Following on the heels of strong 2Q2014 production results in the DJ Basin and more growth expected to come, two new pipeline projects announced open seasons to connect rapidly growing DJ crude production to Cushing. The first announcement was by Enterprise Product Partners for a 30”, 340 Mb/d (expandable to 700 Mb/d) pipeline which would originate in the Bakken, and pass through both the Powder River and DJ basins to pick up additional supply to be delivered to Cushing. The DJ to Cushing section of the pipeline is expected to be operational by 4Q2016. The second pipeline open season announcement, the Grand Mesa Pipeline Project, came from a JV between Rimrock Midstream and NGL Energy Partners. The proposed 130 Mb/d pipeline would originate in Weld County, CO and terminate at NGL’s Cushing, OK, terminal.

Supporting these pipeline open season announcements are the facts that not only have the two largest producers in the region, Noble and Anadarko, set aggressive growth targets, but also companies like Bill Barrett, Bonanza Creek, and PDC Energy are focusing their efforts on further developing the region. All three of these companies have allocated at least 75% of their capex budgets to the development of the DJ Basin.

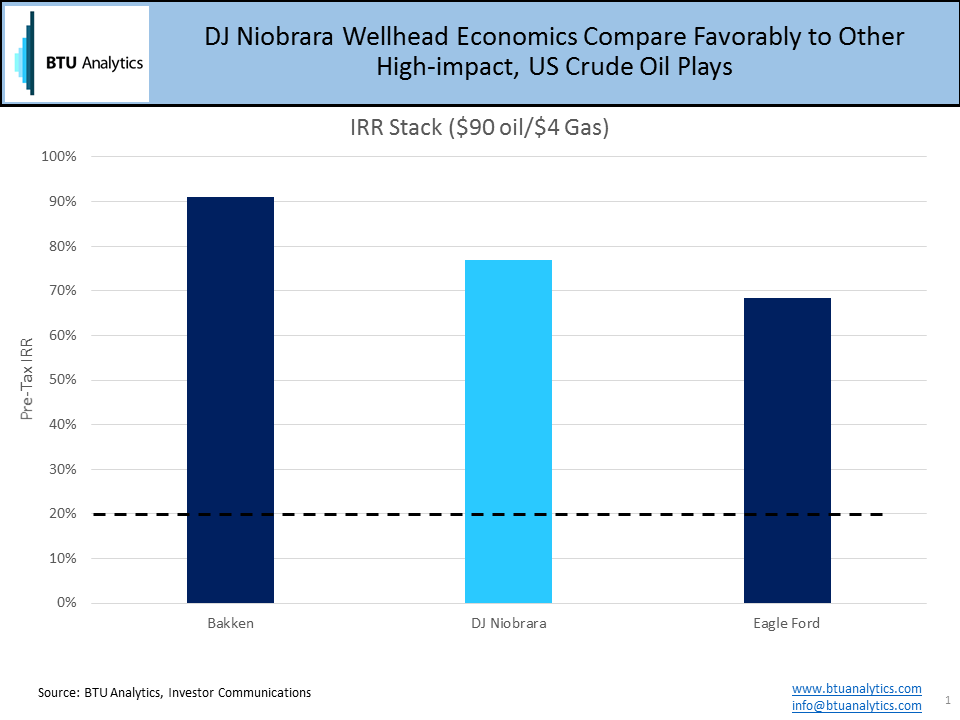

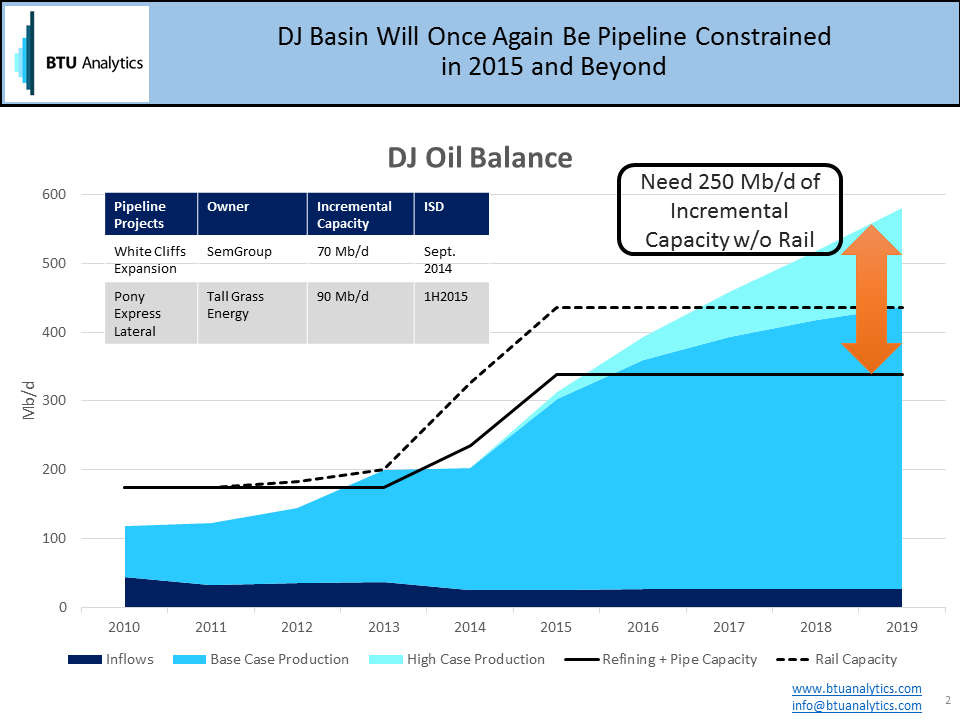

BTU Analytics’ IRR calculations show that at $90 oil and $4 gas, the DJ Basin stacks up extremely favorably, at 77%, against other leading plays like the Bakken and the Eagle Ford (see chart 1). Contributing to the strong IRR is relatively low well costs. One factor contributing to the lower well cost is shorter lateral lengths in the DJ. However, many producers are experimenting with longer laterals, which would increase well costs, but should also increase EURs and IP rates. Noble has reported that its long laterals (9,000’) cost $7.7 million and have an estimate EUR of 750 Mboe. This is compared to the Bakken, where they are drilling two-mile laterals and well costs average between $7.6-$8.8 million and have an estimated 600 Mboe EUR. Even if well costs increase from the current average of $5 million, the strong IRR supports continued investment in the play, resulting in upside potential to BTU’s base case crude oil production forecast for the region (see chart 2). Under BTU’s base case forecast, DJ crude production will once again become pipeline constrained in early 2016. Under BTU’s high case forecast, DJ crude production will be pipeline constrained and reliant on rail or new pipeline projects as early as mid-2015 (see chart 2). BTU estimates that without rail, on average by 2019, an additional 250 Mb/d of pipeline capacity beyond the White Cliffs expansion and Pony Express Lateral will be needed to provide takeaway capacity out of the DJ Basin.

Both the Grand Mesa Project and Enterprise pipeline lock producers into shipping crude to Cushing and on to the Gulf Coast, both of which are already being inundated with growing indigenous, light sweet production. With light sweet imports all but displaced from the PADD 2 and PADD 3, and refineries running at historic highs, the DJ Basin is facing a much larger problem than transportation. Without crude oil exports, BTU Analytics expects WTI to come under downward pressure. But will that pressure be enough to slow down production? With IRRs in excess of 70% at $90 wellhead in many of the large plays, it seems as though prices could fall significantly before producer activity is curtailed…

Erika Coombs will be speaking on Rockies crude oil supply and demand at the Wyoming Oil and Gas Fair, September 18th, 2014.

If you are interested in for more information on the new DJ crude pipelines go to: