Following a slow start to winter 2017-2018 with weak winter temperatures in November and December, winter finally arrived over the last week east of the Rockies. The below-normal temperatures have caused natural gas and oil production freeze-offs in producing areas while demand in major heating markets has soared. All the while, U.S. LNG exports have remained steady and at full utilization. In this Energy Market Commentary, we will look at extreme winter temperature impacts on supply, demand, and LNG exports.

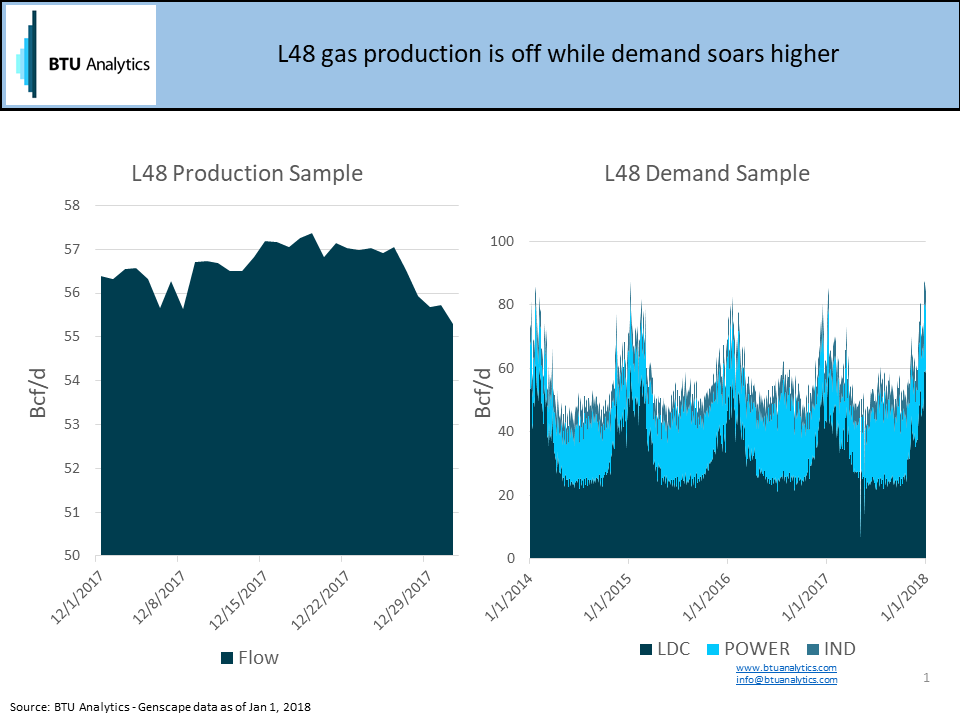

Over the last five days, the natural gas production sample, based on interstate natural gas pipeline nominations, shed about 1.5 Bcf/d as sub-freezing temperatures rolled through the southern producing areas of the Permian, Oklahoma, Barnett, Fayetteville and Haynesville. Meanwhile, frigid temperatures across the major natural gas heating markets of the Midwest, Mid-Atlantic, Northeast and New England have driven demand to peak levels as shown below.

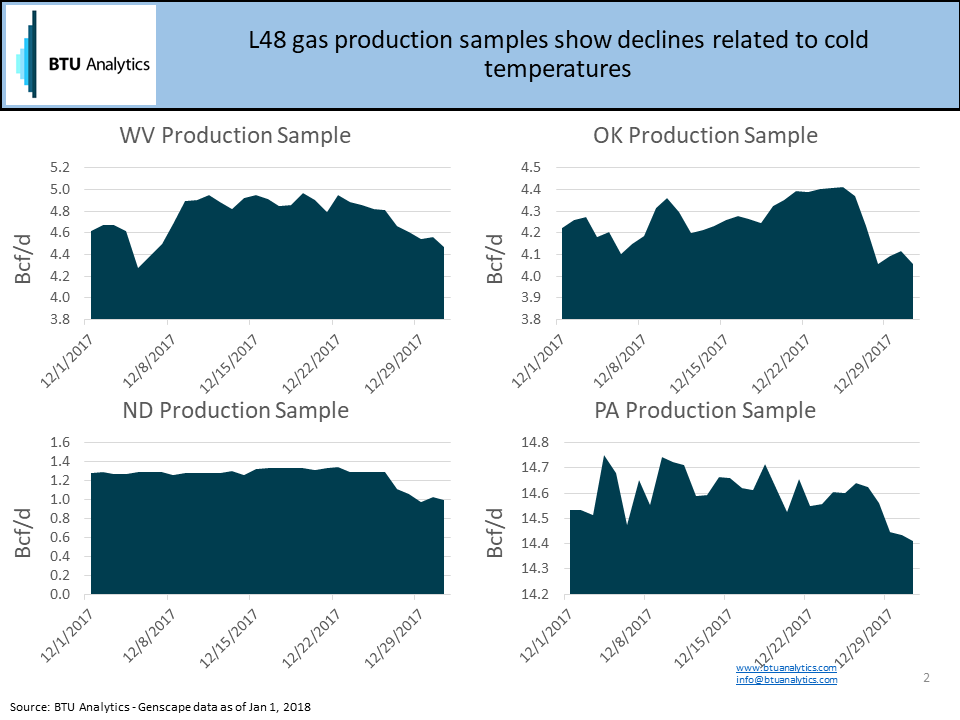

Based on the production samples in the producing area, the areas hardest hit by freeze-offs on a volume basis are West Virginia, Oklahoma, North Dakota and Pennsylvania representing about 1.0 Bcf/d of declines over the last several days as shown below. However, it is worth noting that some of the Oklahoma volumes may not be showing up on interstate pipelines due to gas being diverted to serve local heating markets in Oklahoma. Despite that, the extreme cold and cash price volatility experienced going into the weekend indicates some volumes were likely shut-in due to the cold. The decline in natural gas volumes in North Dakota are also likely an indication of crude oil volumes being shut-in as well since the vast majority of North Dakota natural gas production comes from the Bakken and ties into the interstate network. The pipeline data would suggest that nearly 200 Mb/d of crude oil production may have been shut-in this weekend and 150 MB/d of production shut-in on average over the last week.

Of course, this cold snap has hit across a three-day weekend and the first of the month which due to balancing introduces some variance in the pipeline nomination data. Shut-in volumes in this piece are not inclusive of January 2, 2018 pipeline nominations and based on weather forecasts, more pronounced shut-ins can be expected.

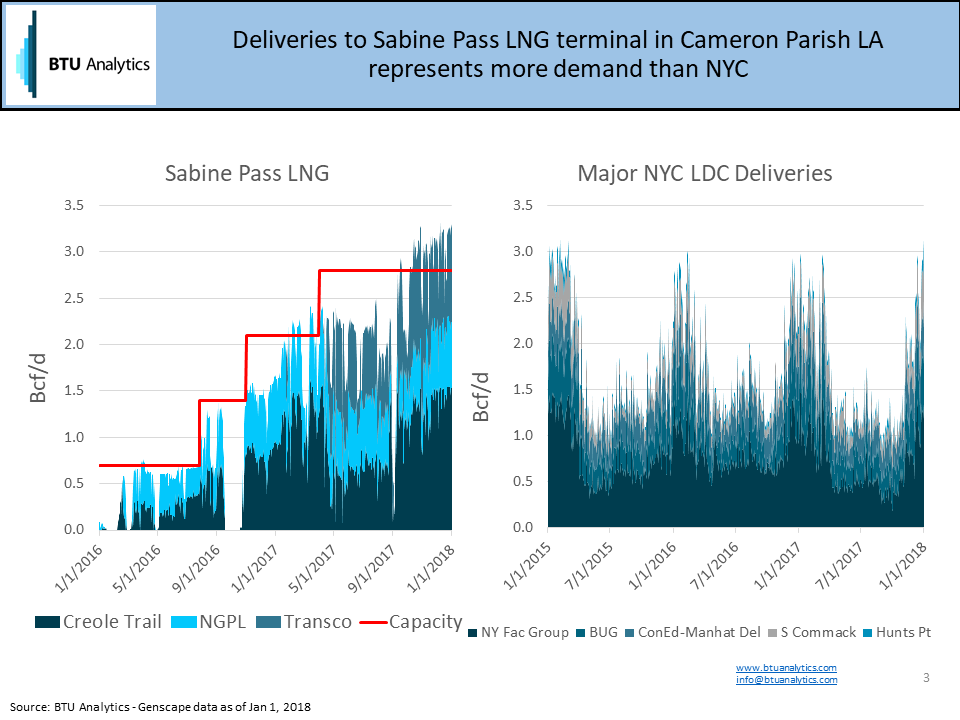

Flipping back to natural gas, as this is the first winter with several trains running at Sabine Pass, it has been impressive to see how steady pipeline nominations to the terminal have been at approximately 3.2 Bcf/d despite the record cold temperatures across the US. The other notable takeaway is Sabine Pass with four trains running is more than the equivalent of deliveries to the major New York City utility meters at peak winter levels at over 3.0 Bcf/d as shown below. An impressive new piece of demand, considering BTU Analytics has covered the declining impact of natural gas res/com demand in previous Energy Market Commentary posts.

To learn more about soaring winter demand see BTU Analytics’ Henry Hub Outlook, to learn more about winter production freeze-offs see BTU Analytics Upstream Outlook, and finally,to learn about how the North American natural gas market will balance going forward, come to BTU Analytics’ What Lies Ahead 2018 conference in Houston on February 22, 2018.