After peaking in late 2012, production in the Fayetteville has been in steady decline and thus tends not to receive as much attention compared to more active regions. However, recent large shakeups to ownership in the Fayetteville makes revisiting the current trajectory of the region appropriate. There has traditionally been three main Fayetteville operators: Southwestern Energy, BHP Billiton, and ExxonMobil. Recently, two of these main players have exited the region. In September, Southwestern Energy, the pioneer and most active producer in the Fayetteville announced it sold its position in the region to privately backed Flywheel Energy, LLC in a $1.865 billion deal that is expected to close in December. BHP Billiton also recently completed the sale of its Fayetteville assets at the end of September to a subsidiary of Merit Energy Company, another private company, as part of its overall divestiture from US shale. Given the relatively close proximity of the Fayetteville to growing natural gas demand along the Gulf Coast, there is opportunity for this legacy shale play as new players enter the region.

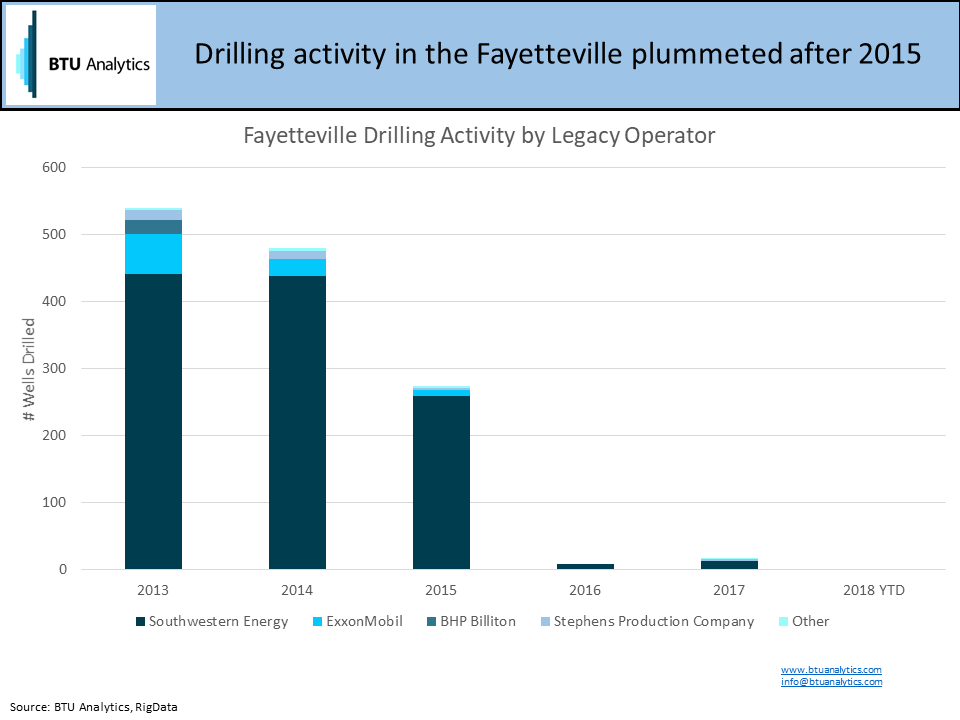

Drilling activity in the Fayetteville has been nearly nonexistent since 2016, falling from 541 wells drilled in 2013 to less than 20 in 2017. Historically, Southwestern Energy was the main operator, as seen in the figure below. Additionally, BHP had not been active in the region since 2013.

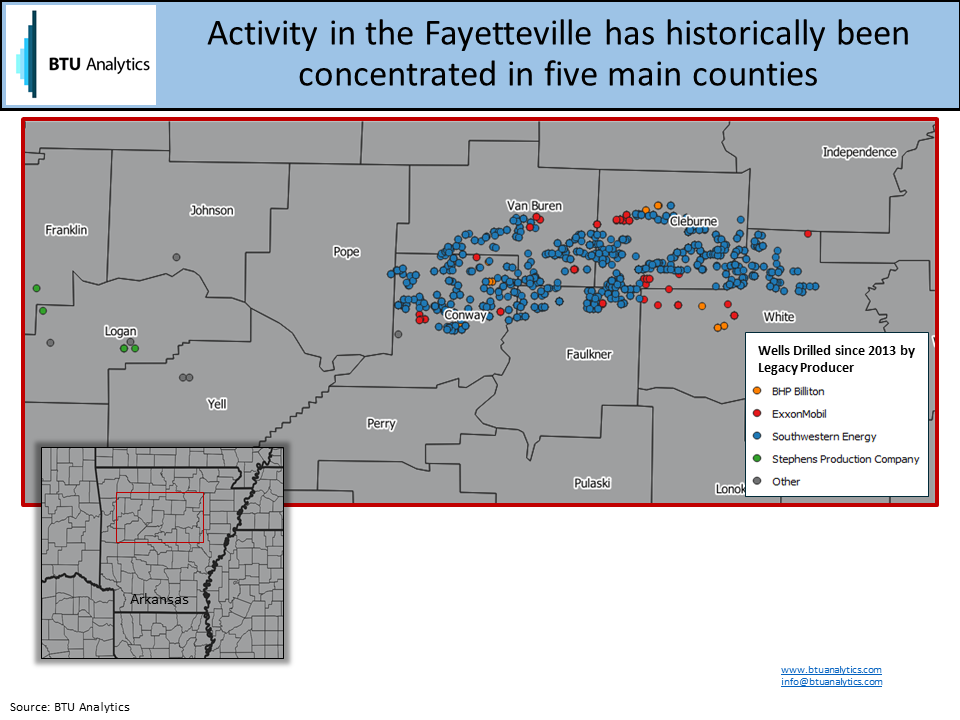

Activity in the Fayetteville has been focused in five main counties in Arkansas, with Southwestern Energy’s activity widely spread across these counties, as seen below. Recently, Southwestern had emphasized in investor materials their efforts at redeveloping legacy areas, including three redevelopment wells in Conway county, claiming 25% to 50% resource recovery improvement.

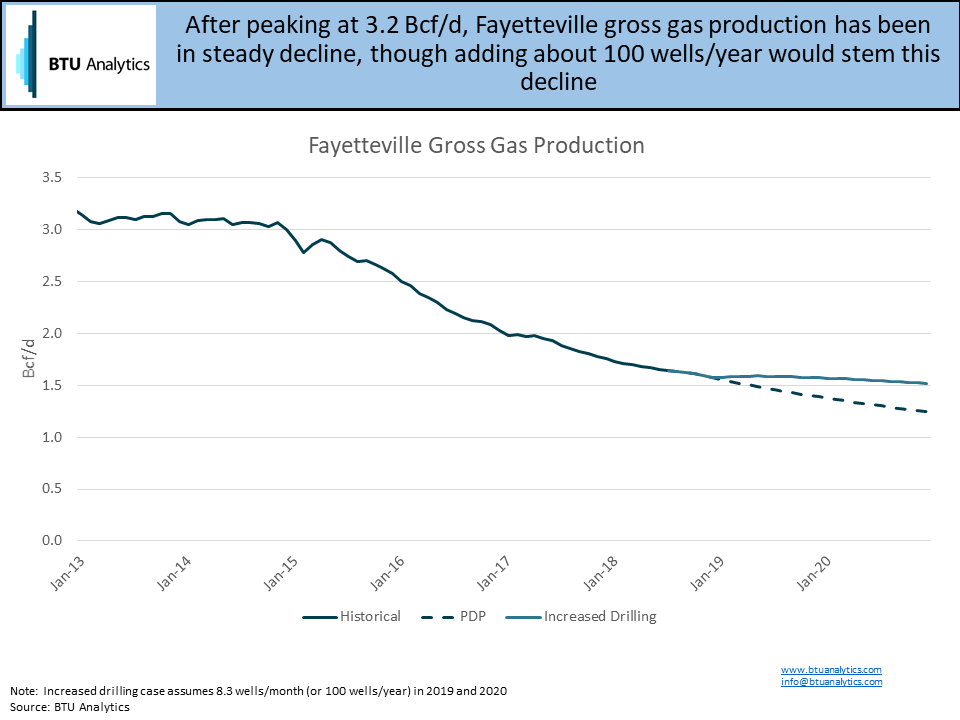

As drilling activity has all but stopped, production has fallen to half of its peak of 3.2 Bcf/d reached in late 2012/early 2013, to currently about 1.5 Bcf/d, essentially following PDP decline, as seen in the figure below. Over the near term, we have expected to see continued production declines in the region and minimal drilling activity, as Fayetteville loses out to more economic Marcellus, Utica, and Haynesville gas plays. This was particularly the case when Southwestern Energy was still in the Fayetteville and utilized cash flow from the Fayetteville to fund its development of Appalachian acreage.

However, new ownership could breathe new life into the Fayetteville, as any increase in activity by these new Fayetteville operators could stem declines. About 100 wells drilled per year would be enough to keep production flat in the region, which would roughly equate to two rigs running, assuming a rig efficiency of just over 4 wells/rig/month; this is in line with the average rig efficiency seen in 2015 when there was higher activity in the region.

How will the Fayetteville evolve with new operators, and how will it stack up compared to other gas plays? To keep up to date with activity and production in the Fayetteville and across the US, check out the Upstream Outlook, and for the relative economics of the Fayetteville, see the upcoming edition of the E&P Positioning Report.