Williams and Chesapeake Energy announced new contract last week for gathering services in the Haynesville and Utica meant to incentivize continued development in both plays. Last week our commentary discussed prospects for the Haynesville as evolving drilling and completion practices might finally be opening the door for more activity out of that play. Today we want to highlight one of the remaining bright spots for infrastructure investment currently in the energy industry, the dry Utica.

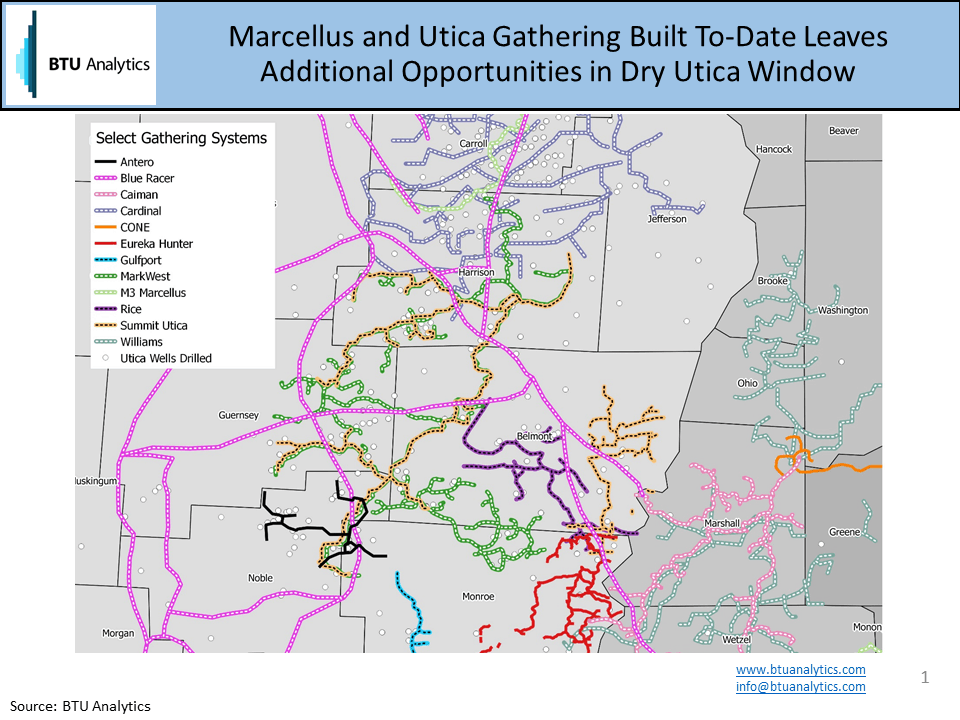

The Williams/Chesapeake announcement highlighted the need for additional dry Utica gas gathering. While wet gas systems exist across much of the region to support the development of the Wet Marcellus, putting dry Utica gas on a wet system makes little sense, as producers of the dry gas would be burdened with unnecessary processing costs that would reduce their returns. The map below highlights some of the major gathering systems surrounding the area. (Note the lines with white dashes are wet systems, black dashes are dry systems, no dashes for systems where public data is unclear).

Many midstream companies are eager to sign producers up to new projects, but with several of the larger producers in the region tied to MLPs of their own creation, will there be enough volume growth from the Dry Utica to support a project for every company proposing projects? Likely not, particularly if capital budgets remained constrained by weakened balance sheets and slowing payback cycles.

For detailed analysis of Northeast natural gas markets, request to learn more about BTU Analytics’ Firm Dilemma Study and Northeast Gas Quarterly products.