At times, we’re all guilty of it. We simplify the complex business of producing oil and gas down to a gratifyingly basic premise—the quality of the rock will define what resource gets developed, and whatever company has captured that resource will be the winner. While it is a commodity (read: price taking) business, some upstream companies have strategically ventured further into the value chain to differentiate themselves from their peers. Today’s commentary will shine a light on the cost of one of these strategies. Specifically, the analysis will examine the long-term contractual obligations of Appalachian producers, and what lessons producers in other capacity constrained basins might learn from it.

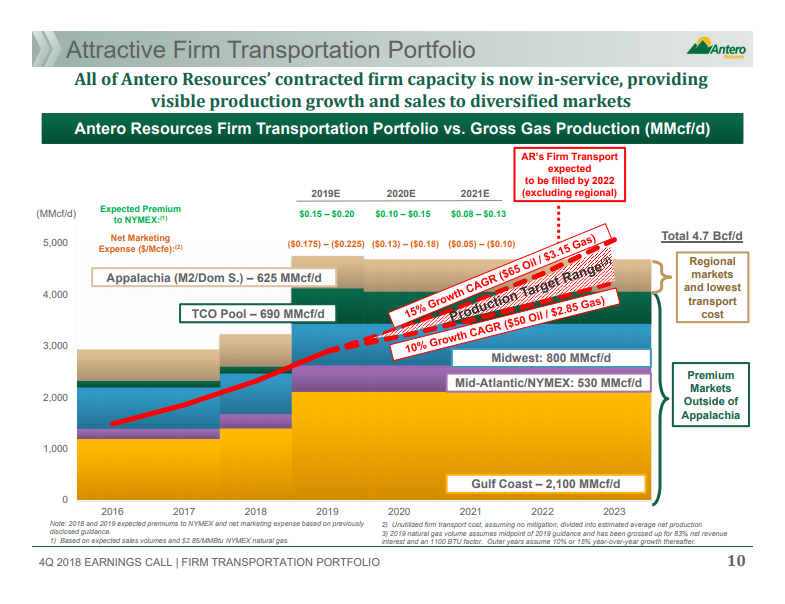

On the Q4 earnings call for Antero Resources (NYSE: AR), the company hit many of the same notes other public E&P companies highlighted during the quarter including drilling and completion efficiencies and a disciplined drilling plan that could allow for growth while returning capital to shareholders and deleveraging. But when it came time for the question and answer portion of the call, the first question on the call was not on operations, but on trying to understand the costs associated with the company’s substantial portfolio of firm transportation, which the company highlighted in one of the slides that were posted for the call (shown below).

Taking a step back for a moment, let’s discuss the role of midstream and marketing in the oil and gas value chain. The price a producer receives for their oil and gas is determined by where the commodity is sold. Midstream and marketing fulfill the integral step of making sure the produced molecules move physically towards eventual end users. Some E&P companies stay out of the midstream and marketing functions completely, paying fees for another party for gathering and processing before selling to a marketer who will move that supply downstream. Other companies, such as Antero, have taken a much more active role in midstream and marketing in hopes of retaining control and capturing more value. Today’s commentary will focus on the risk/rewards that can come with marketing, and we will leave the discussion of the opportunities and risks that come with a producer actively developing and owning their own midstream assets for another time.

Antero, like many Appalachian producers, has a marketing segment tasked with optimizing the value of the company’s natural gas and liquids production. As part of that strategy, the company elected to subscribe to firm capacity on long-haul pipes out of the region. That firm transportation capacity has come into focus more recently, as the way the market thinks about firm transportation capacity has shifted through time. Appalachia had been takeaway capacity constrained for the better part of a decade prior to Rover entering full service last year. During that time, firm transportation capacity was a significant asset that allowed its owners to benefit from “premium” pricing on the other side of the constraint. The cost of firm capacity was highly dependent on the route and when that capacity was acquired, with less expensive early brownfield capacity being captured first, and more extensive and expensive greenfield capacity coming later.

Over the past decade acreage holders in Appalachia have had a choice to make – whether to commit to new pipeline projects at ever higher fees to ensure that production could have access to pricing points outside of Appalachia or remain free of commitments and be tied to in-basin pricing. This idea was the subject of a paper BTU Analytics released almost four years ago – “A Firm Dilemma – Winners and Loser of the Natural Gas Pipeline Reversal Race.”

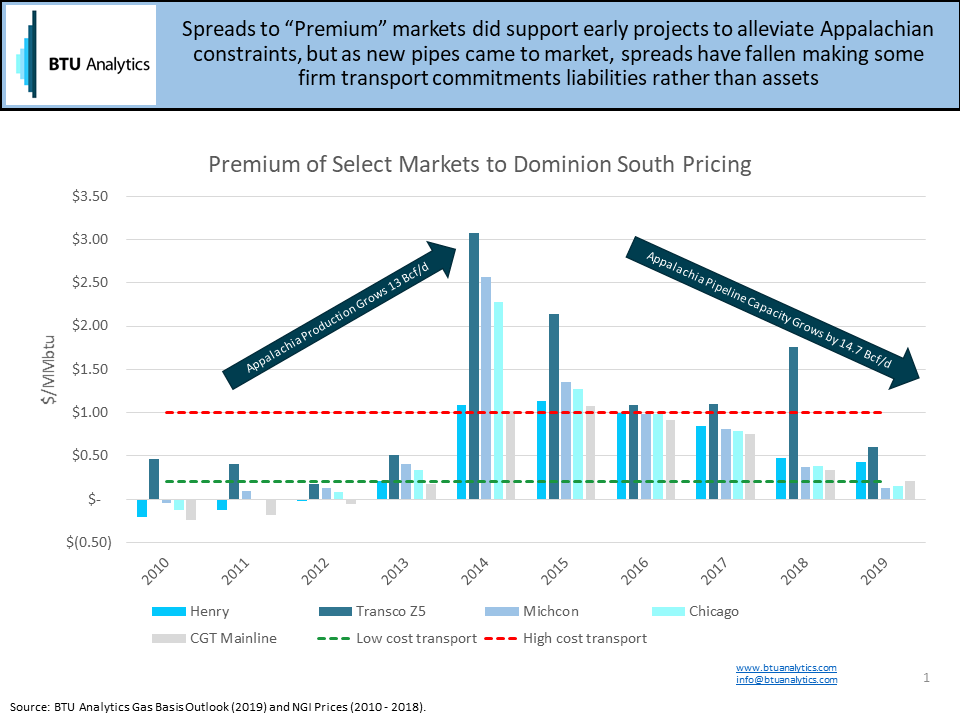

In that paper we highlighted our view – that at some point firm transportation out of Appalachia would be viewed as a liability rather than an asset, as new pipes came into service, production growth moderated, in-basin pricing moved closer to what had historically been “premium” markets. For some parties, the fees associated with the firm transportation, when netted out with the net improvement in price received, would leave those parties in potentially a worse position than parties that elected to remain free of those arrangements. We say ‘potentially’ because arguably having significant market share in Appalachia might provide other benefits and growing to have significant market share in Appalachia would not have been possible without owning some firm capacity.

The chart below shows spreads between in-basin pricing and some of the ‘premium’ markets producers now have access to with firm transport. Overlaid on the chart are two lines which approximate both the lowest cost firm transport and highest cost firm transport to these premium regions. While there have been periods of time where producers have absolutely benefited from their commitments, it is worth asking more detailed questions of producers to understand not only the cost of unused capacity, but the cost of capacity that is being utilized, and whether that capacity will handicap company performance into the future by dragging down cash flow.

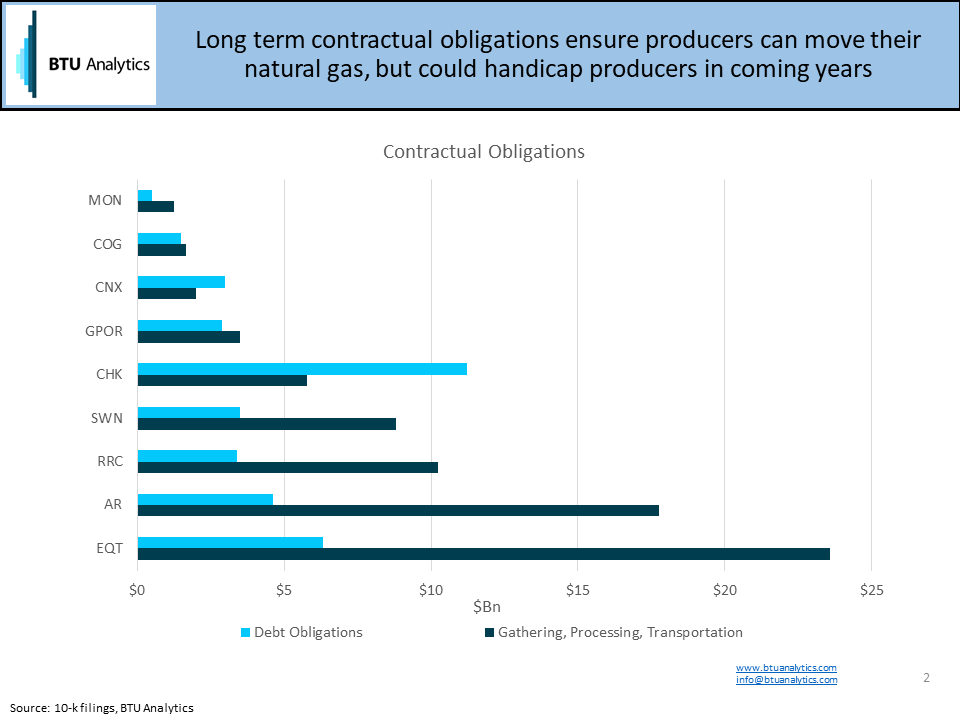

Speaking of the future, it’s high time the market pays more attention to the long-term implications of the contractual commitments producers are making and have made. The chart below highlights the debt and contractual obligations for a select group of public producers in Appalachia. These agreements, which include firm transportation commitments, add real complexity to the decision whether to drill or not to drill.

What lessons should producers in constrained markets and their investors learn from the experiences of the Appalachian producers? The first lesson is obviously that they should have been BTU clients in 2015 (kidding). The real takeaway is that the bold strategies that brought producers success in one period, might be a producer’s Achilles heel in the next. For BTU’s latest thoughts on which bold bets might go sour, request more information on our Upstream Outlook and Gas Basis Outlook services.