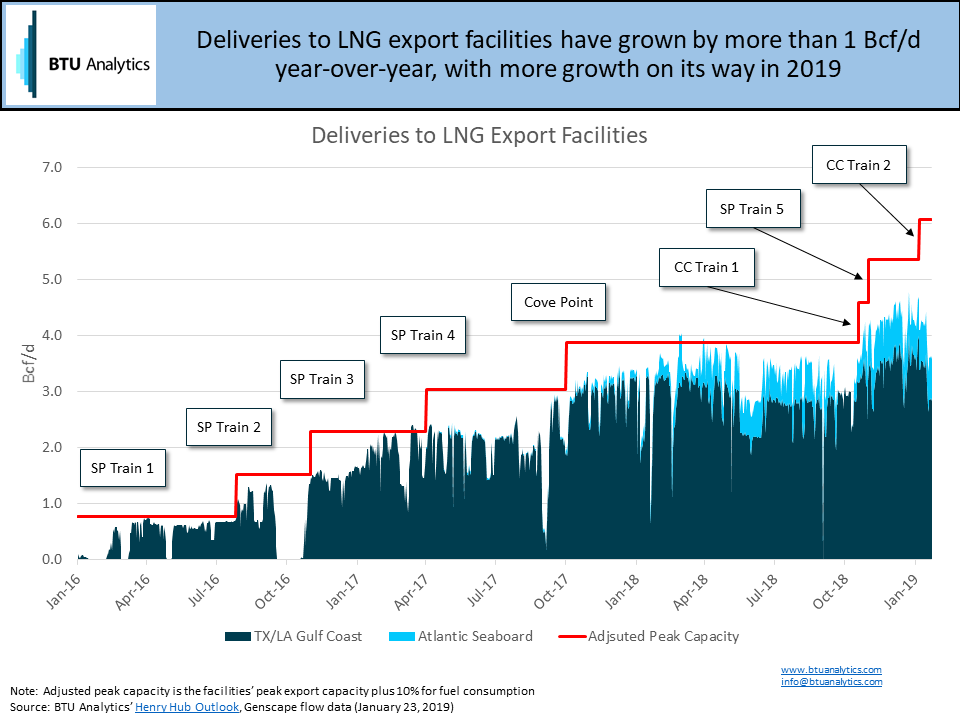

With Train 2 of Cheniere’s Corpus Christi LNG facility in the midst of commissioning and deliveries to the facility expected to ramp shortly, LNG exports are further cemented as a core of the US’ natural gas demand mix. Going forward, this trend will only continue. For example, if facilities under construction hit their current in-service dates, then the US will get to about 9 Bcf/d of LNG export capacity, and feed gas for those new facilities will make up more than 65% of the US’ structural natural gas demand growth in 2019. With so much demand concentrated mostly on the Louisiana and Texas Gulf Coast, an influx of feed gas and supporting infrastructure will change historic pricing dynamics along the Gulf Coast.

With the growth of LNG feed gas targeting the Gulf Coast, as shown in the graphic below, and more on the way, combined with the impact of new infrastructure out of the Northeast and Permian, BTU has expanded our coverage of natural gas basis analysis and forecasts with the Gas Basis Outlook to more fully capture the changing pricing dynamics in North America.

To further highlight these emerging challenges for the gas market we will be hosting a complimentary webinar on February 5th.

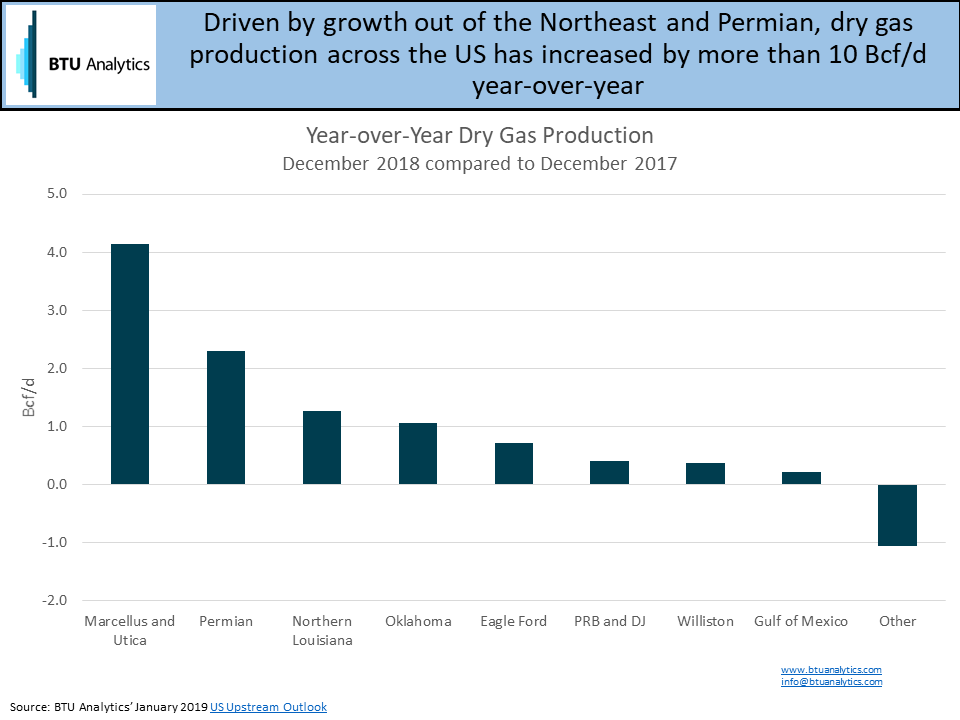

Beyond Gulf Coast LNG demand pulling incremental molecules down to the Gulf, other markets have been inundated with low cost supply that has put, and continue to put, downward pressure on pricing. While the US added 10 Bcf/d of production year-over-year, the biggest culprit for providing downward pricing pressure has been the Permian, which, in 2018, added almost 2.5 Bcf/d associated gas supply that is driven by liquids economics rather than gas pricing.

To date, western basis has most noticeably felt the brunt of expanding Permian pressure with CIG basis averaging $0.60/MMBtu back in 2018 compared to about $0.30/MMBtu in 2017. However, an outlet for this gas is expected to arrive in 2019 in the form of Kinder Morgan’s 2 Bcf/d Gulf Coast Express, which will provide some (short-lived) relief to Rockies’ and Permian pricing, while transferring pressure towards Agua Dulce and the Texas Gulf Coast.

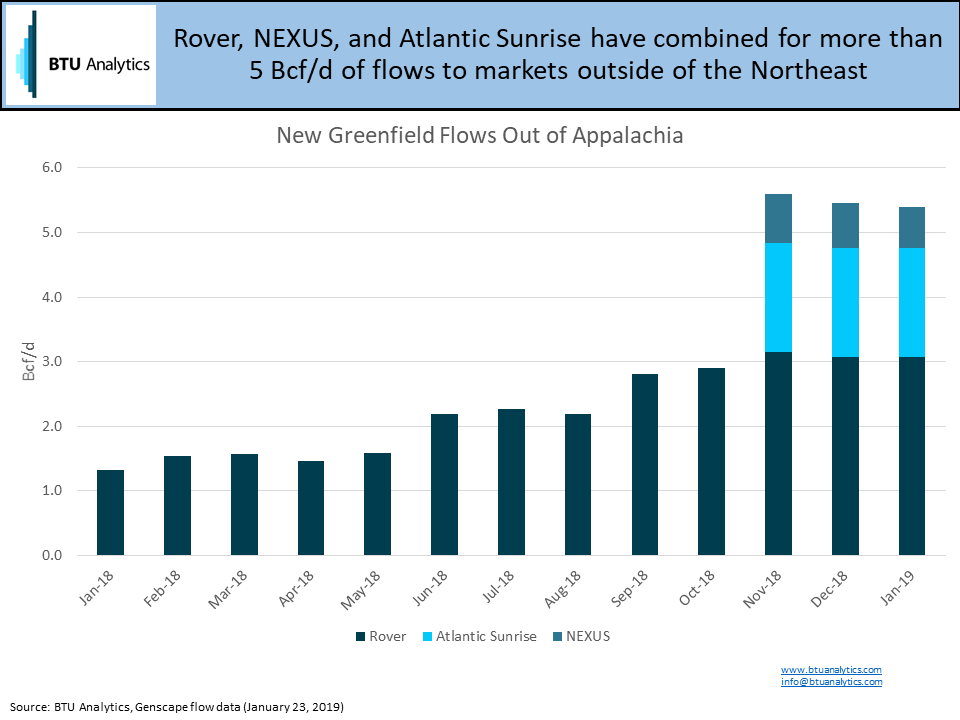

Not to be outdone, the Northeast has also gone through its own infrastructure transformation in 2018, with major greenfield projects, Rover, NEXUS, and Atlantic Sunrise either ramping up or commencing service as shown in the graphic below.

Atlantic Sunrise capacity moves molecules down the Atlantic Seaboard into the Southeast, while Rover and NEXUS capacity mostly target Upper Midwest markets. With most of the ramp-up inflows taking place in the fourth quarter, the full effects of this new capacity have been masked by winter heating demand. However, when winter ebbs, expect molecules to do their best to make their way down to the Gulf towards growing LNG demand contributing to further congestion along the Gulf Coast, Perryville, and Carthage.

This confluence of molecules, either directly or indirectly, making their way down to the Gulf Coast, combined with the pull of new LNG demand coming online, set the scene for an interesting 2019. Sign up for our free webinar to see what we are watching for in 2019.