The Gulf Coast dodged a bullet with Hurricane Dorian’s northward track. However, it’s only a matter of time until the Gulf Coast is in nature’s crosshairs again. Historically, storms have created the possibility of supply disruption as offshore production was put at risk. However, as we’ve seen recently, we should readjust our expectations. Offshore production is expected to continue to decline, and thanks to growing LNG exports, the demand side of the Gulf Coast is becoming more important than ever. In the future, a Gulf Coast storm could result in a major demand interruption that could pressure gas prices to the downside.

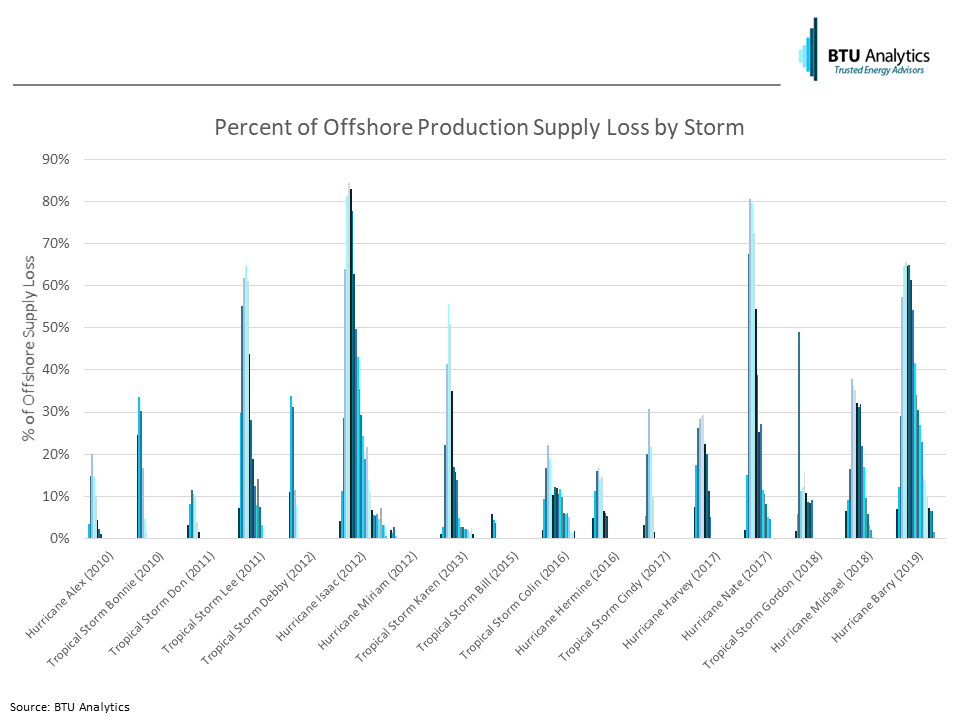

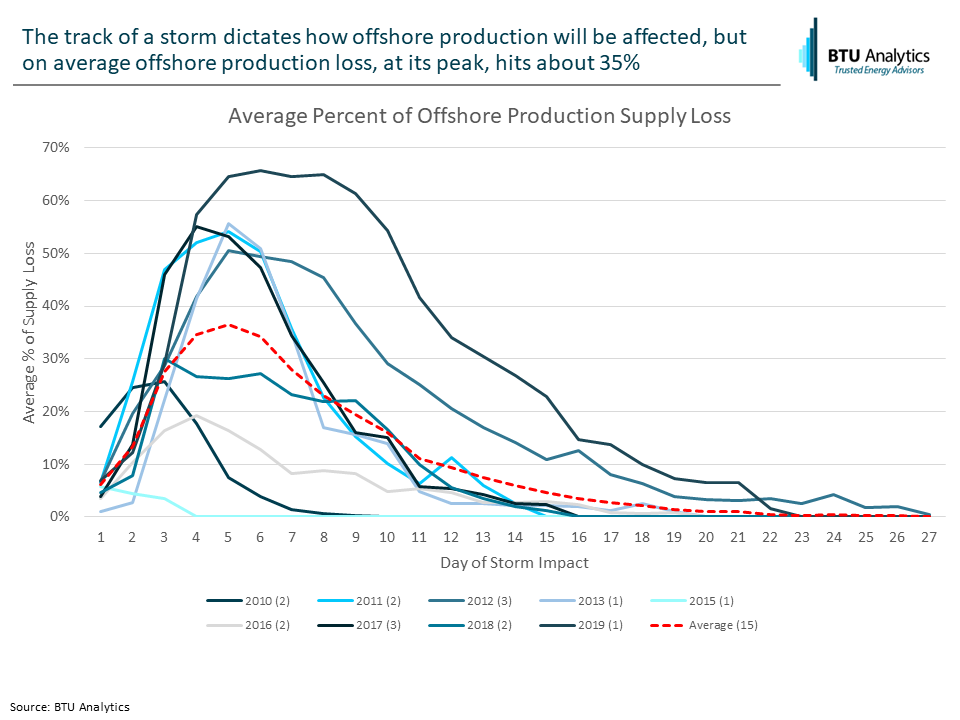

BTU Analytics looked at 15 tropical storms and hurricanes that made their way through the northern Gulf since 2010 to see what their impact was to offshore production and non-LNG Gulf Coast demand (mainly power and industrial). The graphic below shows the impact from the ‘average’ storm to offshore production. Of course, every storm is different, while the 15 storms included below impacted the Gulf Coast, each storm’s unique path brought unique consequences. For this analysis individual tracks were ignored, and all 15 storms were treated equally.

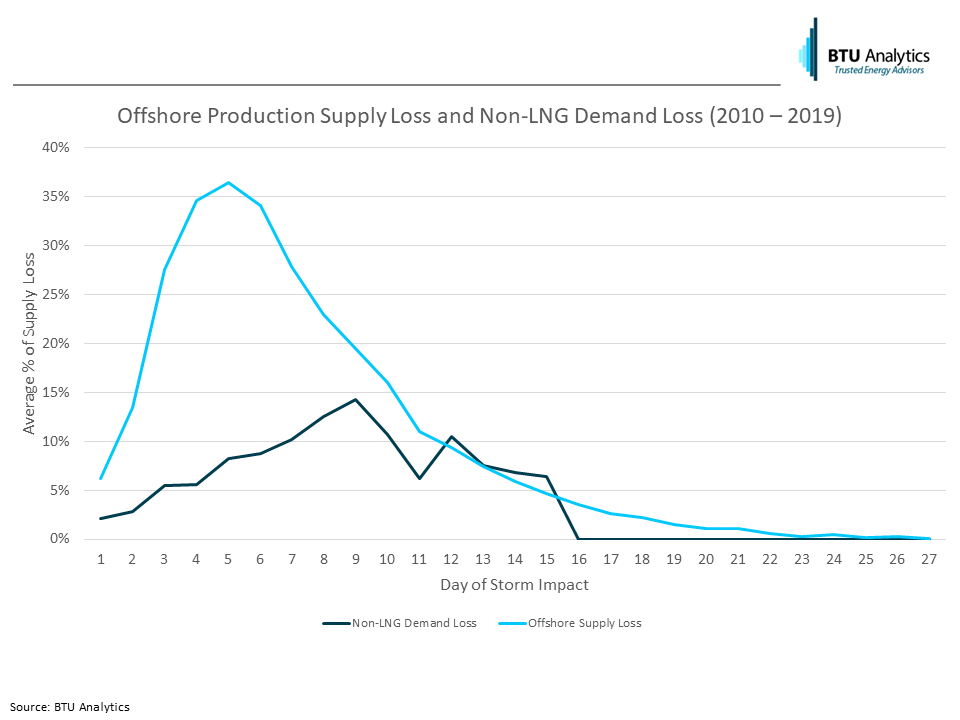

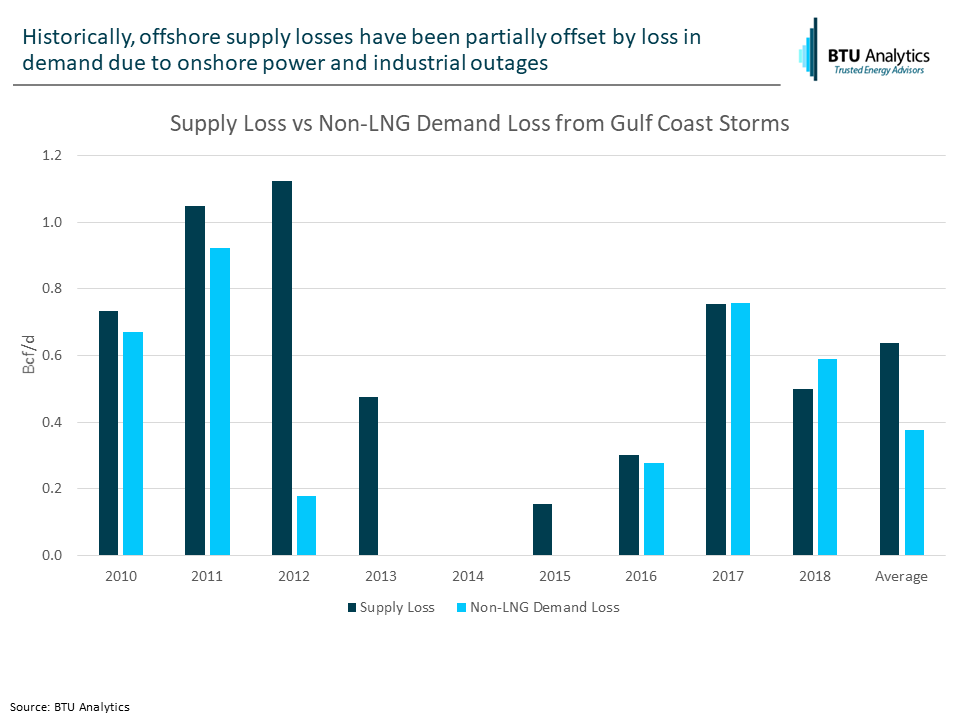

Since 2010, those supply losses have been partially offset by power and industrial outages as storms have made their way onshore. During the lifespan of a storm, on average, offshore supply came off by more than 640 MMcf/d, while demand shed about 370 MMcf/d.

Having both supply and demand losses evening each other out goes a long way for maintaining balance in the market. This was at least the case up until 2017 when LNG exports began to ramp up in force. Now LNG demand throws that partial balance way out of whack. Now the question is just how out of balance will it be?

The answer to that depends on the length of the storm and severity of the aftermath. LNG export facilities all have associated storage tanks that can help to mitigate some volatility in LNG production, however, as we have discussed previously storage can’t save the day forever. So, what would an ‘average’ Gulf Coast storm look like if one hit this year? The below graphic layers in supply loss, non-LNG demand loss, and LNG demand loss. At first LNG demand loss is mostly mitigated by storage, however, after about a week, storage fills and facilities are forced to stop feedstock deliveries as the storm drags on. This is reminiscent of what happened during Hurricane Harvey when feedstock deliveries to Louisiana facilities fell to virtually zero.

Over the next few years as Wave 1 LNG build out wraps up and Wave 2 ramps up (see our recent study for BTU’s outlook on Wave 2 and how the US supplies them), expect more demand to be at risk as hurricanes barrel through the Gulf of Mexico. The graphic below shows net demand loss (total demand lossless supply loss) over the next few years, with both a more minor seven-day storm and a more extreme Hurricane Harvey type storm.

Hurricanes are just one driver of pricing. However, there is a multitude of other drivers that move gas prices all across the country. From the Gulf Coast to Northeast to the Rockies, BTU cuts through the market noise in its Gas Basis Outlook and provides you with actionable and digestible information. Feel free to reach out and speak to an analyst about how we can help you succeed in this difficult market.