Back in March of 2019, Florida Power & Light (FP&L), a subsidiary of NextEra Energy, announced the largest planned battery installation in the world. The 409 MW/900 MWh battery addition will be located at Manatee County, Florida, and operational in 2021. The facility will dwarf Tesla’s existing 100 MW/129 MWh Australian facility currently holding that title. Yet in 2018, the EIA estimated just 1% of Florida’s power generation mix came from solar. Today’s energy market commentary will be part one of a two part blog. Part one will review the Florida natural gas and electricity markets. Part two will focus on the potential impacts to Florida’s natural gas demand from continued gains in solar.

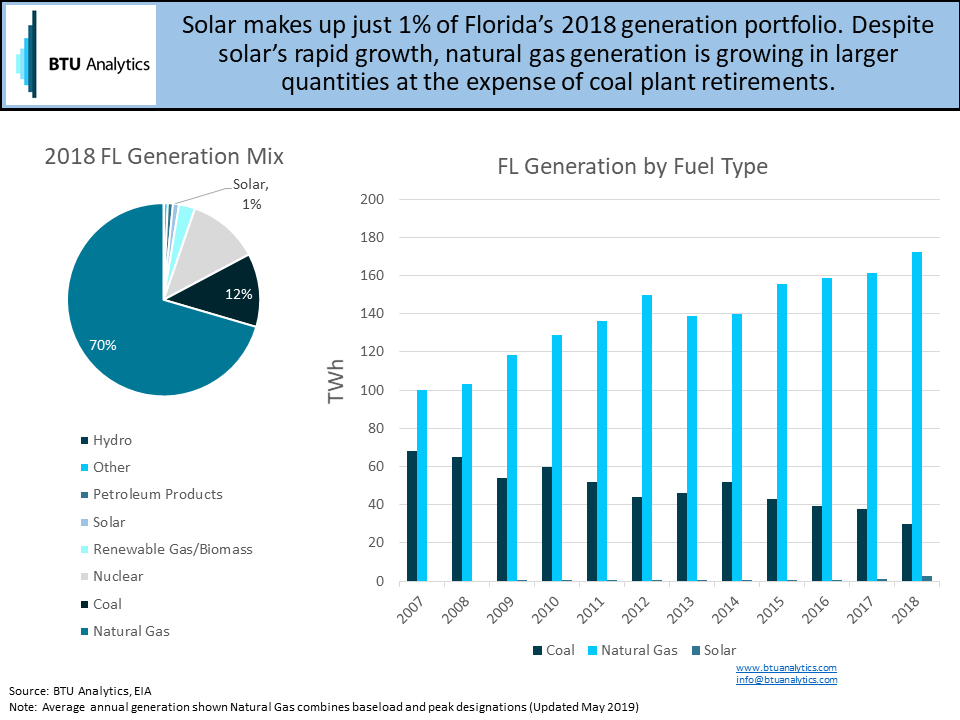

Over the last two decades, Florida’s power market focused efforts on developing efficient gas-burning facilities to replace coal-fired generation. As a result, the bulk of last year’s electricity generation in Florida came from natural gas. From 2007 to 2018, coal’s market share of fossil fuel generation declined from 40% to just 12% in 2018. The chart below on the left highlights 2018 total Florida generation. The bar chart on the right side highlights total coal and natural gas generation through time.

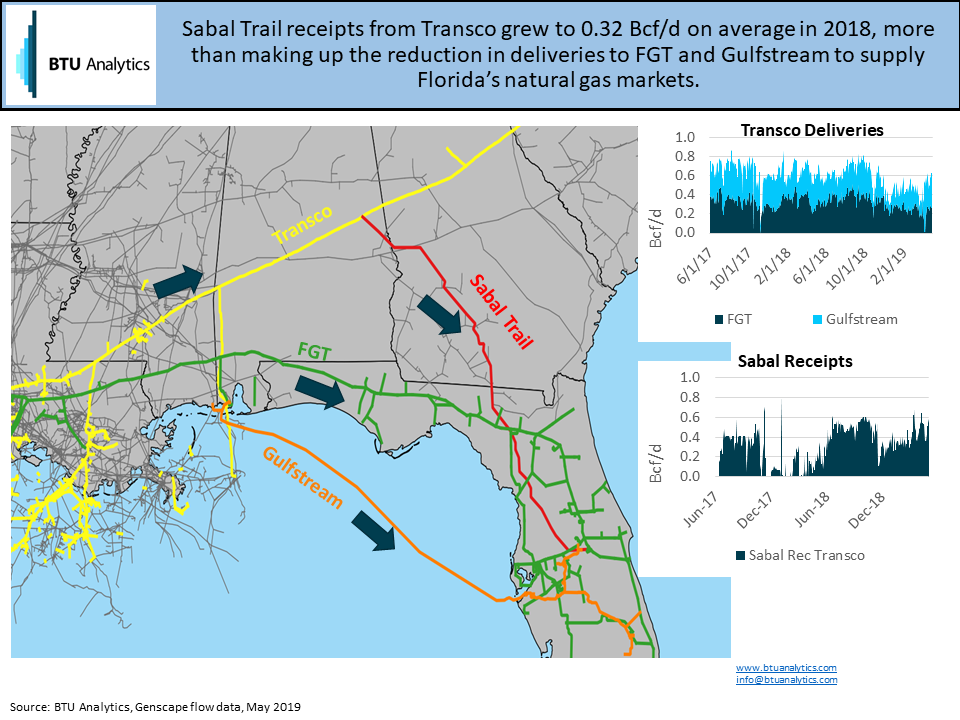

Natural gas-fired generation now accounts for 70% of total electricity generation. Coal and nuclear combine for the majority of the remaining generation with 12% each. The continued shift from coal-fired generation to natural gas generation has boosted total Florida natural gas demand and as a result, natural gas pipeline flows into the state of Florida have grown, as highlighted in the map and charts below.

The Florida natural gas market is primarily supplied by three pipelines – Florida Gas Transmission (FGT), Gulfstream, and Sabal Trail. The newest entrant of these, Sabal Trail, came online in June 2017. The terminal delivery point of Sabal Trail resides in Central Florida in close proximity to major demand markets. Sabal’s average annual receipts from Transco grew from 258 Mcf/d in 2017 to 316 Mcf/d in 2018, with respective summers not far off from those averages. The increased flows on Sabal are a far cry from its 1.0 Bcf/d of capacity into the Florida market though.

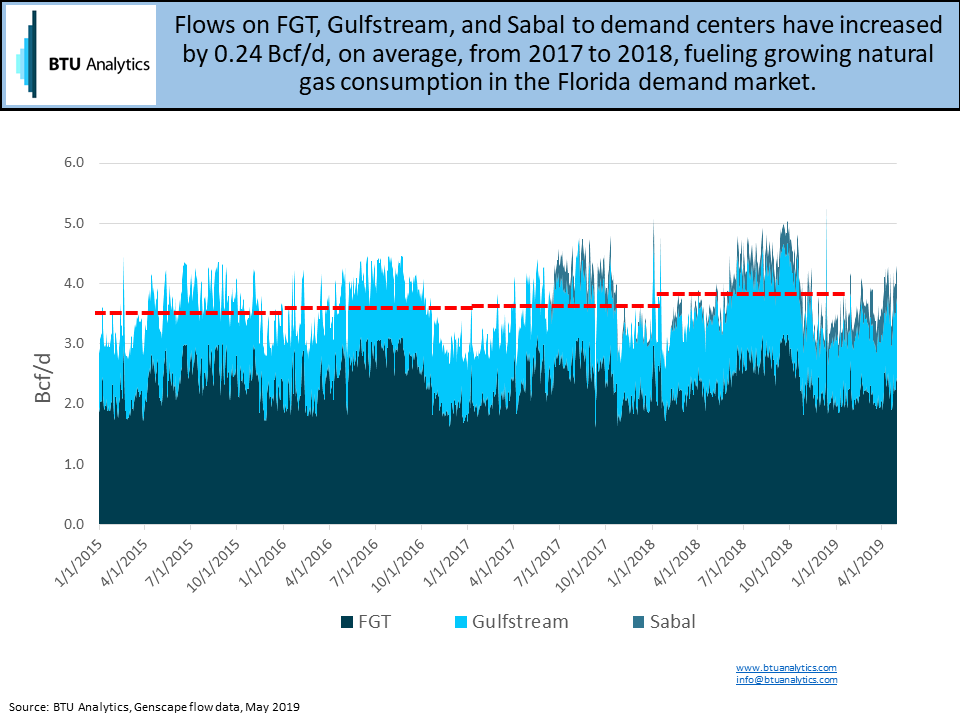

Looking at the flows of FGT, Gulfstream, and Sabal in aggregate, we can see an increase in throughput over time. The annual average in 2015 was 3.53 Bcf/d, which has grown to 3.87 Bcf/d in 2018. Most of the growth occurred in 2018 following the completion of Sabal Trail and several new gas-fired power plant projects that replaced coal-fired generation.

Over the last decade, coal has been the biggest loser in terms of fuel switching. However, looking to the future, coal doesn’t have a lot left to give to natural gas. Therefore new investments in solar and batteries will most likely come at the expense of natural gas-fired generation in the region as we’ll explore in part two of this series in the coming weeks. In the meantime, to learn more about power generation markets and supply/demand balances, request more information about BTU Analytics’ Henry Hub Outlook.