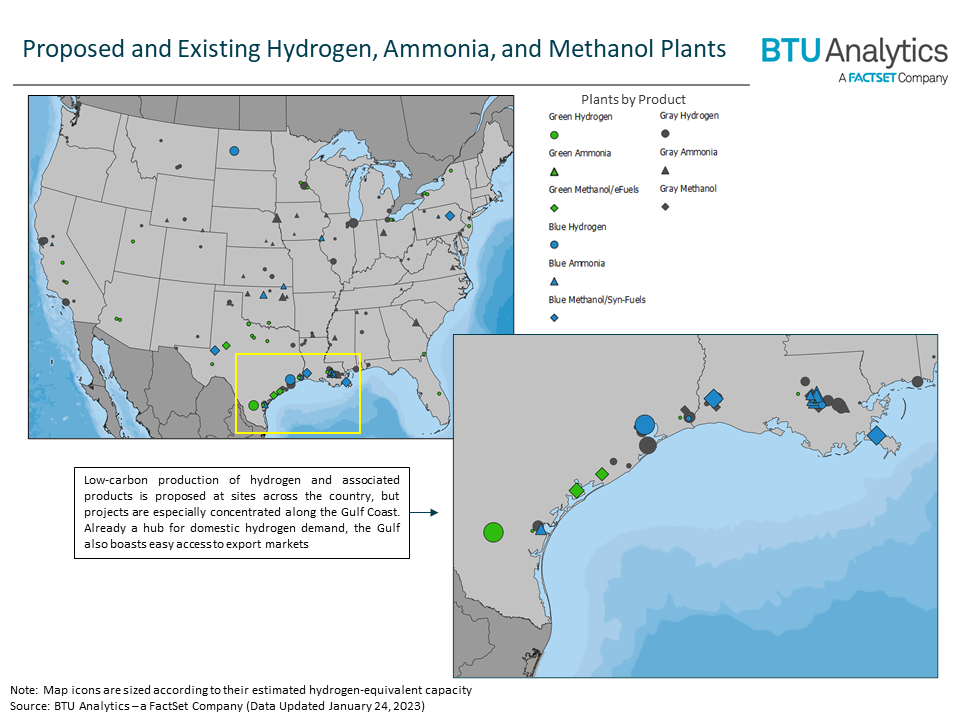

BTU Analytics is tracking 18 blue projects across all three of these commodity types, representing a total of 22,000 t/d of hydrogen capacity. Even more green projects are in development, though most are small pilot plants, with a cumulative total of 12,000 t/d of hydrogen capacity. Currently, operational plants produce just 2,000 t/d of low-carbon hydrogen in the U.S. While new projects are spread across the country, a high concentration is planned along the Gulf Coast. In fact, about 65% of planned capacity is slated for coastal Texas and Louisiana.

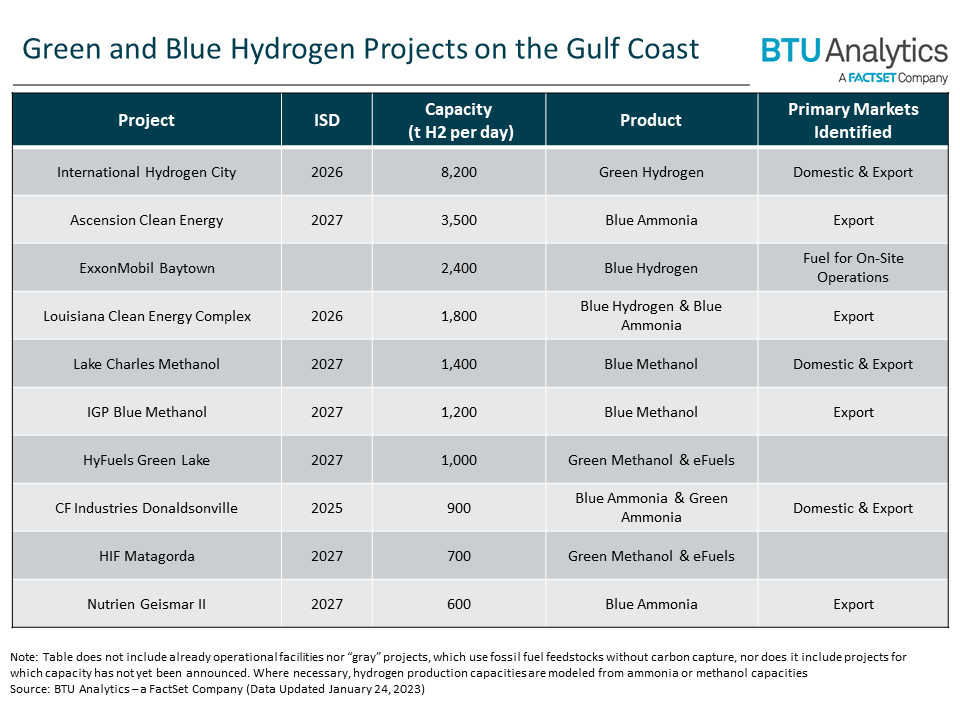

Some of these projects will supply demand at existing industrial complexes, as is the case for ExxonMobil’s hydrogen plant in Baytown, TX, but many of these projects have stated that their products will be sold into export markets or transportation fuel markets. Of the ten largest Gulf Coast hydrogen projects listed below, four are planning to produce methanol or methanol-based fuels for transportation markets. Another four are planning to produce ammonia, with most identifying export markets as the primary source of demand. This is consistent with Nutrien signing a letter of intent for Mitsubishi to buy 40% of Nutrien’s Geismar blue ammonia production for export to the Asian market, as well as CF Industries signing a memorandum of understanding with JERA to export 30% of its Donaldsonville production to Japan. CF Industries has also entered a joint venture to build a new ammonia plant in Louisiana with Japanese conglomerate Mitsui, which could similarly support export demand.

As hydrogen development focuses on export markets and transportation fuels, these new plants could create incremental demand for natural gas. BTU Analytics estimates the largest of the blue ammonia plants in development could consume an incremental 550 MMcf/d of natural gas once operational.

To see more analysis and insights from BTU Analytics about the Energy Transition, and to be the first to see new products on the Energy Transition, email info@btuanalytics.com with the subject line “Energy Transition”.