Changes are on the horizon for natural gas liquids (NGLs) production in the Northeast. In late October, Energy Transfer Partners announced that they expect Mariner East 2 (ME2) to enter service “shortly” as the first phase is nearly mechanically complete. Mariner East 2’s full capacity will be 275 Mb/d when it is complete in late 2020, but the pipeline initially going into service will be a combination of existing and new pipelines at a reduced capacity. ME2’s impending startup, even at a reduced capacity, could be a catalyst for producers to shift drilling from dry gas acreage to acreage with higher yields of natural gas liquids. So how does Mariner East 2 change the landscape for Northeast producers?

Appalachian NGL production has historically exceeded pipeline takeaway capacity, forcing producers to truck or rail NGLs to downstream markets and not recover the full amount of ethane from the natural gas production stream. Mariner East 2 will carry propane, butane, and natural gasoline to the Marcus Hook export terminal near Philadelphia, PA. Additionally, the existing Mariner East pipeline will enter dedicated ethane service. The conversion will improve the producer’s ability to recover ethane from the natural gas stream.

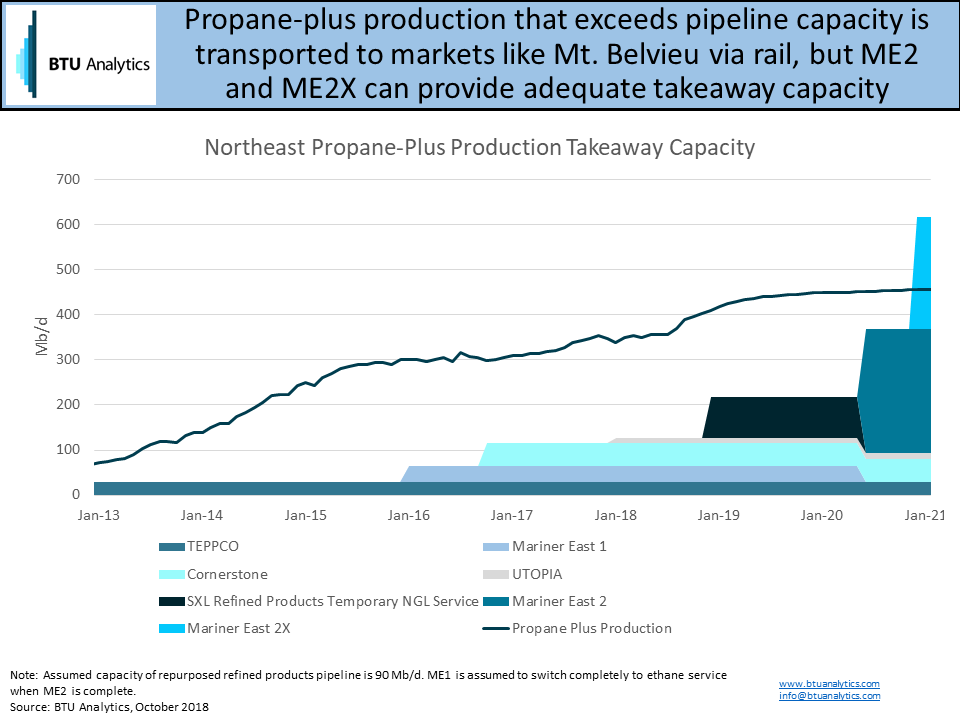

The graph below shows historical and forecasted propane plus production from the Marcellus and Utica versus pipeline takeaway capacity. Even partial completion of Mariner East 2 represents a significant step change in pipeline capacity for the region. The full completion of the system in 2020 will, for the first time, give producers in the region an excess of NGL pipeline takeaway capacity. Additionally, Mariner East 2 will allow direct access to export markets via Marcus Hook and end the reliance on truck and rail.

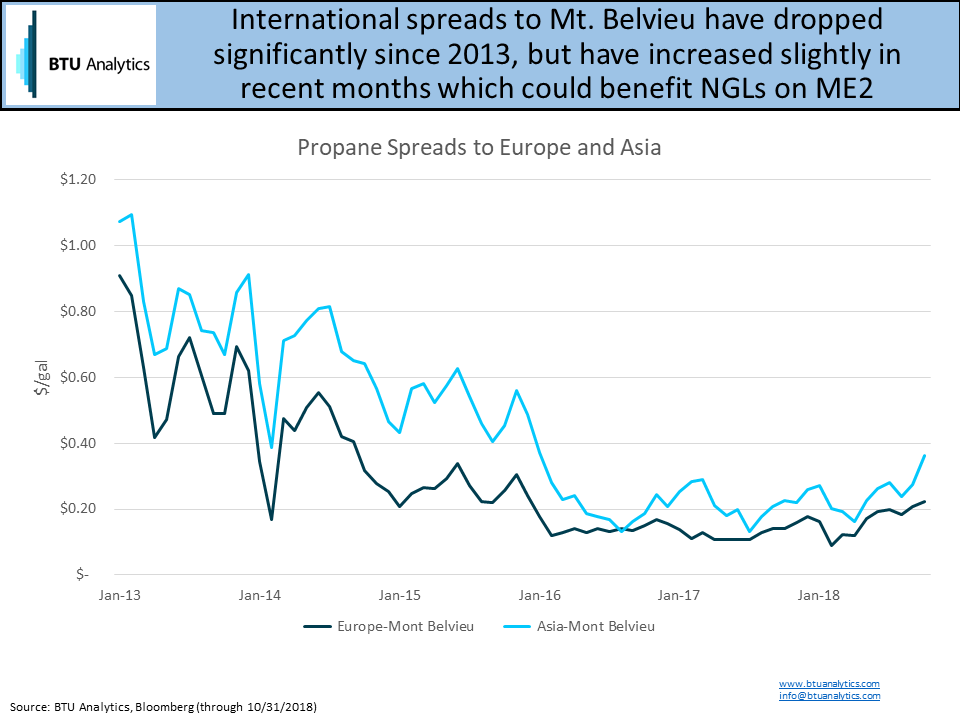

The historical reliance on truck and rail for Marcellus and Utica producers resulted in higher transport costs and wider differentials compared to other plays with pipeline access to Mt. Belvieu. Mt. Belvieu and other Gulf Coast hubs have benefited from the ability to export excess natural gas liquids to global markets. Once in service, ME2 will provide pipeline takeaway capacity to the Marcus Hook terminal where NGLs can be distributed along the Eastern Seaboard or exported from Marcus Hook to international markets. This new route for Appalachian producers could provide a significant uplift compared to railing natural gas liquids to the Gulf Coast if international prices remain strong. As shown in the graph below, spreads between Mt. Belvieu, Europe, and Asia for propane have started widening in 2018, but remain well below 2013 levels.

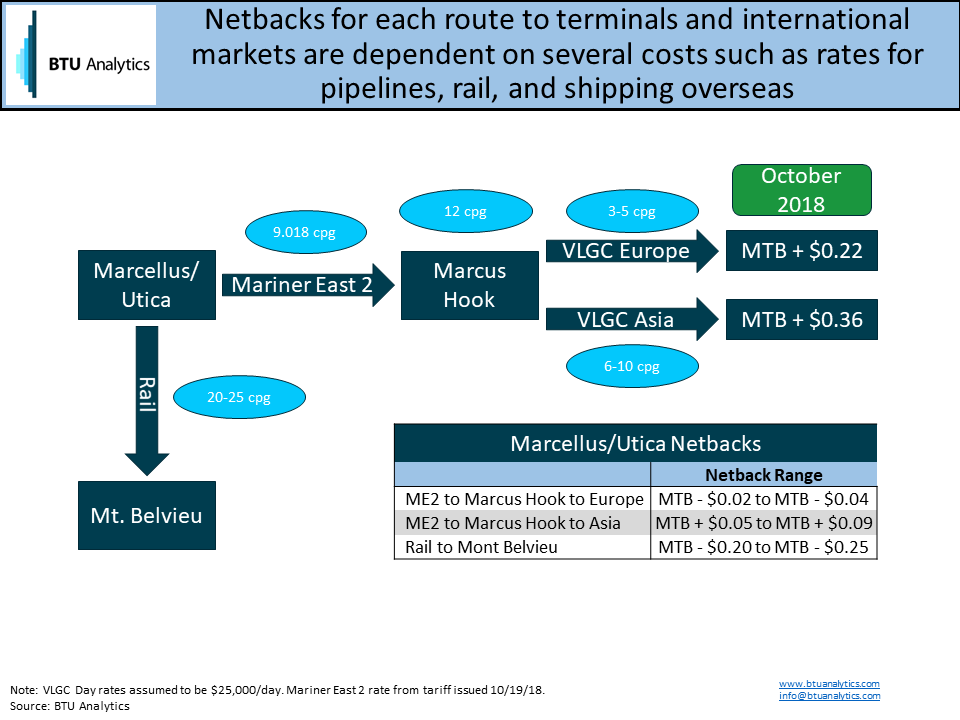

With European prices at a $0.20 premium in October to Mt. Belvieu and Asian prices at nearly a $0.40 premium, the incentive to export internationally has grown. The graphic below provides an illustrative example of the potential uplift for Northeast producers with access to Mariner East 2 pipeline capacity.

Currently, producers are faced with marginal barrels moving on rail to Mt. Belvieu at an estimated cost of 20-25 cents per gallon while Mariner East 2 should have a cost of roughly 9 cents per gallon. A significant improvement over rail. However, additional fees are incurred before producers can reach export markets including paying for export rights at Marcus Hook of roughly 12 cents per gallon and shipping costs to downstream markets that range from 3-5 cents per gallon to Europe and 6-10 cents per gallon to Asia. Even with the additional costs, producers should see netbacks improve significantly as highlighted in the table above.

Not surprising, two of the largest producers in the region have already announced plans to shift drilling to liquids rich acreage. In 3Q 2018 earnings, Range Resources (NYSE: RRC) said they will focus their fourth quarter production in wet acreage near upcoming processing plants to help meet firm capacity on Rover. Additionally, Antero Resources (NYSE: AR), which also has capacity on Rover, announced accelerated activity in liquids-rich areas in 4Q 2018 to capitalize on both stronger liquids pricing and ME2’s anticipated startup.

For more insights and analysis on BTU Analytics’ outlook for natural gas, natural gas liquids, and crude oil production, request a sample of our Upstream Outlook, and for a closer look at dynamics in the Northeast, request a sample of our Northeast Gas Outlook.