The North American energy market makes efficient work of taking what were once attractive spreads, whether they be geographic or seasonal, and building additional infrastructure to create the capacity to crush the aforementioned spread. Bye-bye spread. In the gas market this has happened many times. One prominent example being the building of Rockies Express in 2009, and another playing out currently with the building of over 18 Bcf/d of pipeline reversals coming out of the Northeast headed to the Midwest and Southeast. In BTU Analytics’ recently released natural gas market study – ‘A Firm Dilemma – Winners and Losers of the Natural Gas Pipeline Reversal Race’, one of the main takeaways is that we expect the pipeline reversals to make Dominion South, which has been severely weak in 2015, tighten to a variable transport cost below Henry Hub.

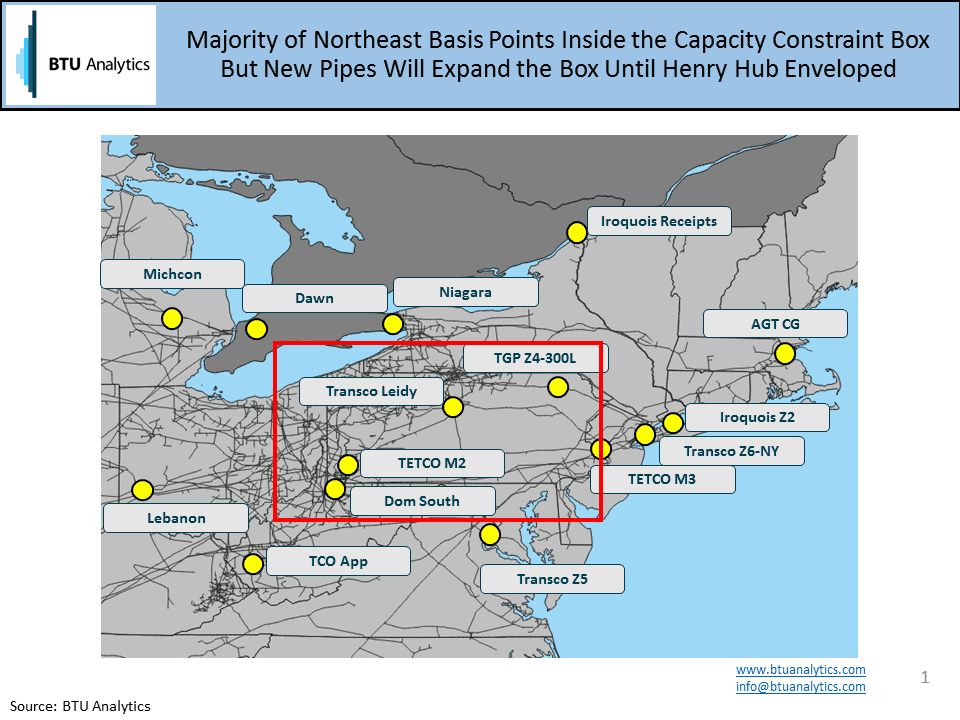

We spent a good part of the paper talking about our basis forecast through 2020 for various Northeast markets and Henry Hub. As shown below, we talk about Northeast supply area markets being ‘in the box’, meaning they have limited access to outside markets and are currently oversupplied. Clearly in 2015 YTD, points such as Tennessee Zone 4 and Dominion South have been ‘in the box’ trading in the outright cash market at $1.20 per MMBtu and $1.64 per MMBtu, respectively compared to Henry Hub at $2.79 per MMBtu. Points ‘out of the box’ typically have stronger demand and access to Marcellus and Utica supply is limited by a pipeline constraints. The question is, with all the Northeast production growth and pipeline reversals going into service between now and 2020, when does Henry Hub fall ‘in the box’? And by extension, once US LNG exports fire up, does the National Balancing Point (NBP) natural gas index in the UK start to fall ‘in the box’ on a seasonal basis as well? Is the US natural gas over-supply situation set to spill over into the European LNG market?

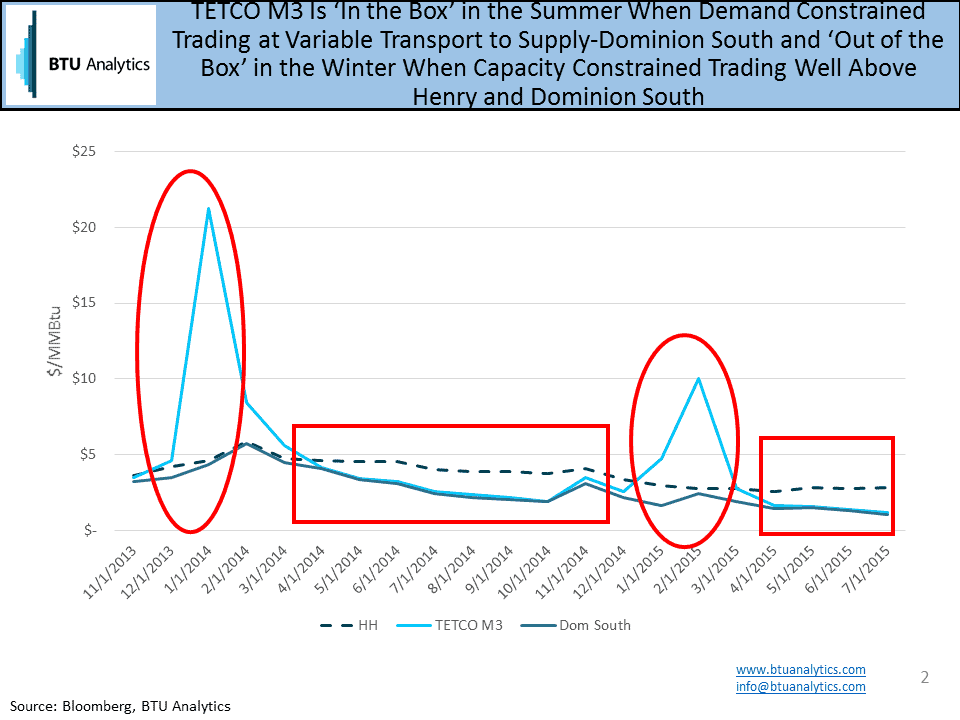

Some markets such as TETCO M3 are only ‘in the box’ on a seasonal basis. This means that TETCO M3 trades at variable cost to Appalachian supply points in summer when the pipe is demand constrained. In the summer of 2015 season to date, M3 has traded 12 cents over (about variable cost of transport) Dominion South. In the winter demand shoots higher and prices are set by scarcity as pipeline capacity approaches full utilization Last winter, Dominion South traded at $2.27 per MMBtu with M3 at $4.64 per MMBtu, a $2.37 per MMBtu spread (see red ovals below). M3 is clearly ‘out of the box’ in the winter.

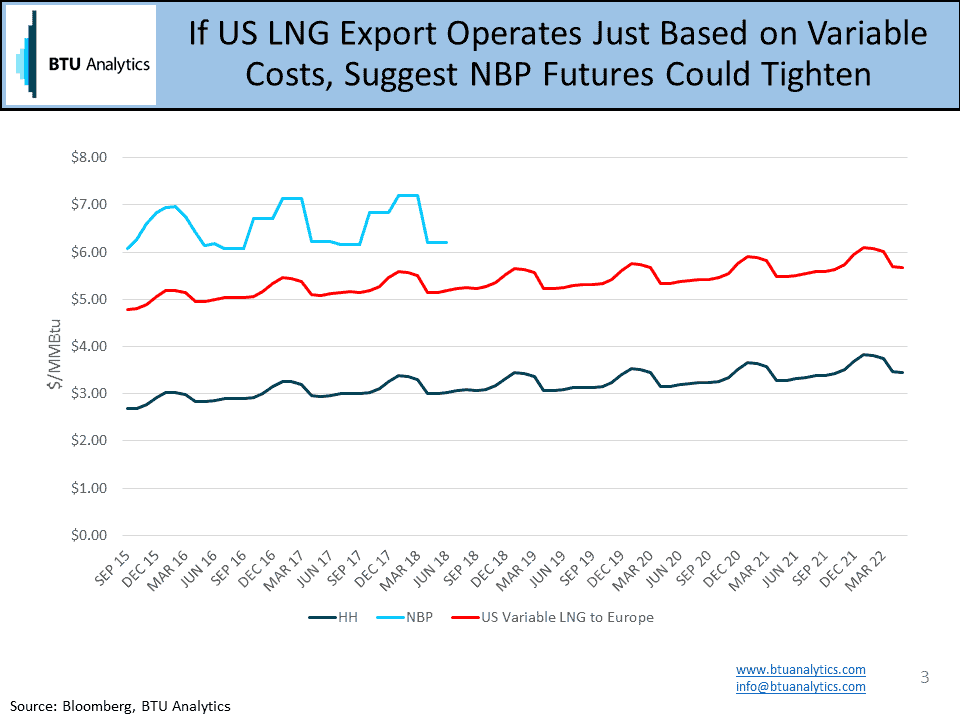

If a flood of US LNG hits the European markets, a similar M3 situation may evolve for NBP, albeit the variable cost will be much more than 12 cents. For the sake of this blog, let’s assume US LNG exports are dispatched based on variable economics, not all-in economics. In simple terms, if we assume the liquefaction fee is a sunk cost, then shipping LNG to Europe is a logical destination based on a calculated landed cost. Using the NBP as a price point results in a US LNG export variable cost to the UK at about $2.15 per MMBtu (assuming 15% of HH prompt, transport fees of $1.20 and a $0.50 regas fee). The chart below shows Henry Hub and NBP futures compared to a US landed variable cost (15% of Henry Hub plus $1.70) into the UK well below the current NBP futures curve. Go crush that spread US LNG exporters.

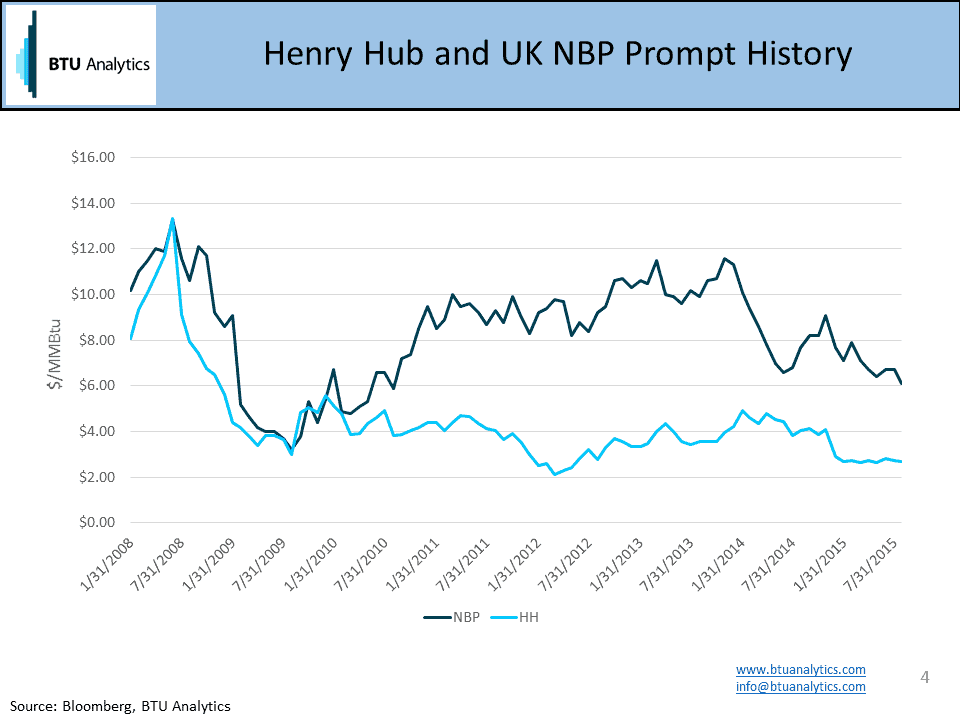

Recent price action of Henry Hub and UK NBP prompt prices would suggest we may be well on our way to achieving a tightening of the UK NBP-Henry Hub spread even though US LNG exports have yet to start. US LNG exports will be the first very liquid and free market to export gas, so we really have no analog to which to refer. Only time will tell. To better understand how US natural gas markets will evolve over the next five years, request a table of contents and figures table of ‘A Firm Dilemma’.

Recent price action of Henry Hub and UK NBP prompt prices would suggest we may be well on our way to achieving a tightening of the UK NBP-Henry Hub spread even though US LNG exports have yet to start. US LNG exports will be the first very liquid and free market to export gas, so we really have no analog to which to refer. Only time will tell. To better understand how US natural gas markets will evolve over the next five years, request a table of contents and figures table of ‘A Firm Dilemma’.